Key takeaways:

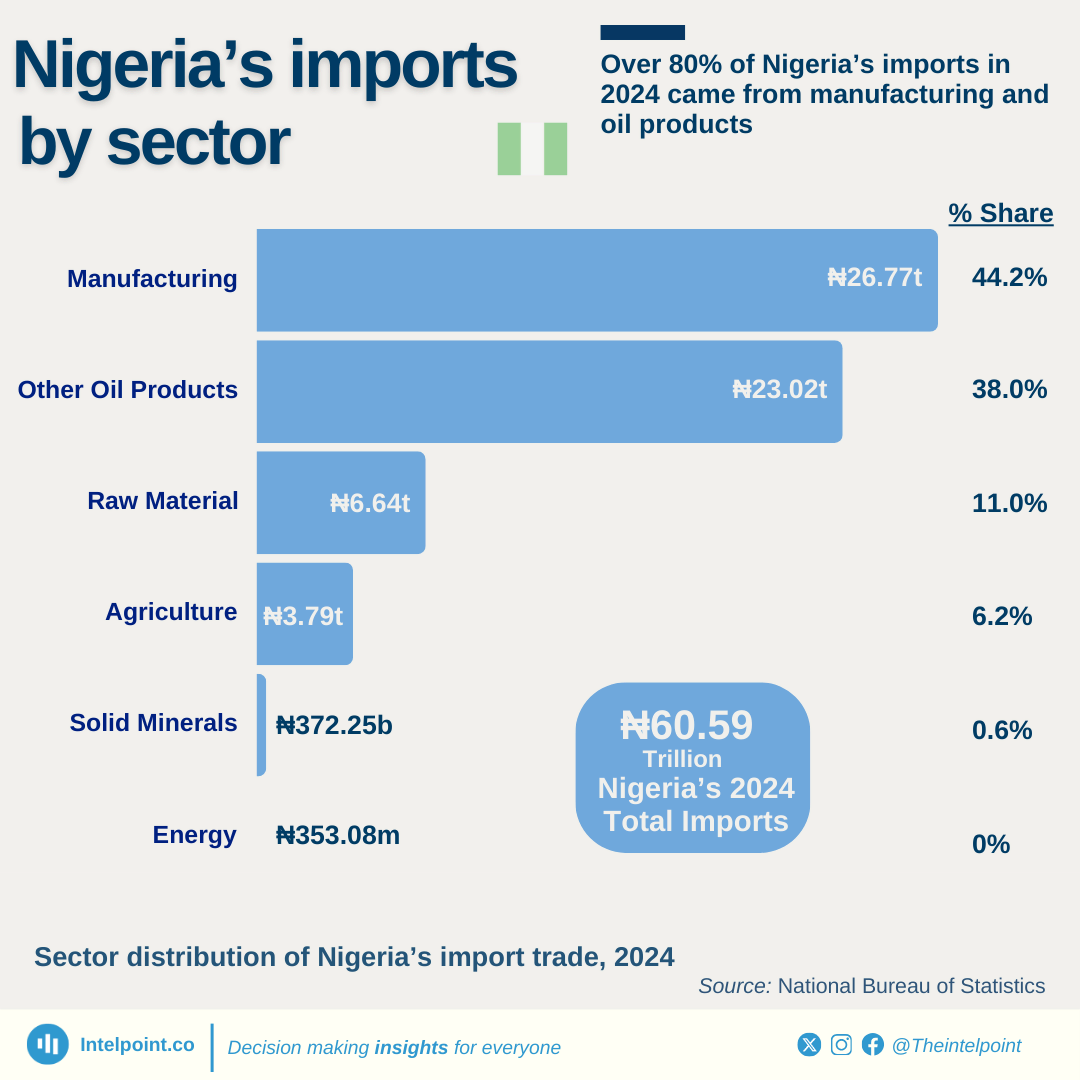

In 2024, Nigeria’s import landscape was predominantly driven by the manufactured goods and refined petroleum products sectors. The manufacturing goods sector tops Nigeria’s imports, accounting for 44.2% of the total ₦60.59 trillion in import value. Petroleum products (excluding crude oil) followed closely, contributing 38%, underscoring the country’s dependence on imported refined fuels despite being a major crude oil producer.

Raw materials accounted for 11% of Nigeria’s total imports, while agricultural products comprised 6.2%, highlighting the country’s reliance on foreign inputs for both industrial and food needs.