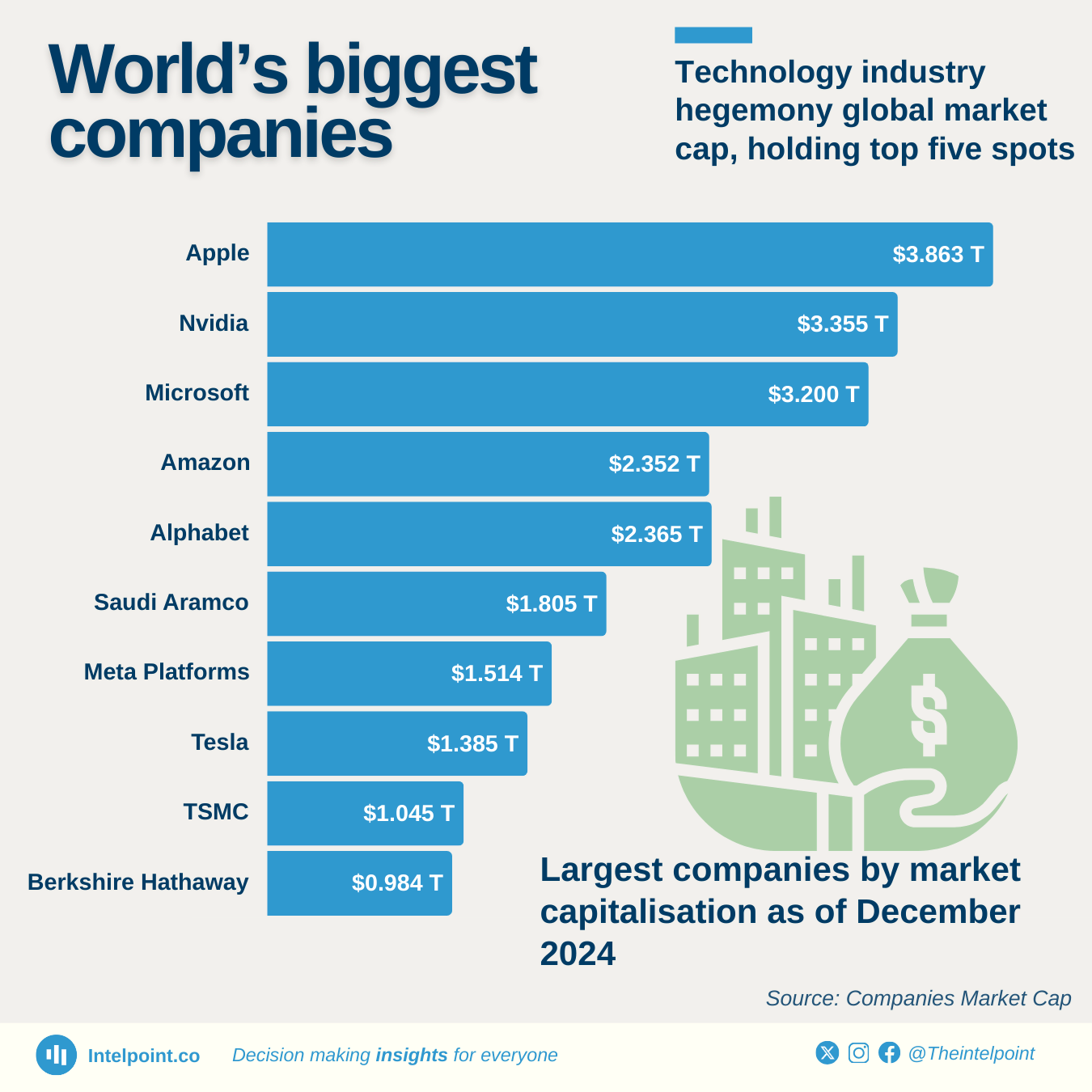

The rankings show that while technology companies dominate, industries like energy, finance, media, and automobiles still hold significant market value. The presence of Saudi Aramco, Berkshire Hathaway, Meta, Tesla, and TSMC on the trillion-dollar companies list displays the continued influence of these sectors on the global economy.