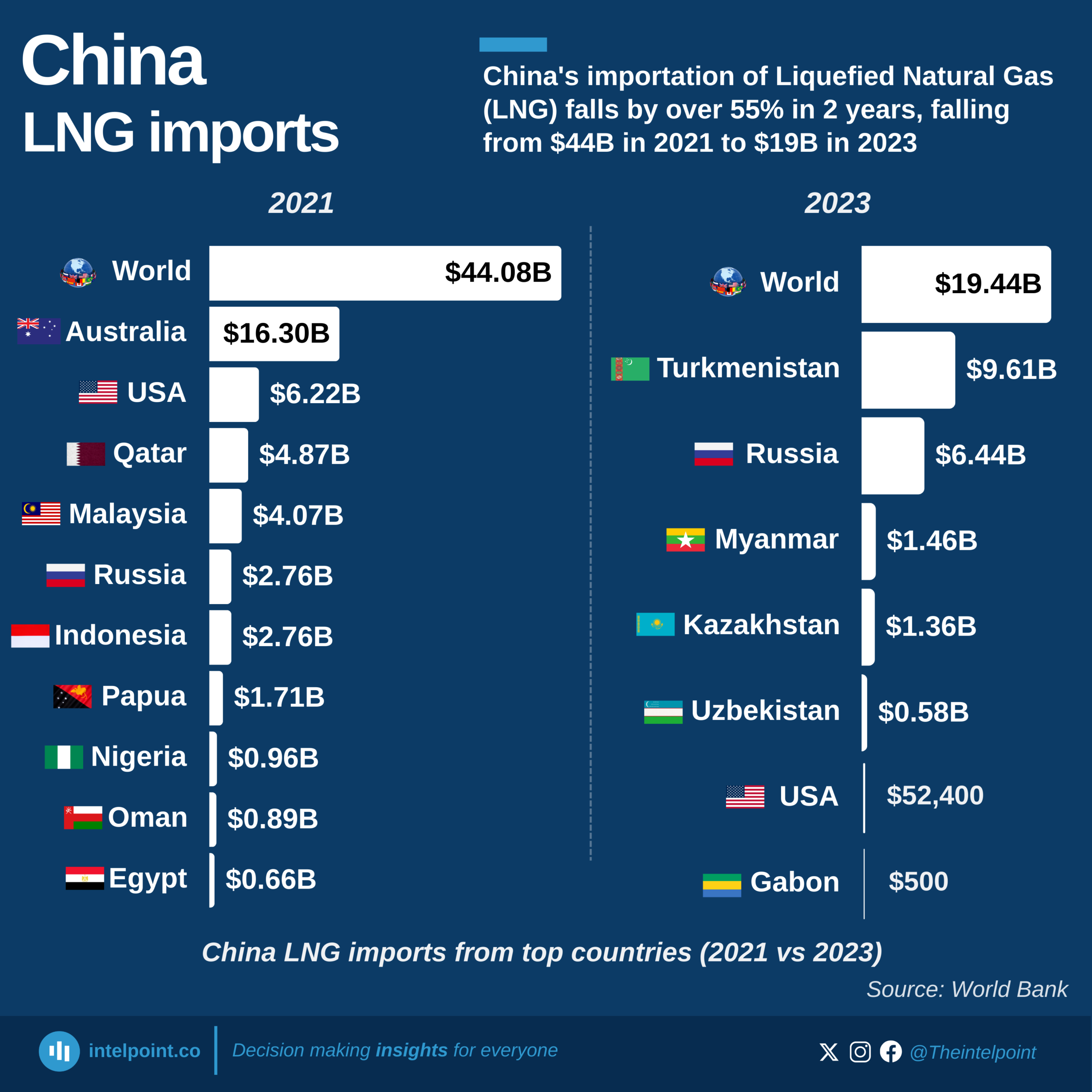

China’s importation of Liquefied Natural Gas (LNG) has declined, dropping from $44 billion in 2021 to just $19.4 billion in 2023. This steep fall of over 55% reflects a major shift in China’s energy-sourcing strategy. In 2021, Australia led as the top supplier with $16.3 billion in LNG exports to China, but by 2023, the entire landscape had changed, with Turkmenistan ($9.61 billion) and Russia ($6.44 billion) emerging as the dominant suppliers.

2021 also saw importations from Nigeria and other 26 countries, but in 2023, importations were just from 7 countries with Nigeria out of the scene.

This shift is not just about numbers, it tells a bigger story about geopolitical realignments and shifting trade preferences. The near disappearance of traditional suppliers like the U.S., Australia, and Qatar from China’s top LNG sources indicates a major transformation in global energy flows. The United States, which supplied $6.22 billion worth of LNG in 2021, saw its exports to China go down to an almost negligible $52,400 by 2023.