Global oil consumption rose from about 30.9 million barrels per day in 1965 to 101.4 million barrels per day in 2024, more than tripling over the period.

Asia Pacific saw the biggest structural shift in global oil demand, increasing its share from 10.7% in 1965 to 37.9% in 2024 to become the world’s largest oil-consuming region.

Africa accounted for just 1.9% of global oil consumption in 1965 and 4.5% in 2024, staying below 5% for nearly 60 years.

The global centre of oil demand has gradually shifted away from Western economies toward Asia, reflecting industrialisation, urbanisation, and population growth across the region.

Africa’s modest share of global oil demand highlights the continent’s relatively low industrial energy consumption despite rapid population growth.

The Strait of Malacca is the world’s most important oil chokepoint, carrying about 24–25% of global oil supply in recent years.

The Strait of Hormuz moves around 20–23% of global oil supply, making it the second-largest energy transit chokepoint.

The Cape of Good Hope carries about 9–10% of global oil flows, and its share tends to increase when other chokepoints face disruptions.

The Bab el-Mandeb saw a sharp drop in oil flow share from about 9% in 2023 to around 4% in 2024, reflecting security concerns affecting shipping in the Red Sea corridor.

Oil transported through the Suez Canal and the SUMED pipeline system dropped significantly after 2023, falling from about 8.6% to below 5%, showing how quickly routes shift during geopolitical tensions.

The Strait of Malacca’s share has remained consistently high and stable, indicating its structural importance to Asian energy demand.

Alternative routes like the Cape of Good Hope in South Africa are longer but strategically crucial, especially when Middle Eastern chokepoints become unstable.

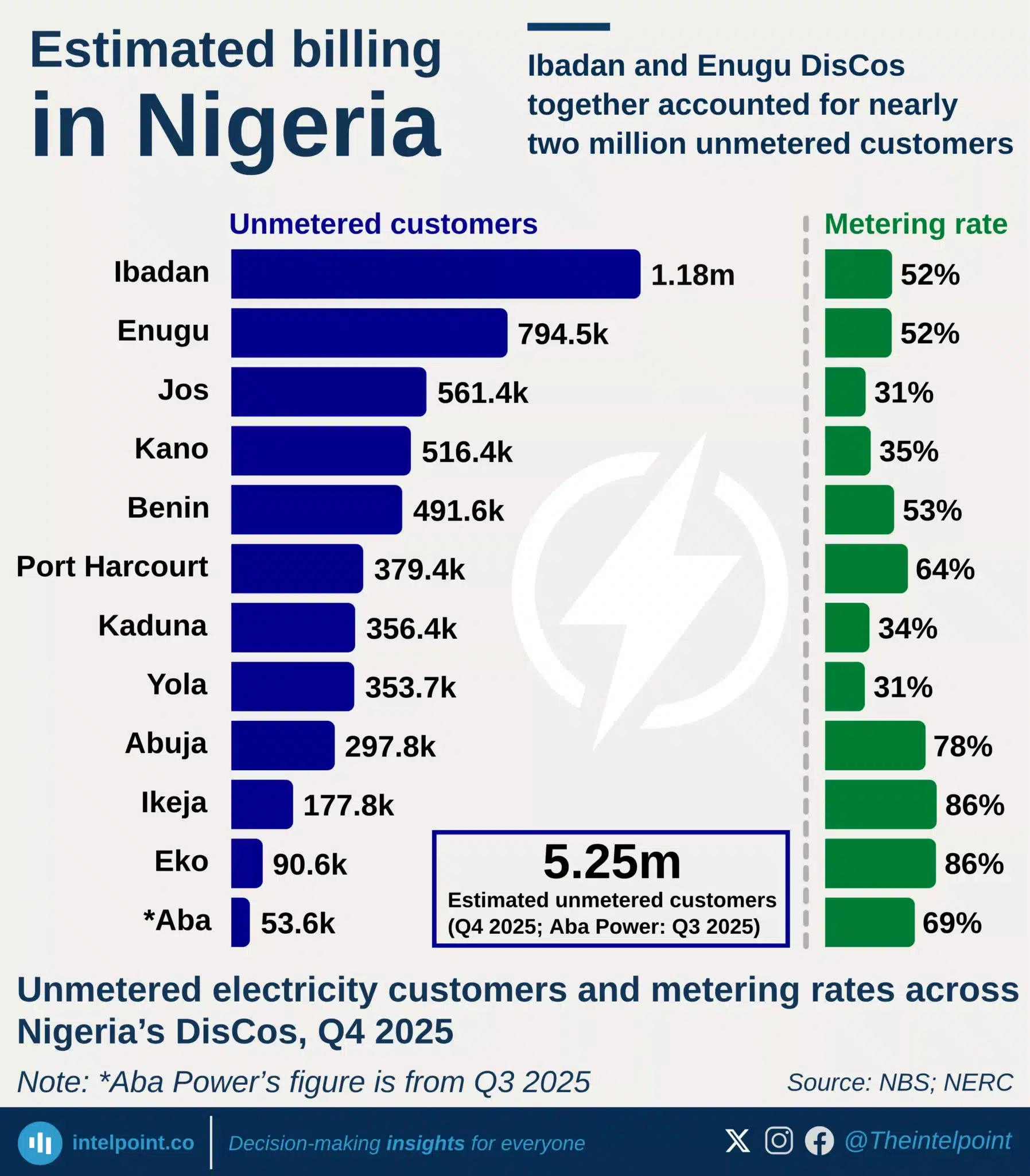

DisCos billed approximately ₦1.49 trillion but collected only ₦1.12 trillion in H1 2025.

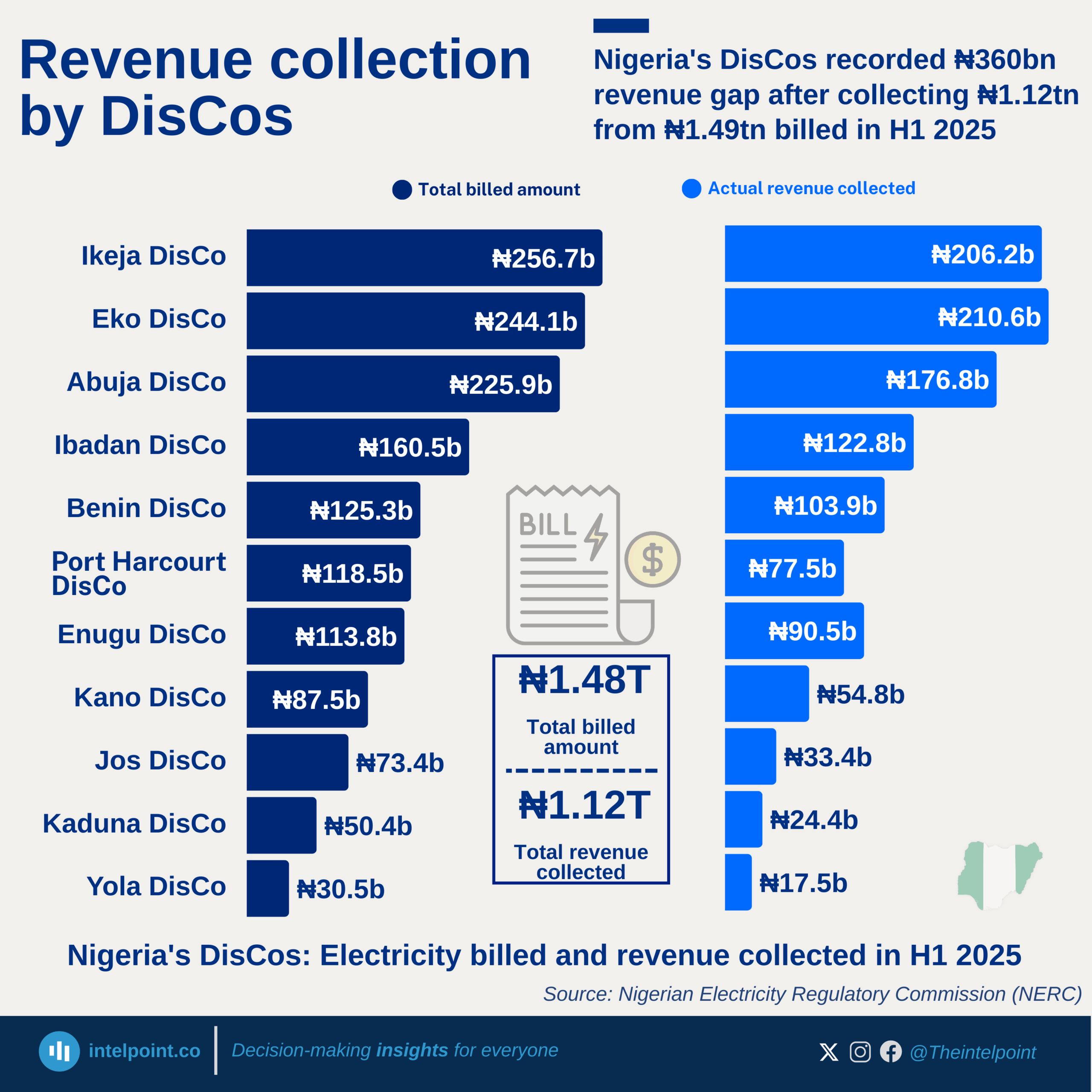

Ikeja and Eko DisCos generated the highest revenues, collecting ₦206.22 billion and ₦210.59 billion, respectively.

Revenue collection gaps remain significant, with Jos, Kaduna, and Yola posting the weakest collection performances.

The wide gap between billings and actual collections suggests persistent challenges in customer payment compliance, metering, and distribution efficiency.