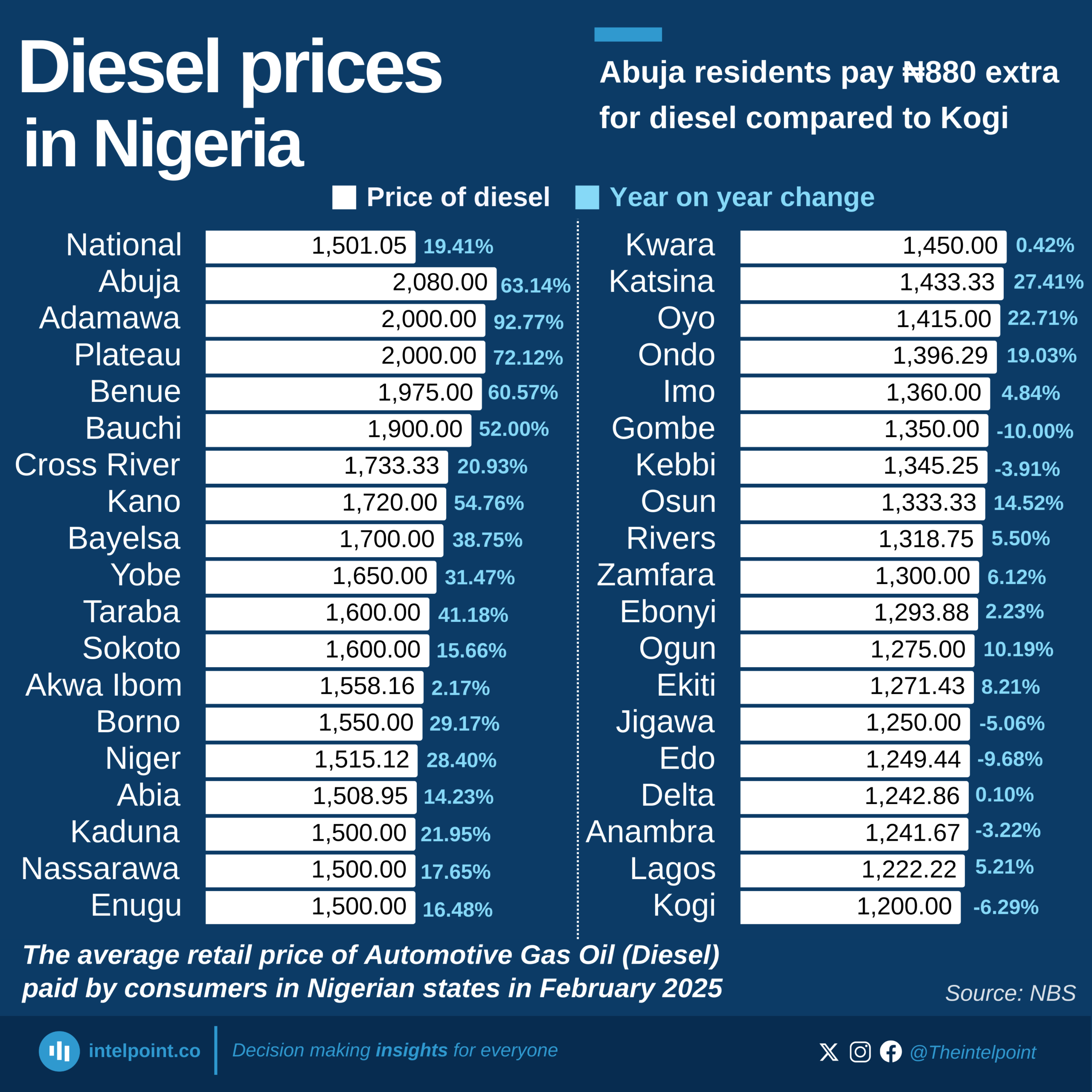

Diesel prices across Nigerian states have shown a range of changes over the past year, with some states seeing sharp increases and others recording declines. Nationally, the average diesel price rose by 19.41% between February 2024 and February 2025, reaching ₦1,501.05 per litre. However, this average masks major state-by-state disparities. States like Adamawa (+92.77%), Plateau (+72.12%), and Benue (+60.57%) saw massive surges, while places like Gombe (-10.00%), Edo (-9.68%), and Kogi (-6.29%) recorded significant drops.