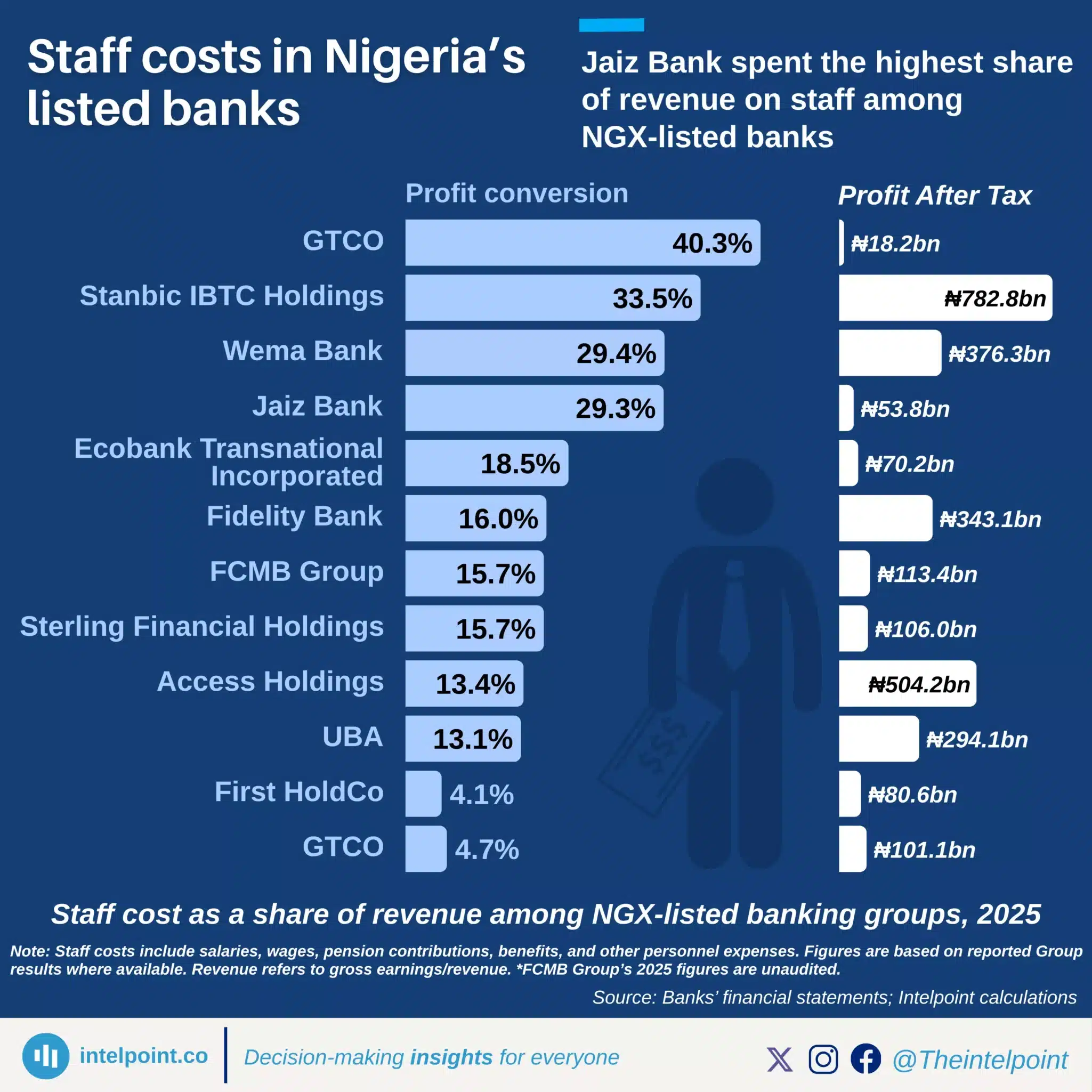

Jaiz Bank spent the highest share of revenue on staff in 2025.

Jaiz spent nearly ₦18 on staff for every ₦100 of revenue.

ETI and UBA followed with the next highest staff-cost-to-revenue ratios.

GTCO had the lowest staff-cost burden among the listed banks.

ETI spent the most in absolute staff costs, at ₦782.8 billion.

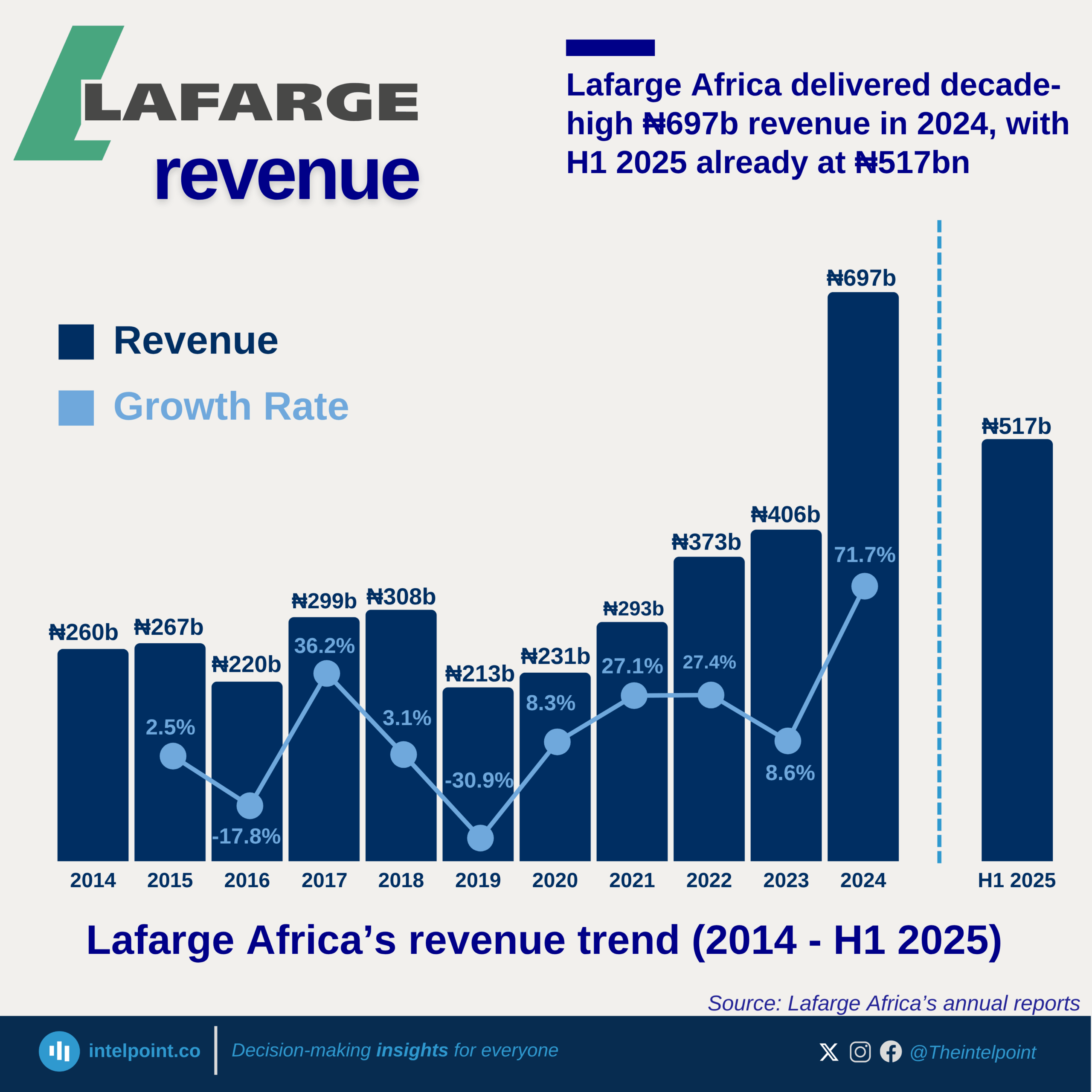

Lafarge Africa's revenue hit a decade-high of ₦697bn in 2024, reflecting a strong 71.7% year-on-year growth.

With ₦517bn in H1 2025 alone, Lafarge Africa has already achieved nearly 74% of 2024’s full-year revenue, signalling potential to surpass last year’s record if momentum continues.

The company has experienced sharp swings, including steep drops in 2016 (-17.8%) and 2019 (-30.9%).

Despite volatility, Lafarge has grown from ₦260bn in 2014 to ₦697bn in 2024, showing long-term expansion.

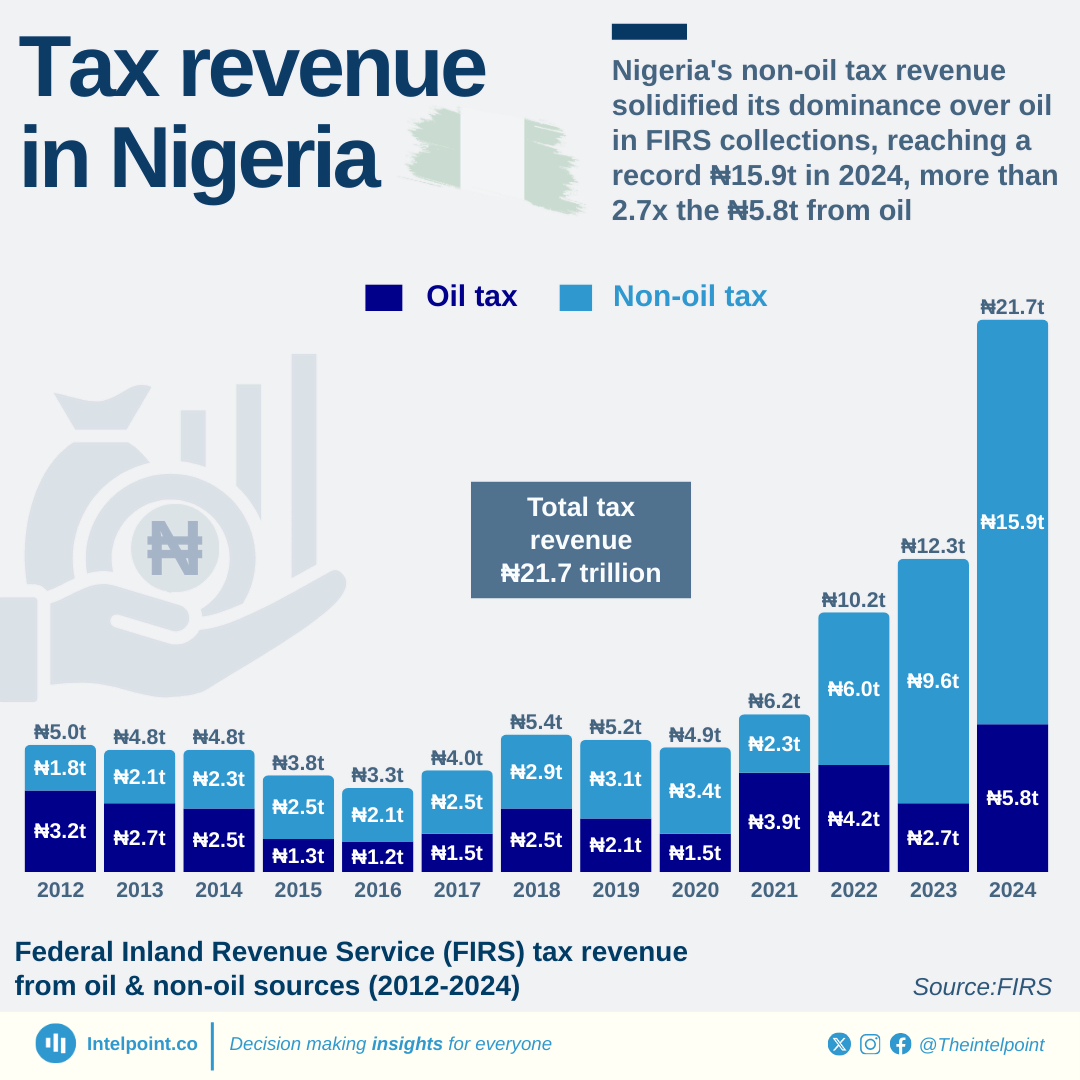

FIRS recorded ₦15.9 trillion of non-oil tax, almost three times the ₦5.8 trillion recorded for oil tax.

Non-oil tax revenue made up 73.3% of the total revenue collected in 2023.

From 2012 down to 2024, non-oil tax revenue surpassed oil tax revenue most of the time.

Oil taxes are petroleum profit tax and company income (oil & gas) tax while non-profit tax includes company income (non-oil) tax, gas tax, capital gains, stamp duty, NCS import VAT, and non-import VAT.