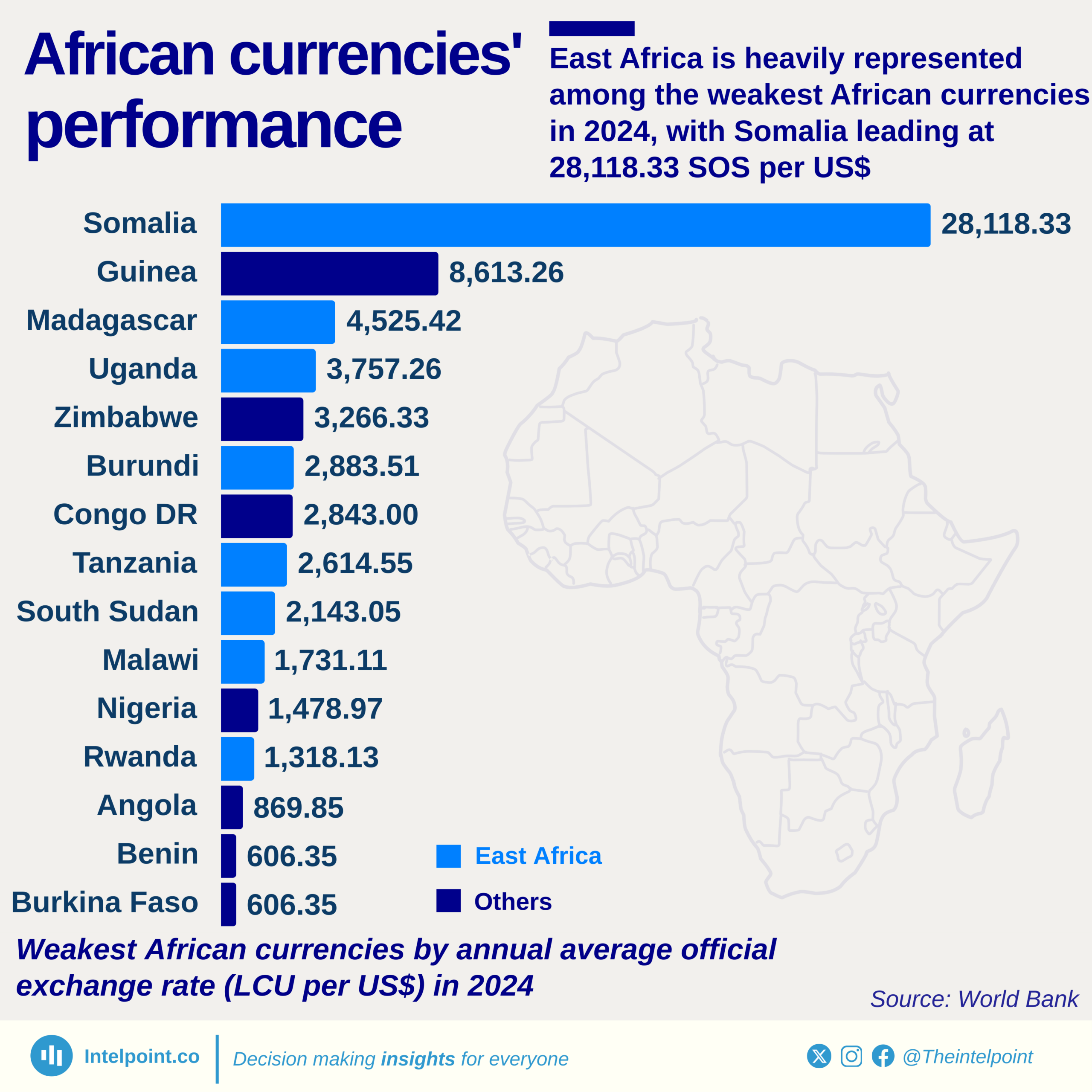

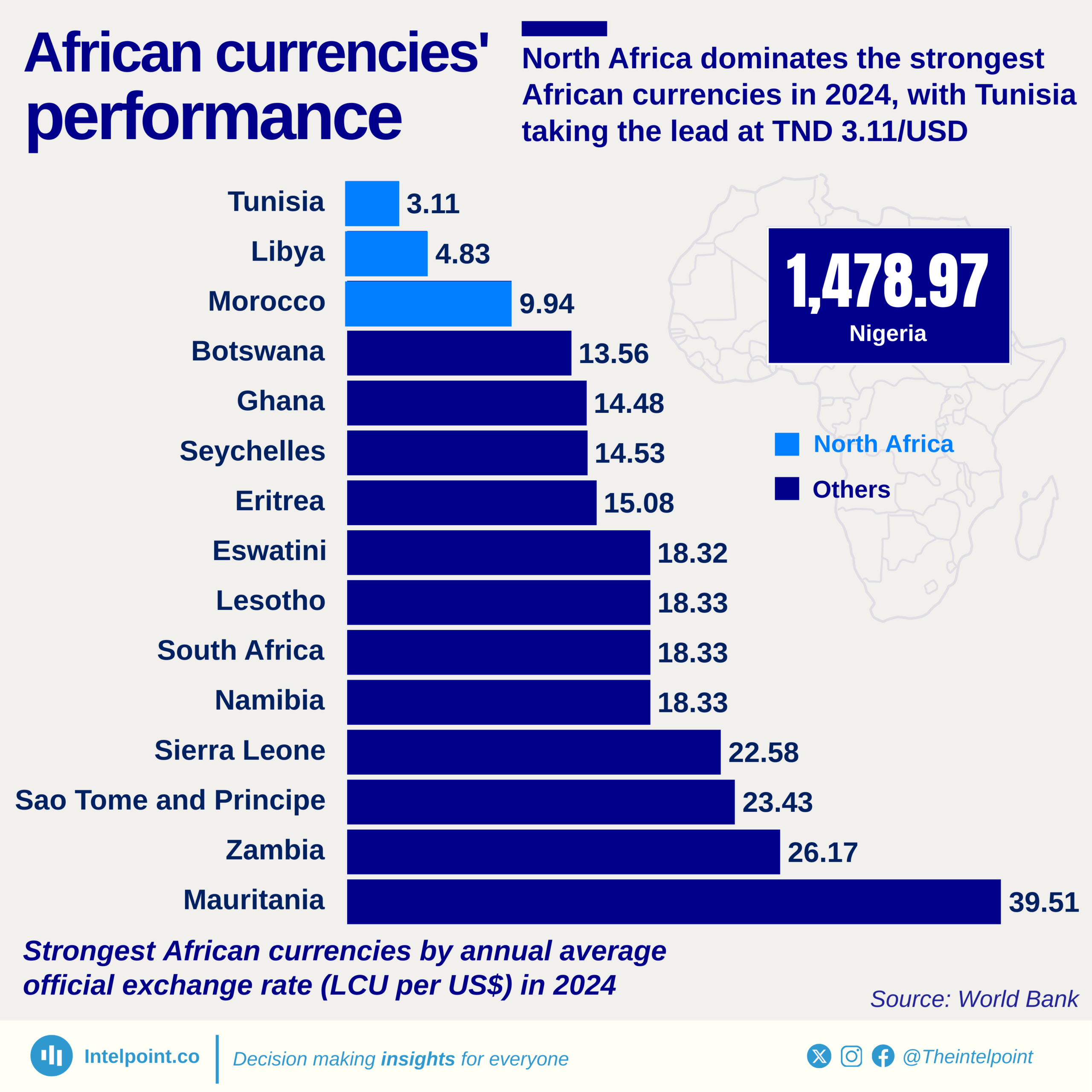

Tunisia held the top spot with the strongest African currency, trading at 3.11 TND per USD in 2024.

Libya followed as the second-strongest, with an exchange rate of 4.83 LYD per USD.

Morocco maintained a strong regional position, with its dirham trading at 9.94 MAD per USD.

Botswana’s pula was relatively stable, exchanging at 13.56 per USD, highlighting Southern Africa’s economic steadiness.

Ghana and Seychelles had closely matched exchange rates, trading at 14.48 and 14.53 to the dollar, respectively.

South Africa, Lesotho, Namibia, and Eswatini all shared almost identical exchange rates of around 18.32–18.33 per USD, showing tight regional monetary coordination.

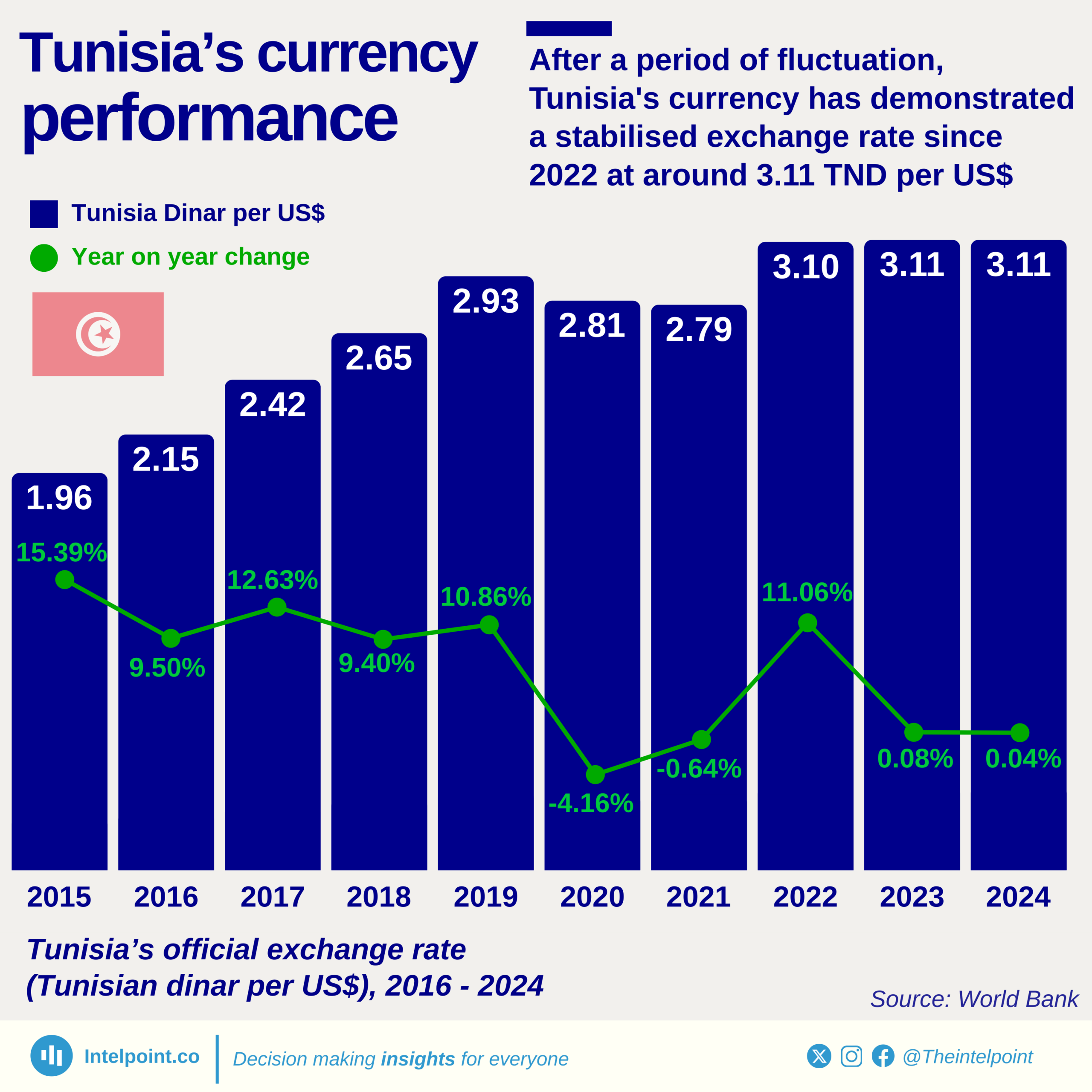

The Tunisian dinar stood at TND 2.15 per US$ in 2016 and has since depreciated to TND 3.11 per US$ in 2024.

Between 2016 and 2019, the dinar saw a strong depreciation.

2020 marked a turning point with a 4.16% appreciation, the first notable currency strengthening in the period observed.

From 2022 onward, the exchange rate has stabilised closely around TND 3.10 to TND 3.11 per US$, with minimal yearly changes of 0.08% and 0.04%.

The largest year-on-year depreciation occurred in 2017 with a 12.63% change.

Despite the earlier years of high volatility, Tunisia’s currency performance in the last three years suggests better monetary management and external stability.

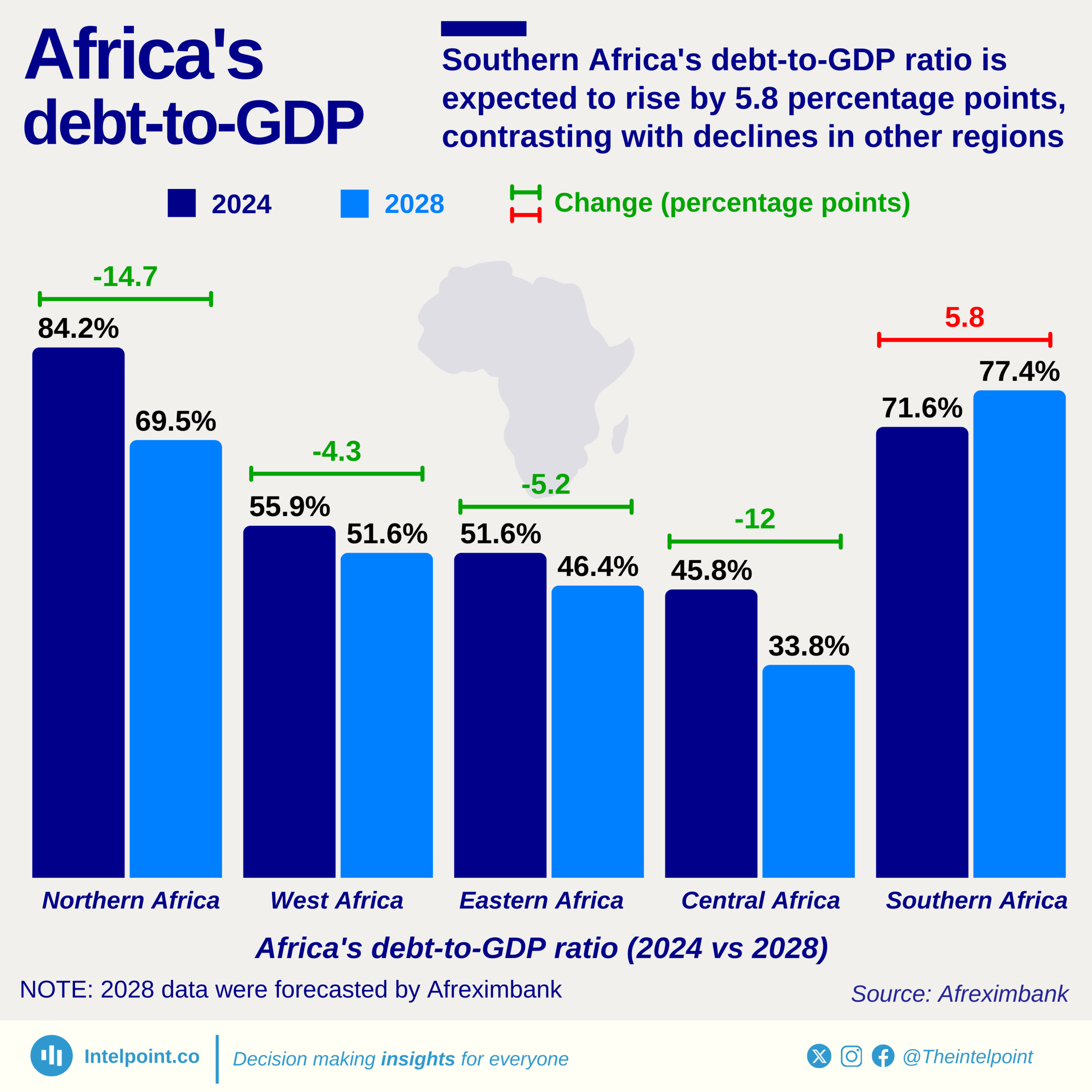

Unlike other regions, Southern Africa’s debt-to-GDP ratio is expected to increase by 5.8 percentage points, reaching 77.4% by 2028.

Northern Africa is set to achieve the largest debt-to-GDP decline of 14.7 percentage points, from 84.2% to 69.5%, indicating significant fiscal adjustments.

Central Africa is expected to see a 12 percentage point drop, reducing its debt-to-GDP ratio from 45.8% to 33.8%.

West Africa’s debt-to-GDP ratio is projected to fall by 4.3 percentage points, while Eastern Africa is expected to drop by 5.2 percentage points, both showing signs of improved debt management.

Even with the projected declines, some regions like Northern Africa (69.5%) and Southern Africa (77.4%) will still have high debt burdens compared to others like Central Africa (33.8%).

The declining debt-to-GDP ratios in most regions suggest either economic expansion or strategic debt control, but Southern Africa’s increase indicates potential fiscal stress.

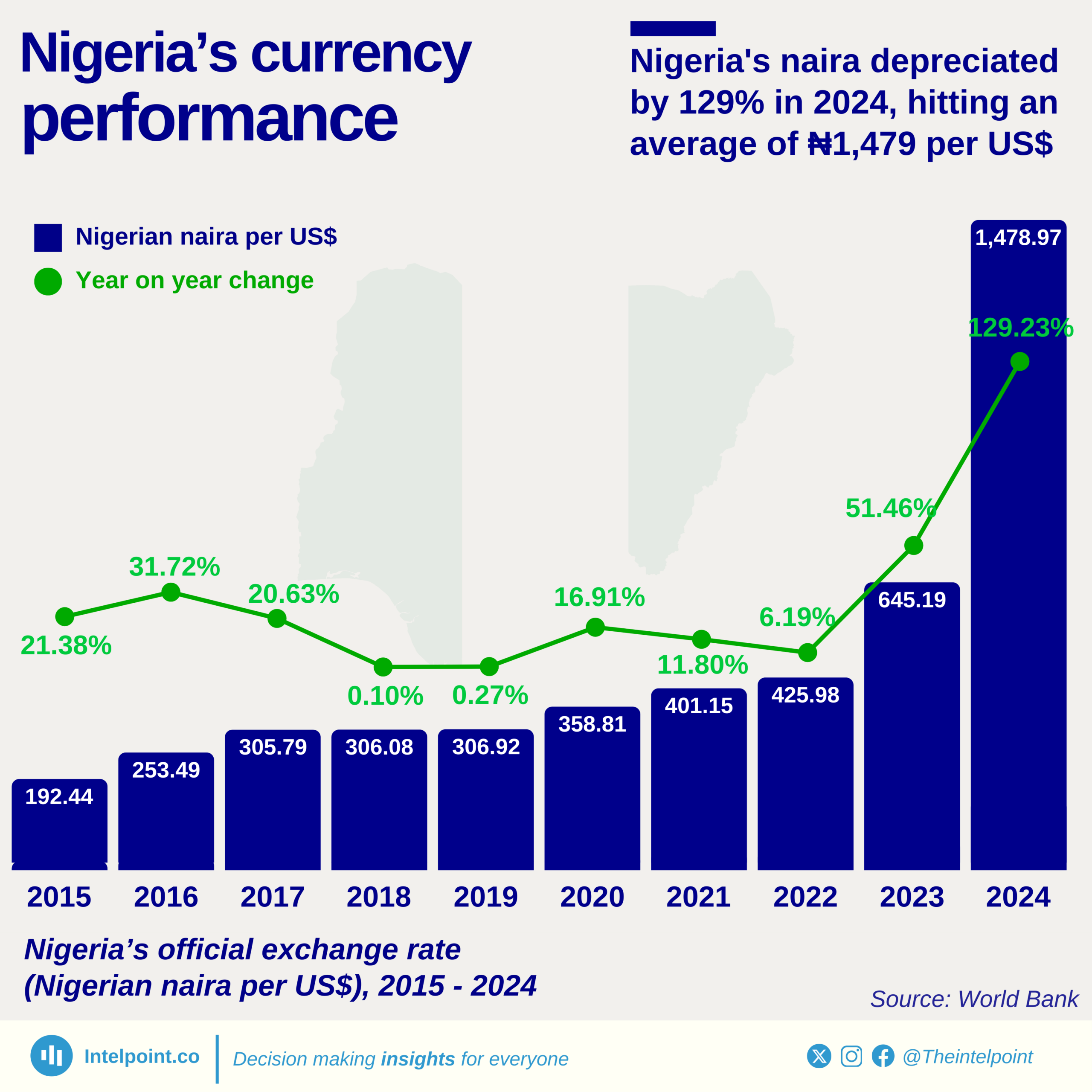

When Olusegun Obasanjo took office in 1999, the exchange rate was ₦97 to $1; it was ₦128 under Yar'Adua in 2007. During Jonathan's tenure in 2010 it was ₦151 while it was ₦199 when Buhari was in office.

Despite efforts to let market forces decide the rate, the naira continues to weaken. Will the current administration turn things around soon?

Can’t find what you’re looking for? Please fill the form below