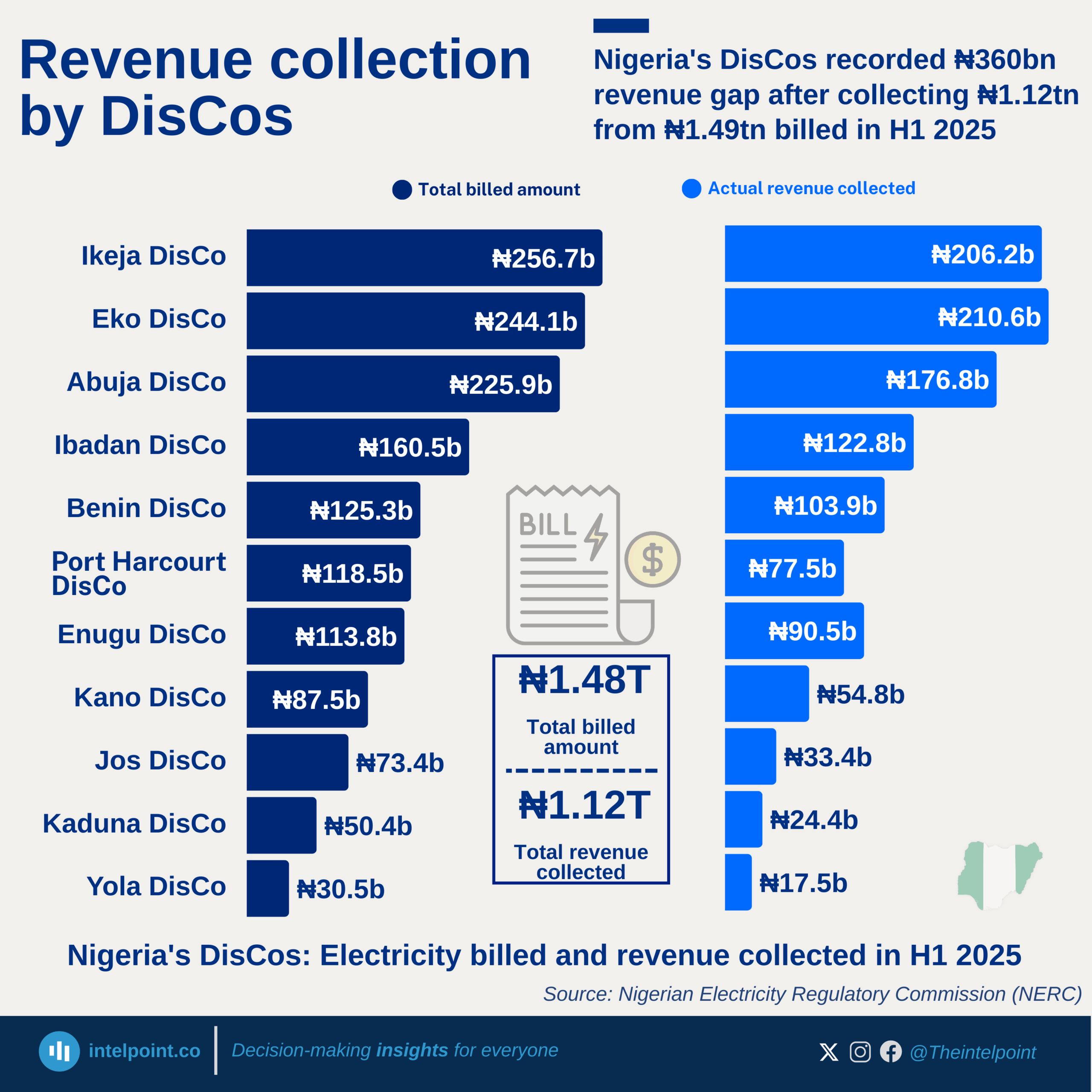

DisCos billed approximately ₦1.49 trillion but collected only ₦1.12 trillion in H1 2025.

Ikeja and Eko DisCos generated the highest revenues, collecting ₦206.22 billion and ₦210.59 billion, respectively.

Revenue collection gaps remain significant, with Jos, Kaduna, and Yola posting the weakest collection performances.

The wide gap between billings and actual collections suggests persistent challenges in customer payment compliance, metering, and distribution efficiency.