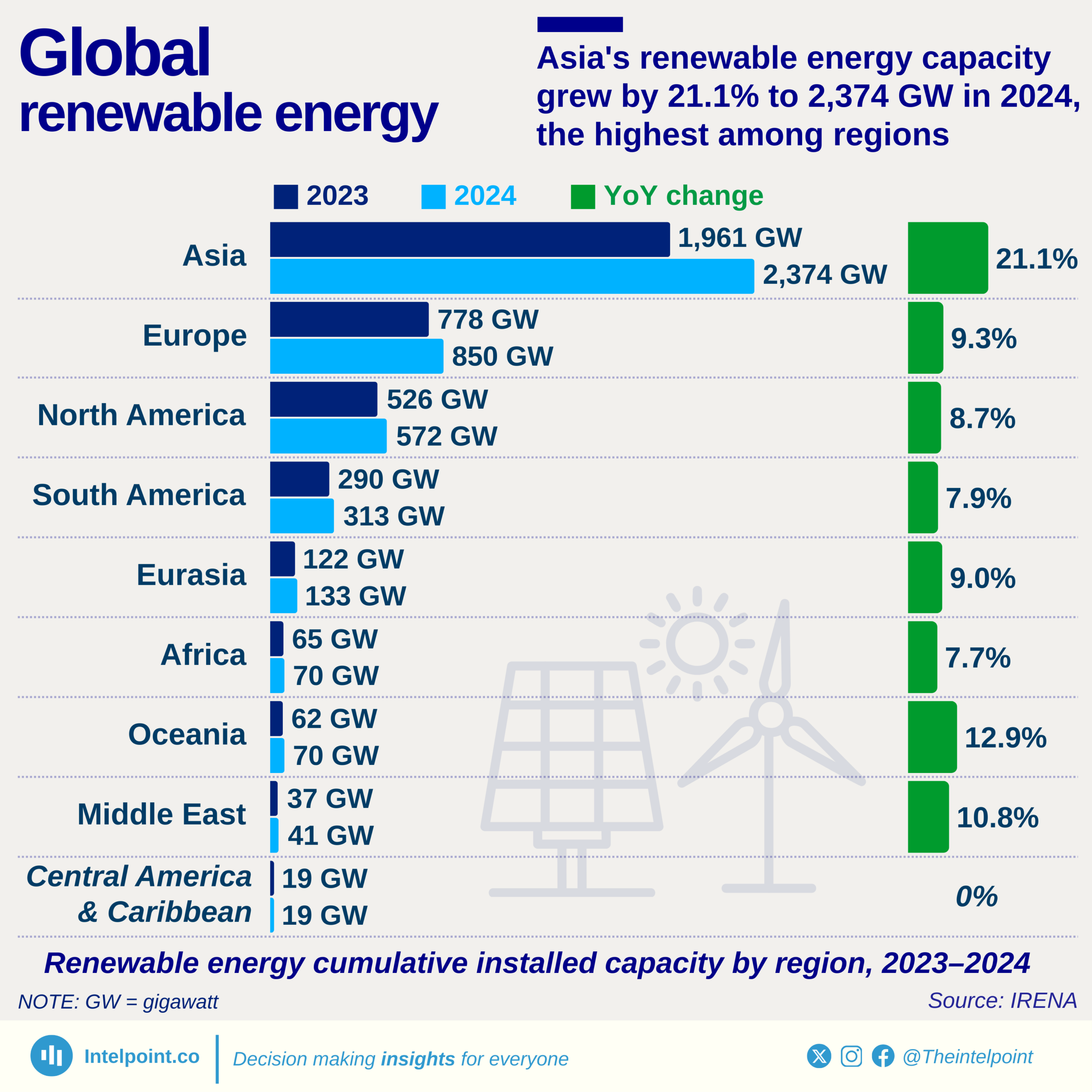

Asia has taken the lead in global renewable energy growth, recording a massive 21.1% increase in installed capacity between 2023 and 2024. This surge pushed its total to 2,374 GW, far ahead of every other region. The scale of Asia’s growth highlights its aggressive push towards clean energy, driven by rapid industrialisation, policy support, and the urgency to cut reliance on fossil fuels.

In comparison, Europe and North America maintained growth, adding 72 GW and 46 GW, respectively, though their year-on-year growth rates—9.3% and 8.7%, respectively—are far behind Asia’s pace. Regions like Oceania and the Middle East, although smaller in total capacity, stood out with double-digit growth rates, demonstrating that even emerging players are increasing their adoption of renewable energy. Meanwhile, Africa and South America posted modest gains, reflecting progress but underscoring the need for further investment and infrastructure to harness their vast renewable potential.