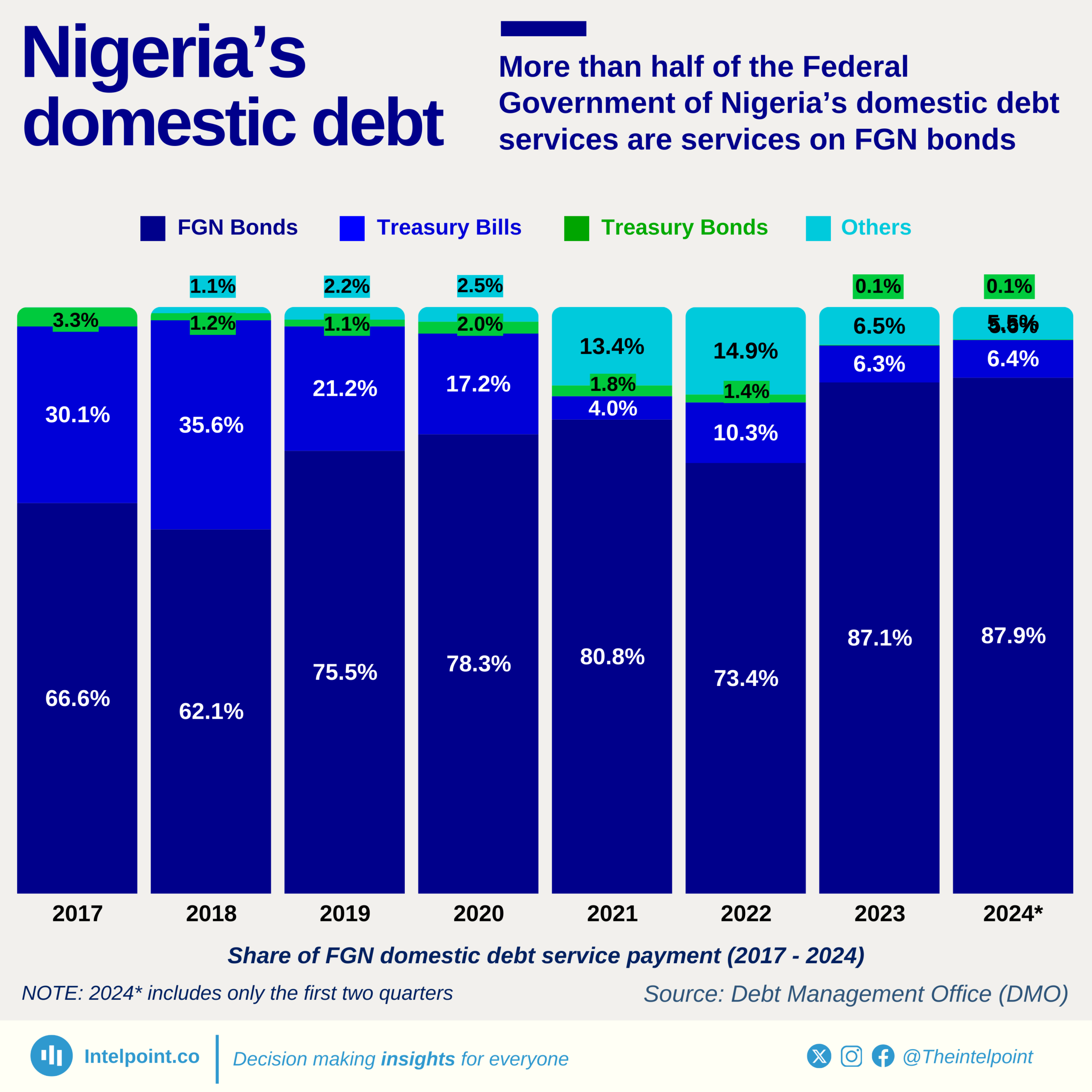

Nigeria’s domestic debt service structure has become increasingly dominated by FGN Bonds, which accounted for a staggering 87.9% of total payments in 2024. This is a sharp increase from 66.6% in 2017, reflecting a gradual shift in the government’s debt servicing strategy. The reliance on FGN Bonds has significantly reduced the share of Treasury Bills and Treasury Bonds, which played a more significant role in earlier years.

Between 2017 and 2024, Treasury Bills' share plummeted from 30.1% to just 6.4%, while Treasury Bonds, which peaked at 14.9% in 2022, now make up only 5.6% of the total.