Key Takeaways:

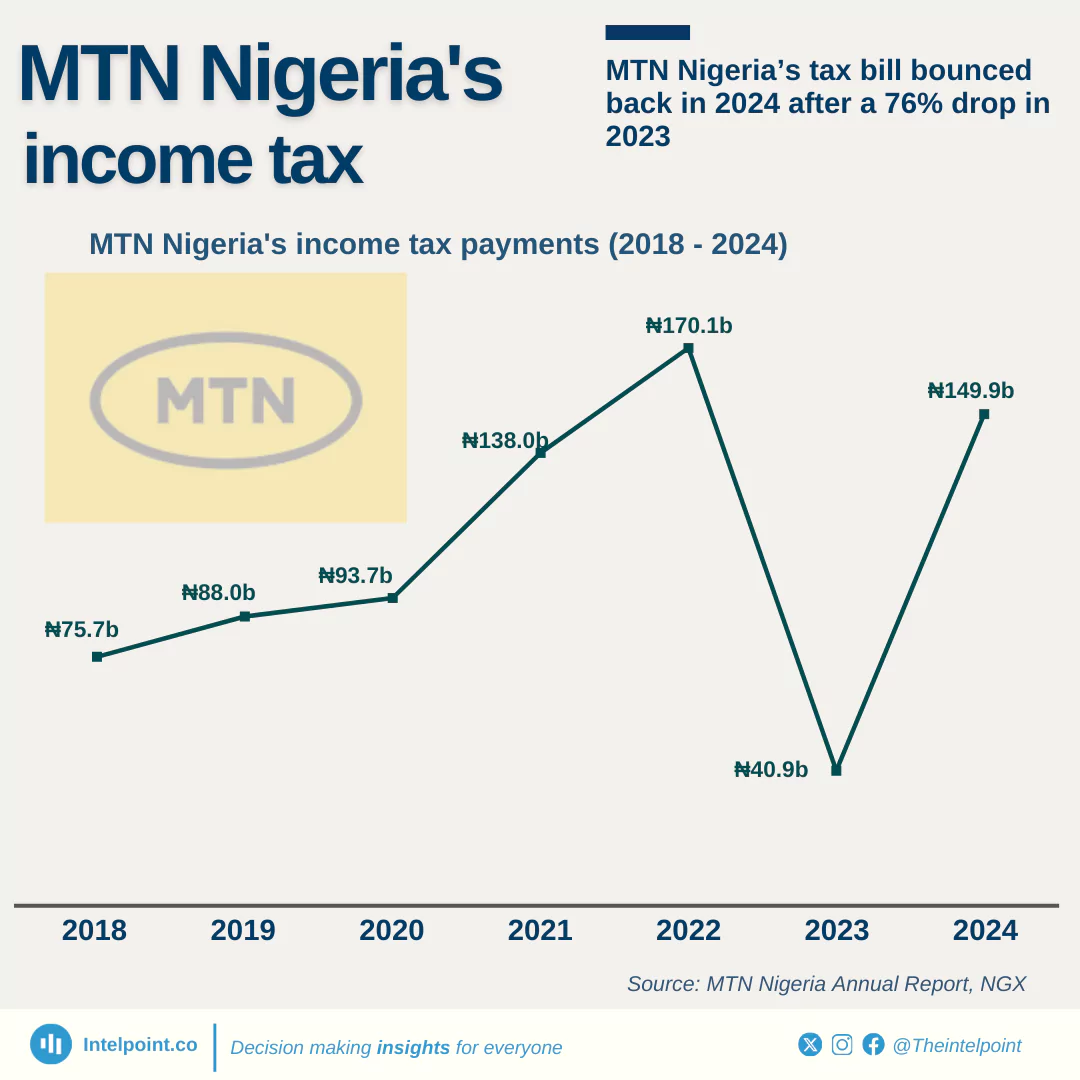

Over recent years, MTN has witnessed considerable fluctuations in its income tax payments, reflecting growth and difficulties. From 2018 to 2022, the firm's tax payments consistently increased. In 2018, MTN's tax payment was ₦75.66 billion, and by 2021, it surged to ₦138.03 billion. The positive trajectory persisted in 2022, with taxes climbing to ₦170.1 billion.

However, in 2023, MTN encountered a notable decline in its tax payments arising from the devaluation of the naira. Despite the decline, the company's income tax payments rebounded to ₦149.89 billion in 2024, primarily due to improved revenue growth despite the challenges of foreign exchange losses.