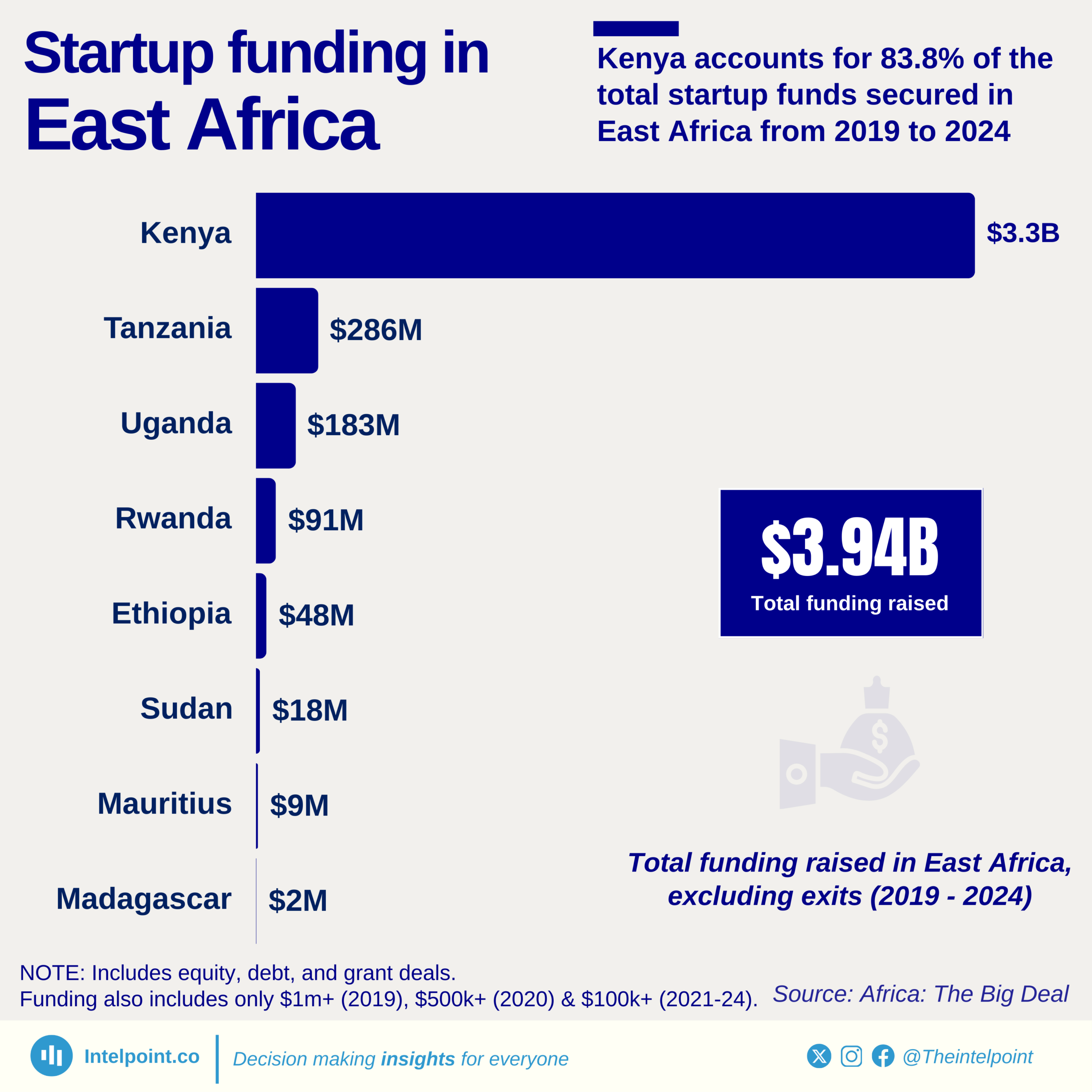

Kenya accounts for 83.8% of the total startup funds secured in East Africa from 2019 to 2024

Key takeaways:

Kenya is the absolute leader in startup funding, with $3.3 billion raised in the past six years.

The rest of East Africa is way behind, with Tanzania ($286M), Uganda ($183M), and Rwanda ($91M) being the next in line. But collectively, they don’t even match 20% of the funding Kenya received.

The total funding raised across East Africa from 2019 to 2024 is $3.94 billion, which means Kenyan startups alone secured more than 8 out of every 10 dollars invested in the region.

Investor confidence is highly concentrated in Kenya, largely due to its well-developed venture capital ecosystem, startup accelerators, and government support for innovation.

Kenyan startups secured an astonishing $3.3 billion, capturing 83.8% of all funds raised in the region. This leaves the other East African countries scrambling for the remaining 16.2%, with Tanzania ($286M) and Uganda ($183M) trailing far behind.

What’s driving this massive funding gap? Kenya’s startup ecosystem benefits from stronger investor networks, a vibrant tech culture, and a policy environment that encourages growth. Nairobi, often referred to as "Silicon Savannah," has become a magnet for global venture capitalists while startups in neighbouring countries struggle to attract similar attention.

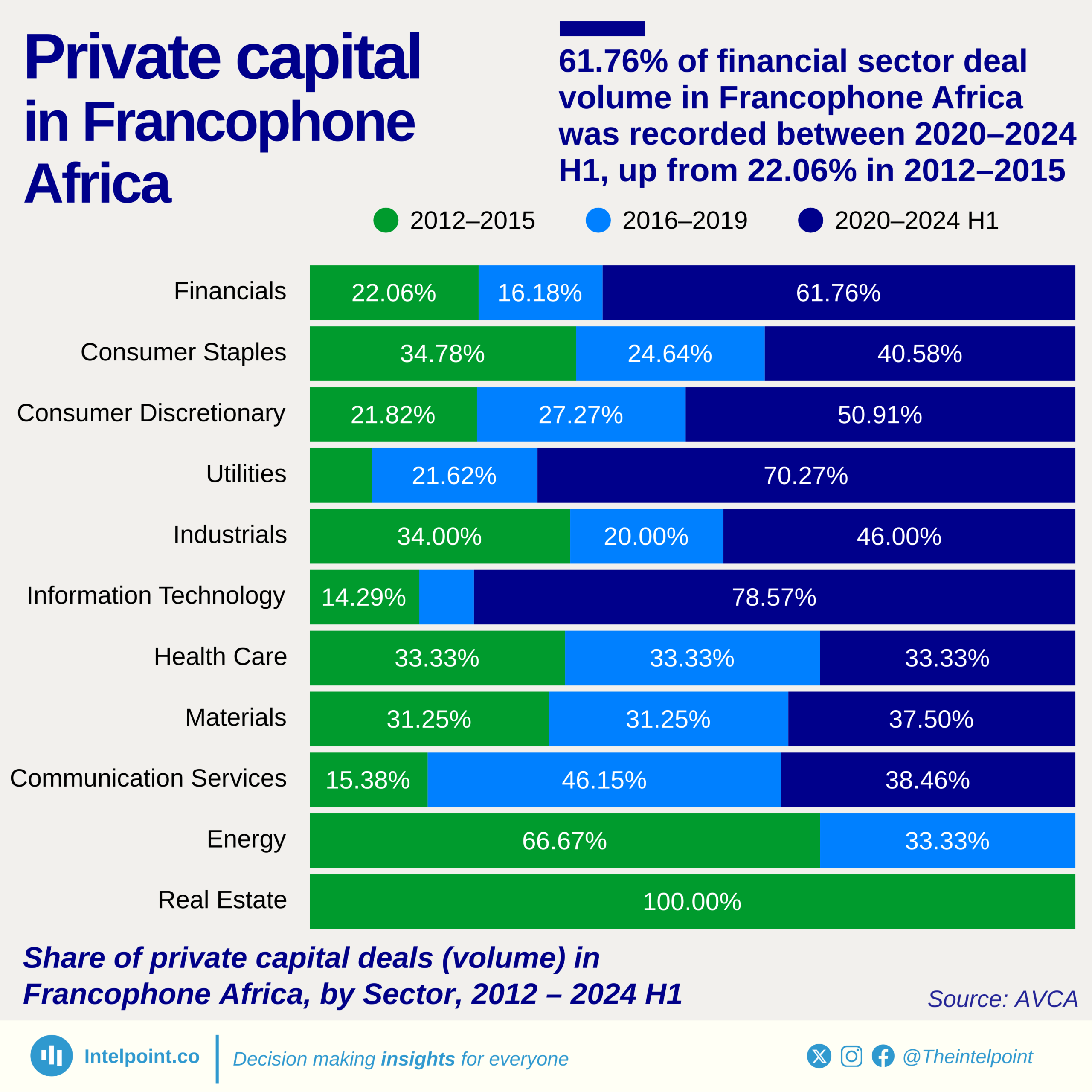

Between 2020–2024 H1, 40.58% and 50.91% of deal volume went to consumer staples and consumer discretionary respectively, showing that everyday goods and lifestyle products are fast becoming investment magnets.

The utilities sector deal volume exploded in recent years, jumping from 21.62% in 2016–2019 to 70.27% in 2020–2024 H1, an indication that basic infrastructure services like energy, water, and power are now central to investment strategies.

78.57% of all deal volume in the information technology sector happened in the most recent period, suggesting that digital solutions and tech platforms are increasingly being backed by private capital.

The industrials sector also bounced back, with 46% of its deal volume coming in the 2020–2024 period.

Energy sector investment dropped from 66.67% to 33.33%, and real estate recorded no new deals after 2015.

Health care remained consistent across all three periods, securing exactly 33.33% of the deal volume each time, highlighting its stability, even if not standout growth.

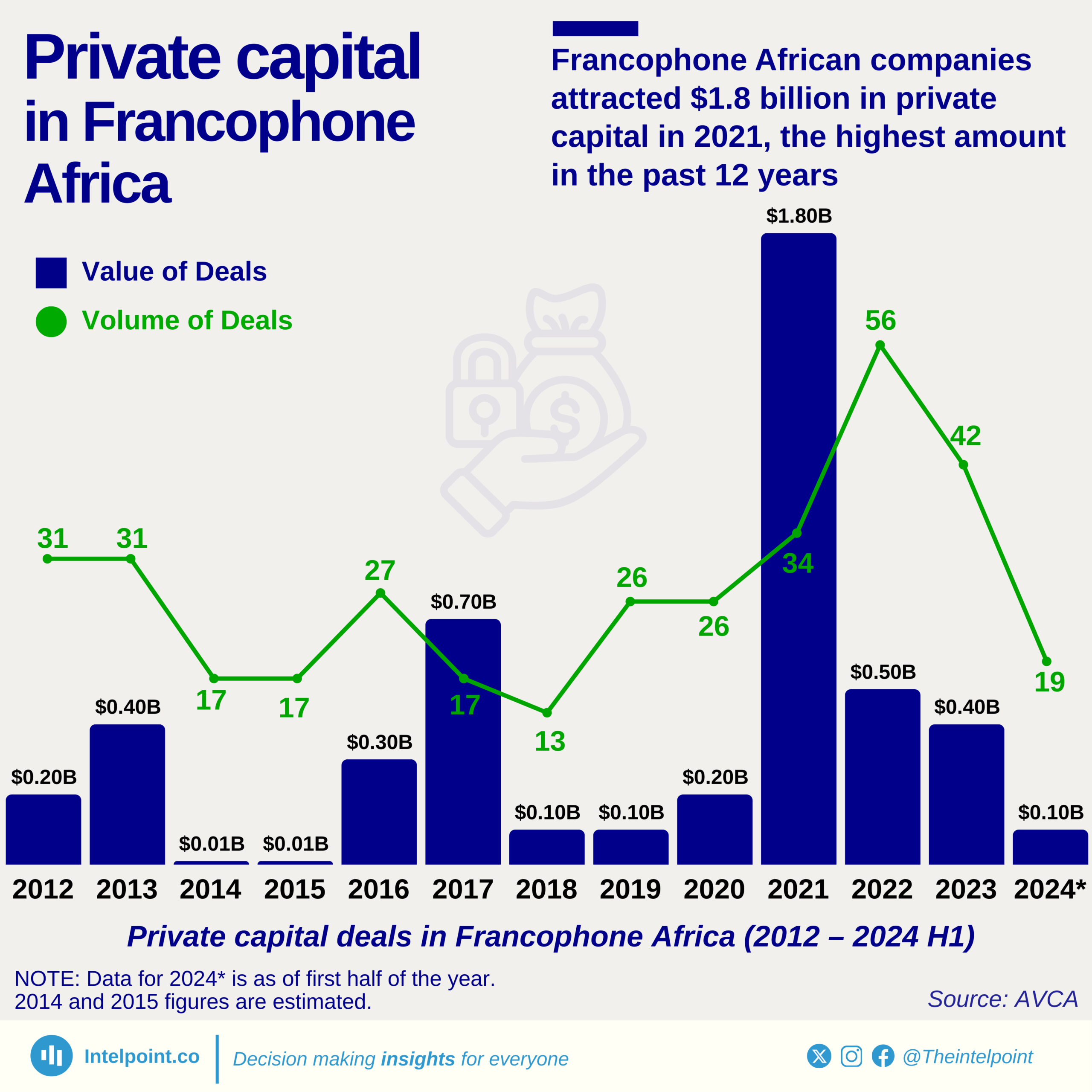

Francophone Africa attracted $1.8 billion in private capital in 2021, about 9x the previous year (2020).

That same year saw 34 deals, which is quite high when compared to some other years, indicating strong investor confidence.

In 2024, deal value amounted to just $0.1 billion, and deal volume to 19, pointing to a significant cooling in activity.

Between 2012 and 2015, the region saw low deal values, with both 2014 and 2015 recording just $0.01 billion in investments.

A notable spike occurred in 2017 with $0.7 billion invested across 17 deals, marking the first major surge before 2021's breakout.

Deal counts haven’t always aligned with capital volume. For instance, 2023 had 42 deals but only $0.4B, suggesting a trend of smaller-sized investments.