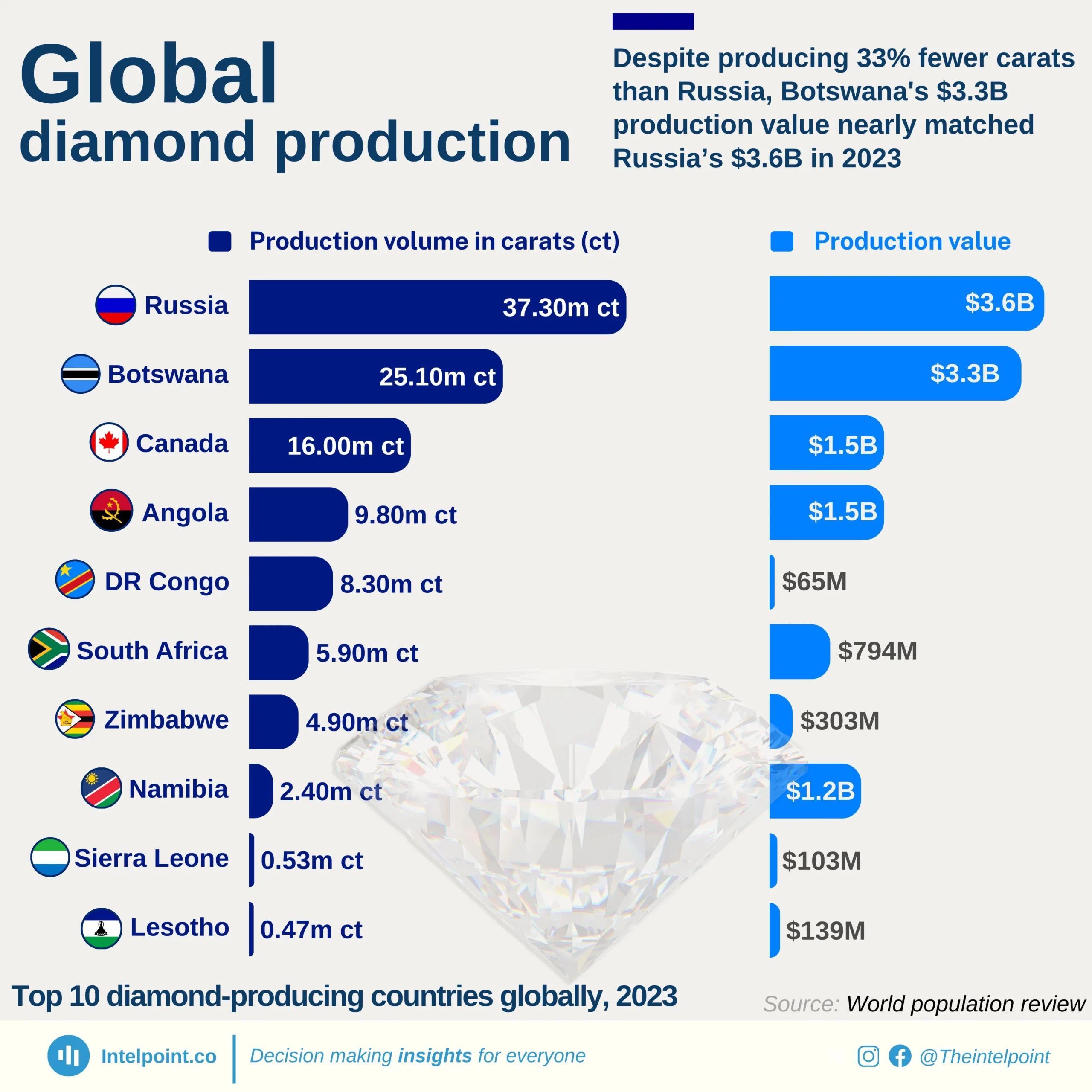

In 2023, the global diamond market continued to show a fascinating split between volume and value. Russia retained its crown as the world’s largest producer by carats, mining 37.3 million ct, yet Botswana proved nearly as lucrative, generating $3.3 billion from just 25.1 million ct, underscoring the premium quality of its stones. Africa remains the diamond powerhouse, with 8 countries in the top 10, led by Angola (9.8M ct, $1.5B) and DR Congo (8.3M ct, $65M) — the latter revealing how industrial-grade stones can drag down export value. Meanwhile, Namibia and Lesotho demonstrated that size doesn’t always matter in diamonds; with relatively small outputs, they delivered outsized earnings per carat. Together, these trends highlight the duality of the diamond trade: sheer volume vs. premium value.