Key takeaways:

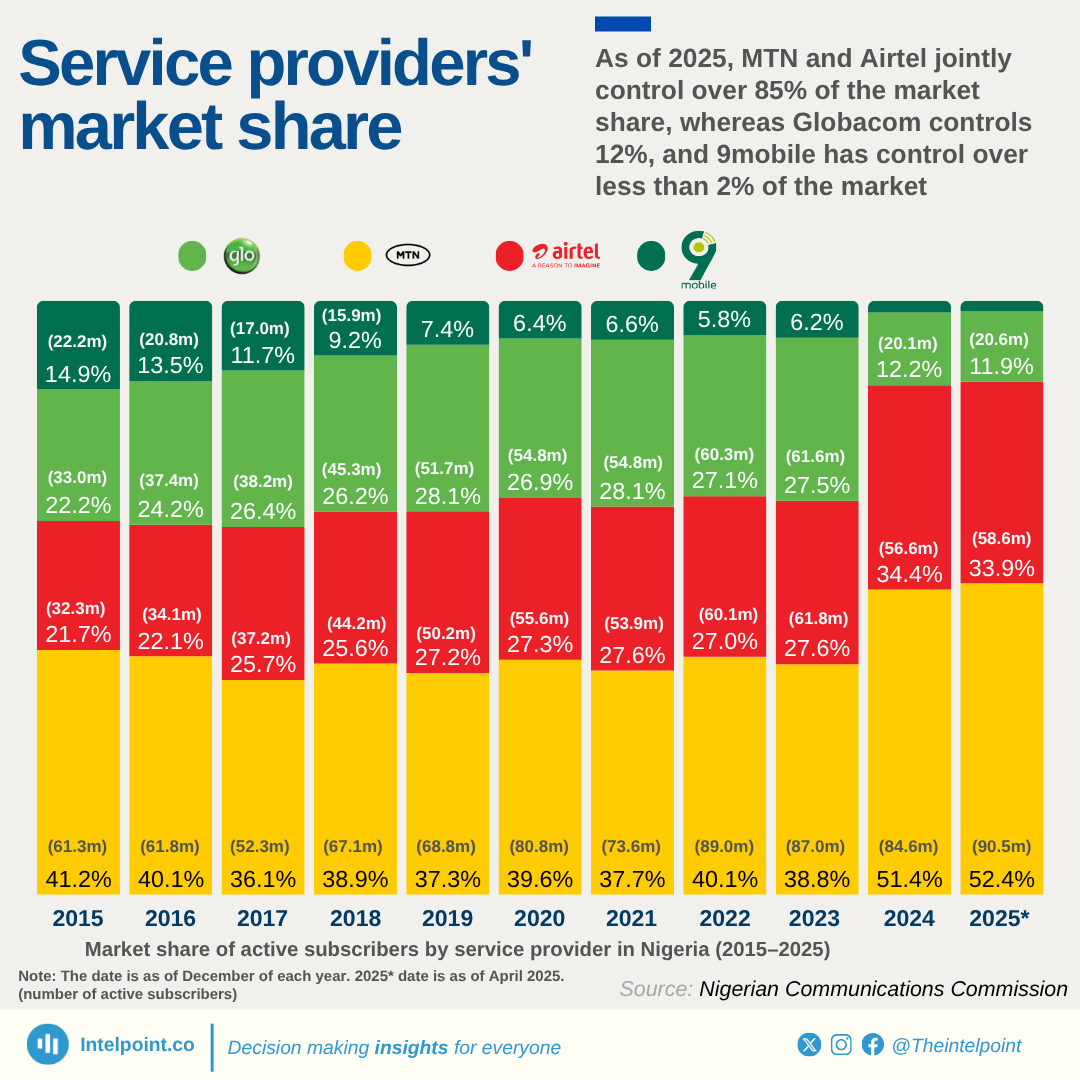

Over the last decade, Nigeria’s telecommunications sector has undergone significant market changes, with MTN solidifying its position as the undisputed leader. As of April 2025, MTN commands 52% of all active telephony subscribers, a significant rise from 41% in 2015. Its subscriber base grew from 61.3 million to over 90.5 million, indicating good customer retention and network expansion.

Airtel’s market share increased from 22% to 34%, bringing its subscriber base to approximately 58.6 million by April 2025. This upward trend highlights Airtel's growth in the sector, especially in recent years.

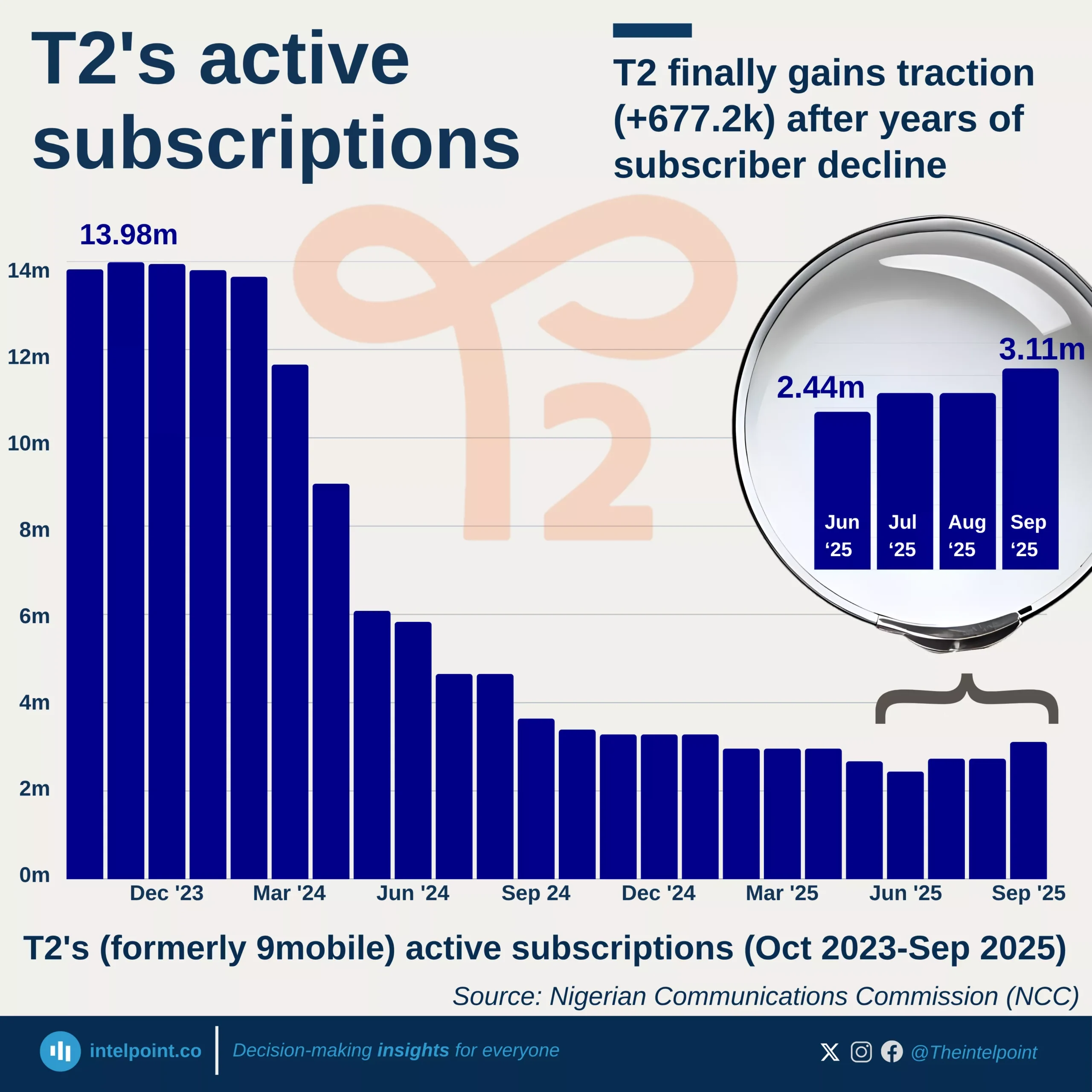

Globacom, whose market share had been constant at 26-28% for many years, has seen its grip on the market weaken sharply. By April 2025, its share had dropped to 12%, with subscriber numbers at roughly 20.6 million. On the more drastic side, from a 15% share in 2015, 9mobile's market share dropped to just 2% in 2025, with active users falling from more than 22 million to around 3 million.