Home

Reports

Blog

Insights

About Us

Subscribe

Home

Reports

Blog

Insights

About Us

Bite-sized

Insights

about

Providing you with data-based insights about things happening around you.

Nigeria

Trade

Debt

Economy

GDP

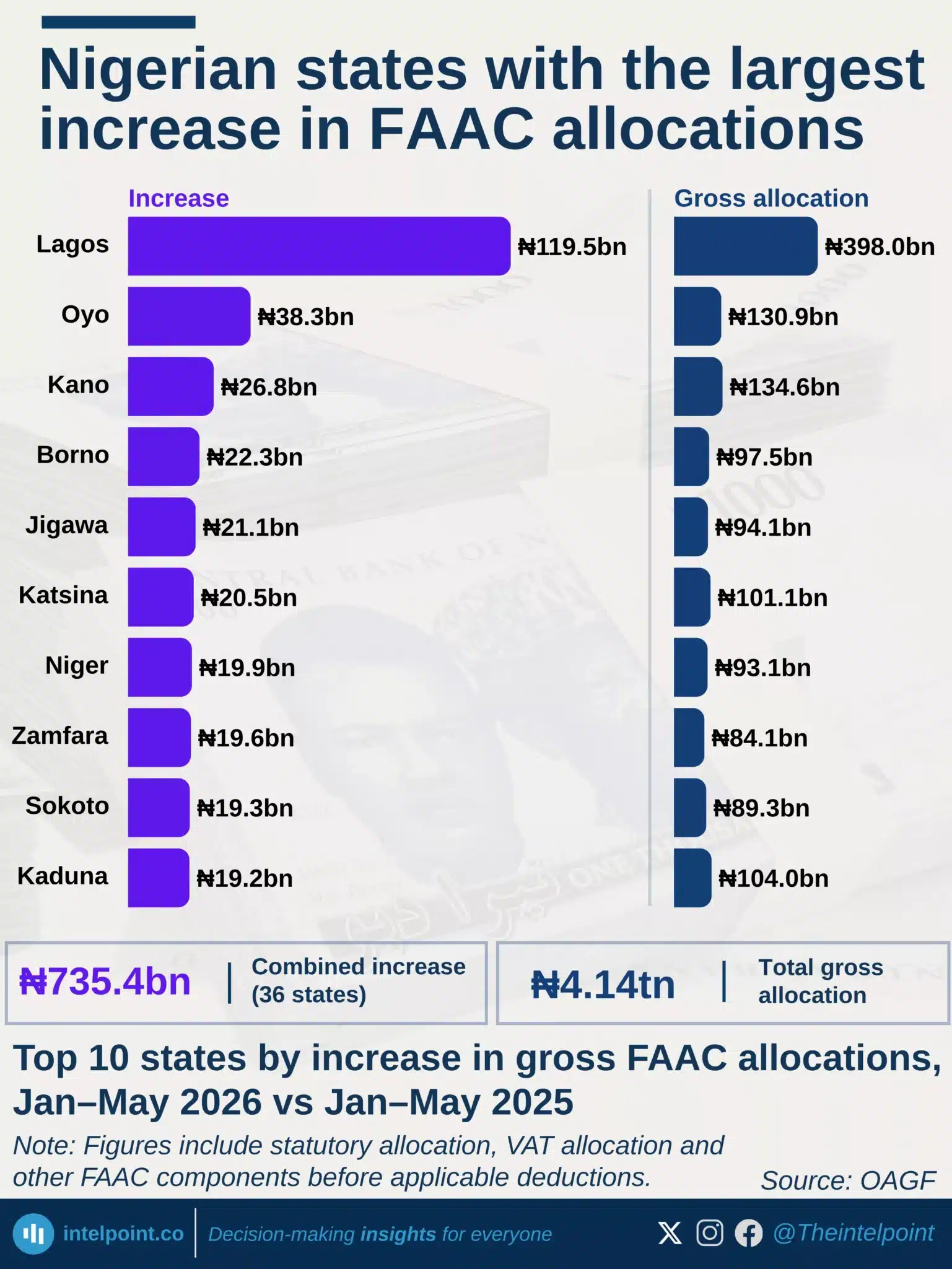

Nigerian states with the largest increase in FAAC allocations

Nigeria's 36 states received a combined ₦4.14 trillion in FAAC allocations in Jan-May 2026, up ₦735.4 billion (21.6%) from a year earlier.

Thirty-five states received higher allocations than a year earlier, while Rivers was the only state to record a decline (₦7.15 billion).

Lagos recorded the largest increase in FAAC allocations (₦119.5 billion), more than three times the increase recorded by Oyo (₦38.3 billion).

Oyo, Kano, Borno, and Jigawa rounded out the top five states with the largest increases in FAAC allocations.

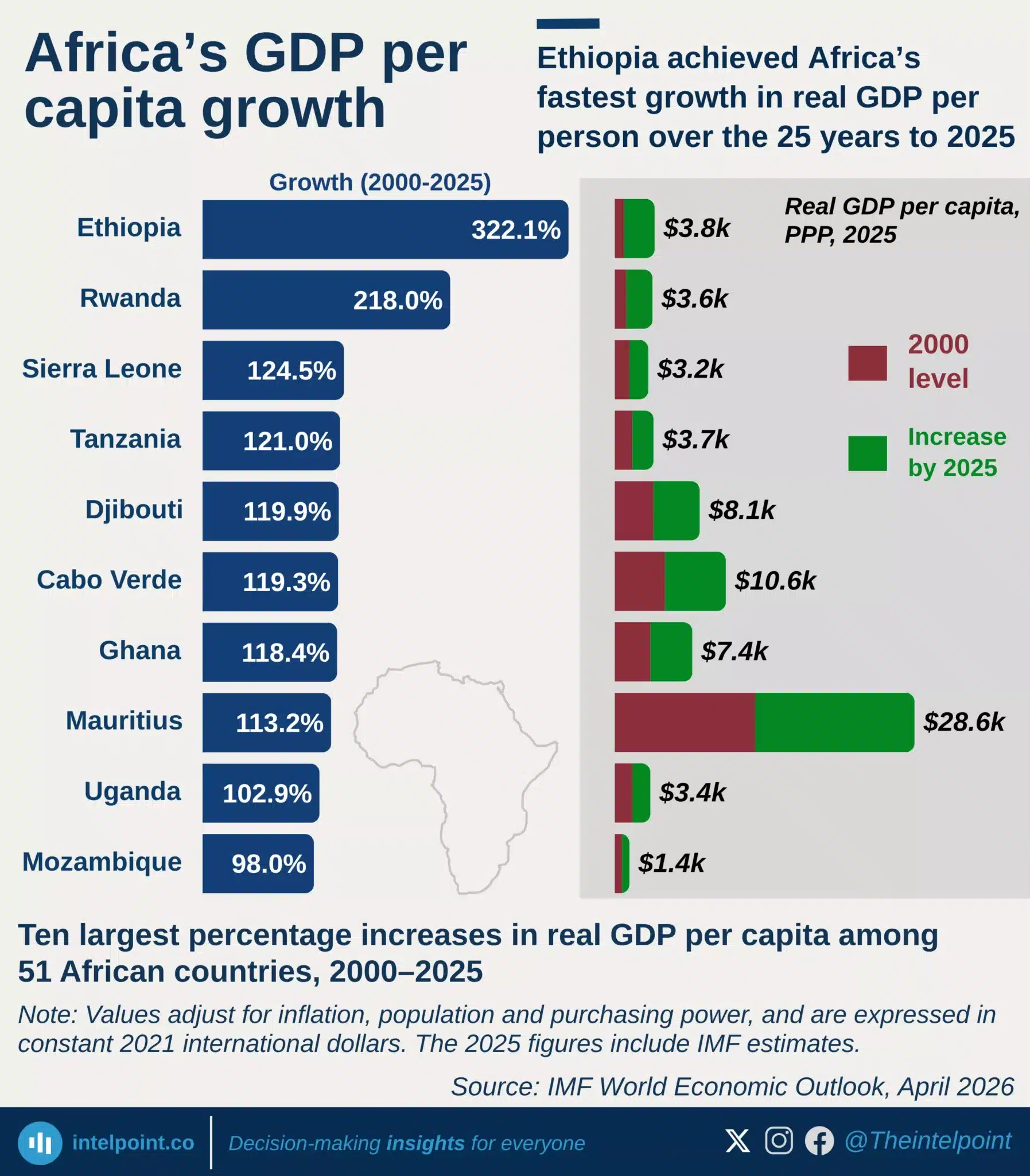

Ethiopia achieved Africa’s fastest growth in real GDP per person over the 25 years to 2025

Ethiopia recorded Africa's fastest real GDP per capita growth between 2000 and 2025.

Rwanda ranked second, while Sierra Leone, Tanzania and Djibouti completed the top five.

Ethiopia's real GDP per capita rose 322%, from $910 to $3,843.

Mauritius recorded Africa's largest absolute gain in real GDP per capita.

Nigeria ranked 15th, with real GDP per capita increasing 76.7%.

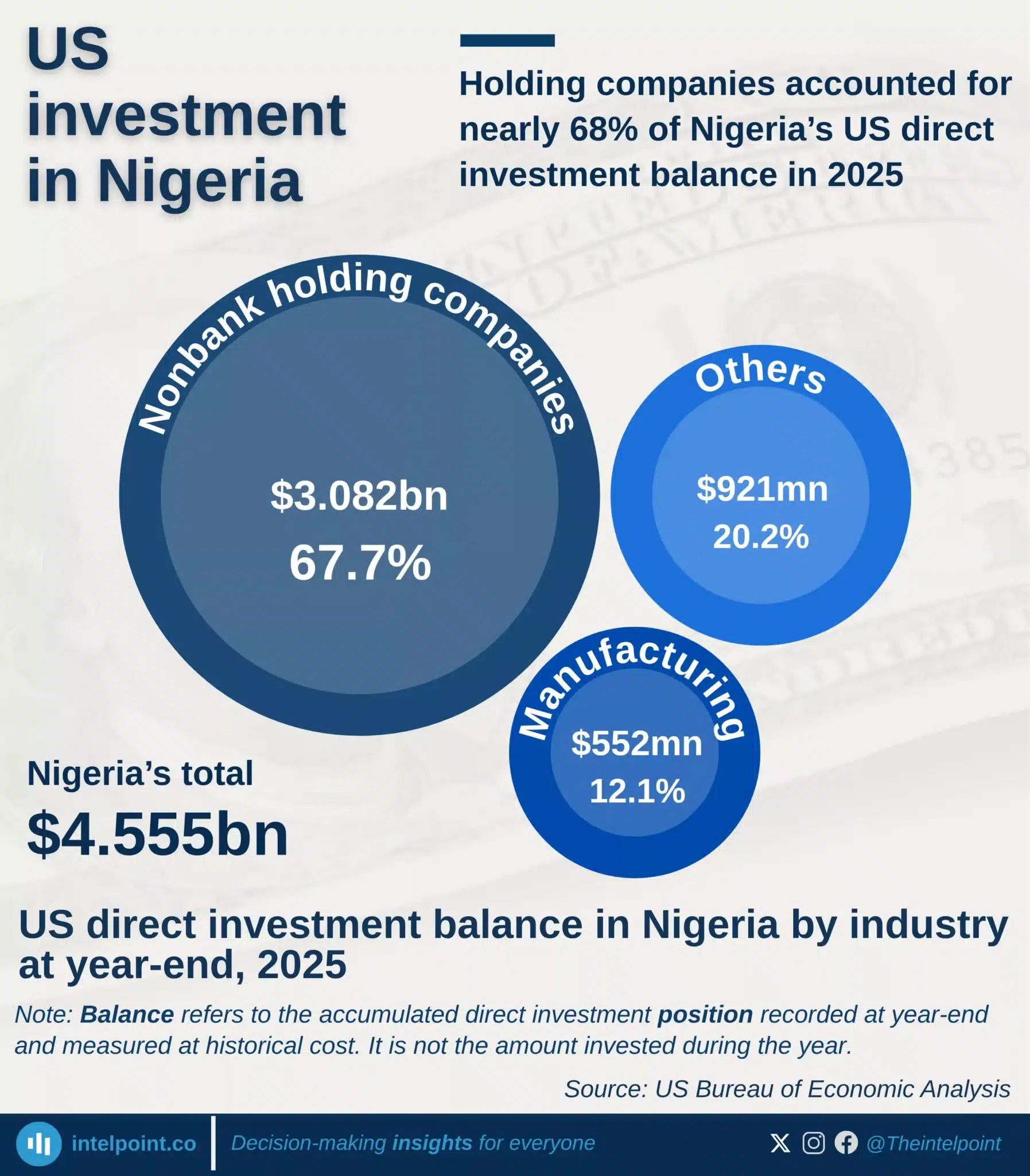

Holding companies accounted for nearly 68% of Nigeria’s US direct investment balance in 2025

Nigeria held Africa’s fourth-largest US direct investment balance in 2025, at $4.56 billion.

The balance fell by $1.98 billion from $6.54 billion in 2024, a decline of 30.3%.

Nonbank holding companies accounted for $3.08 billion, or 67.7% of Nigeria’s total balance.

Manufacturing represented $552 million, or 12.1%, while other industries accounted for $921 million.

Holding-company assets may ultimately be deployed in other sectors, so the classification does not show their final use.

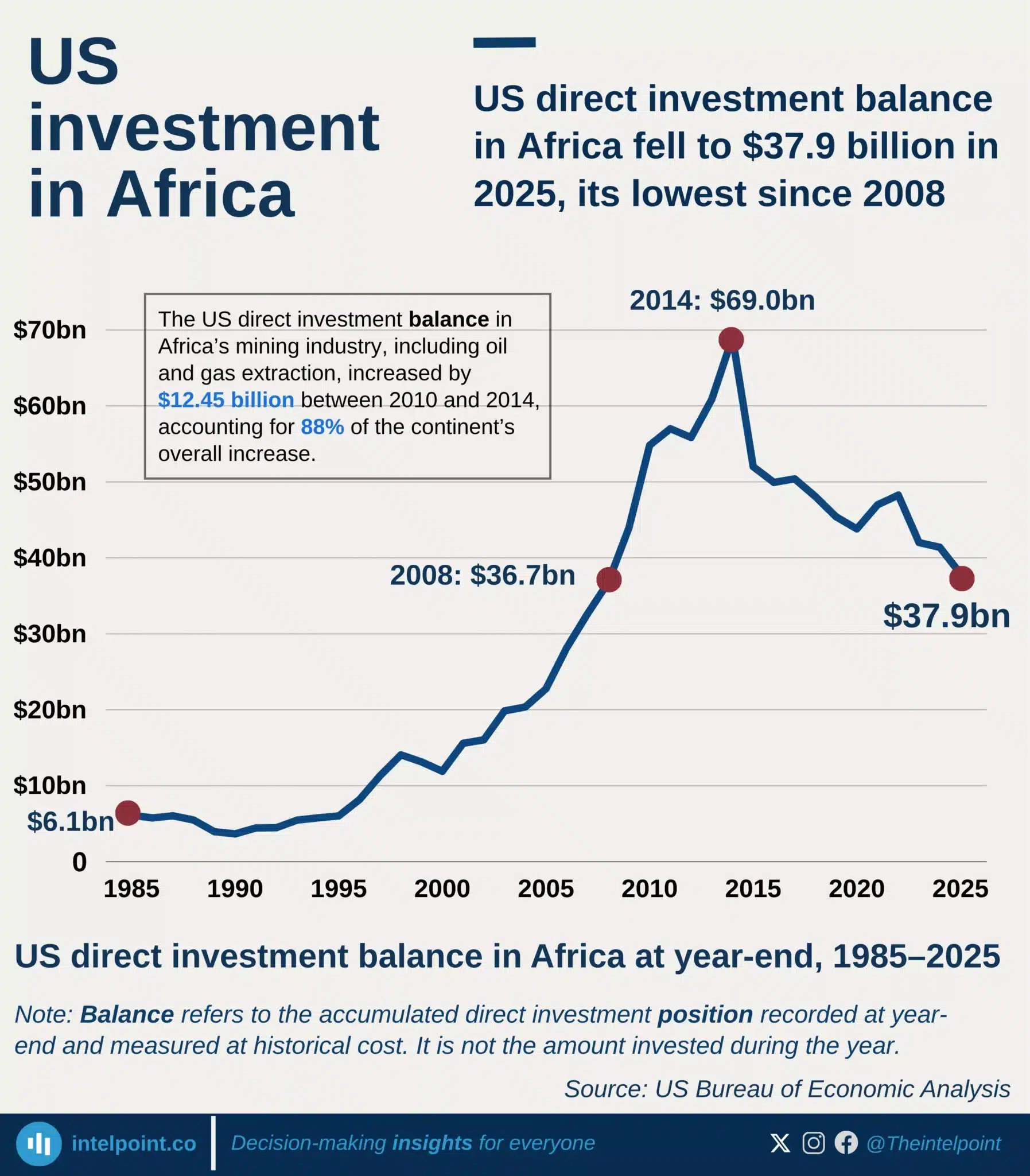

US direct investment balance in Africa fell to $37.9 billion in 2025, its lowest since 2008

US direct investment in Africa peaked at $69 billion in 2014 after expanding rapidly from the mid-2000s.

By 2025, the balance had fallen 45.1% from its peak to $37.9 billion, its lowest since 2008.

Mining drove the cycle, accounting for 88% of the 2010–2014 increase and 97% of the subsequent decline.

Africa’s share of the global US direct investment balance remained below 3% throughout 1985–2025.

The post-2014 decline was interrupted by brief recoveries in 2017 and 2021–2022.

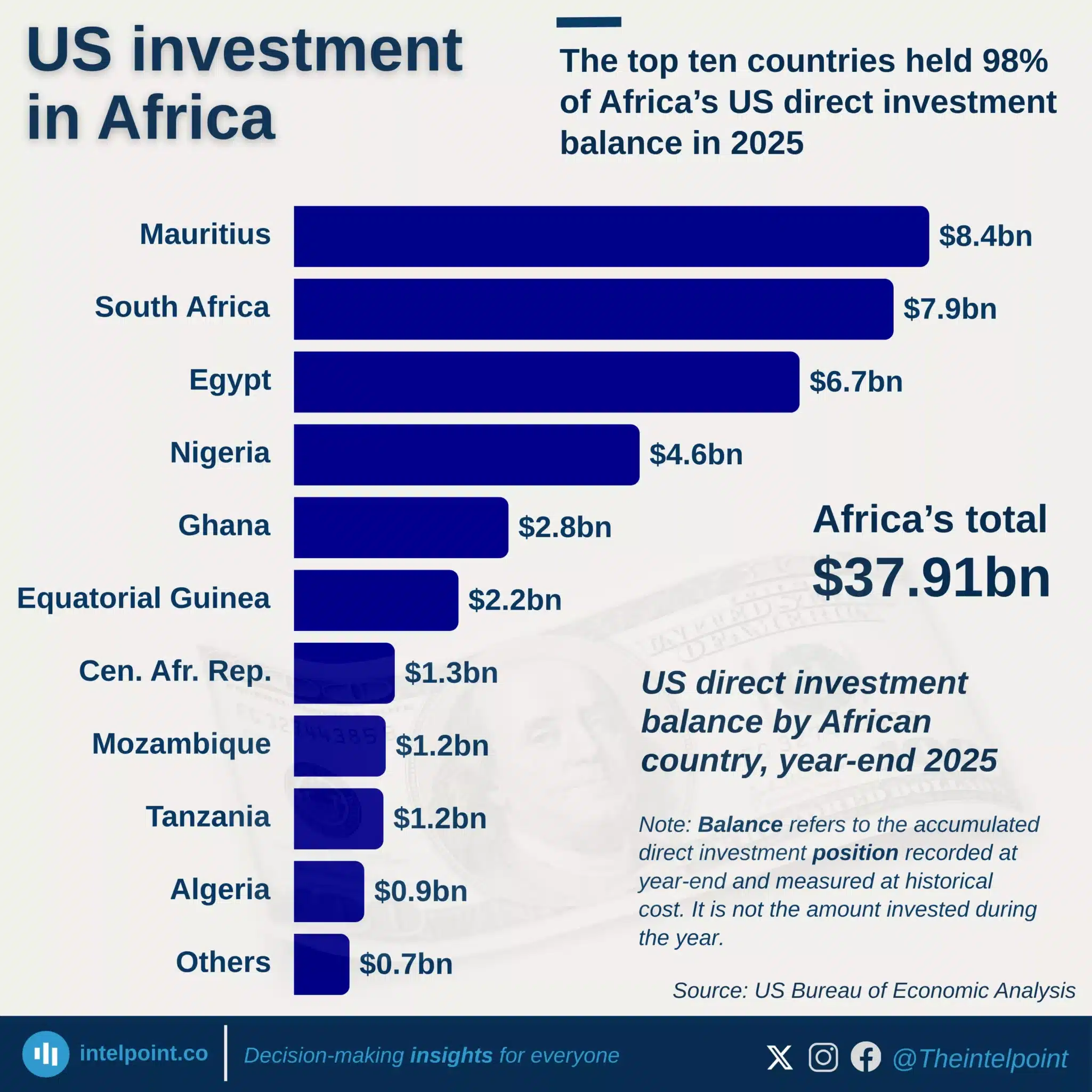

The top ten countries held 98% of Africa’s US direct investment balance in 2025

Mauritius held Africa’s largest US direct investment balance in 2025, at $8.4 billion.

South Africa followed with $7.9 billion, ahead of Egypt’s $6.7 billion and Nigeria’s $4.6 billion.

Africa’s total balance fell by 8.4% to $37.91 billion, its third consecutive annual decline.

The top ten countries held 98% of Africa’s total, leaving only $0.7 billion across the rest.

Manufacturing led South Africa’s balance, mining dominated Egypt’s, and holding companies accounted for most of Nigeria’s.

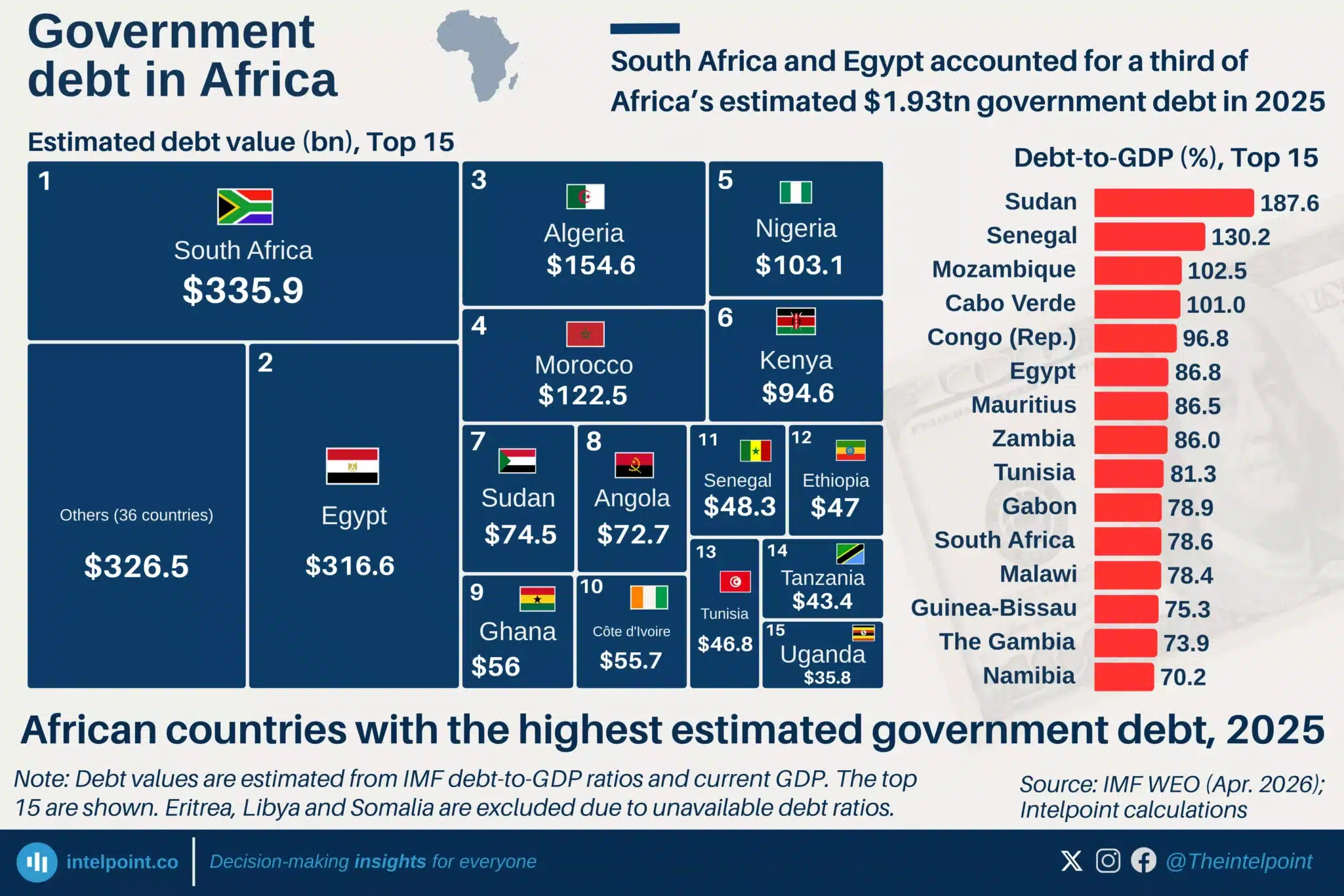

South Africa and Egypt accounted for a third of Africa’s estimated $1.93tn government debt in 2025

Government debt across 51 African countries was estimated at $1.93 trillion in 2025.

South Africa and Egypt had the largest estimated stocks and jointly accounted for 33.8% of the total.

Sudan had the highest debt-to-GDP ratio at 187.6%, followed by Senegal at 130.2%.

The estimates use IMF debt ratios and current-dollar GDP, not national authorities’ reported debt stocks.

Differences in government coverage, instruments and valuation mean the figures are comparable estimates, not fully harmonised official data.

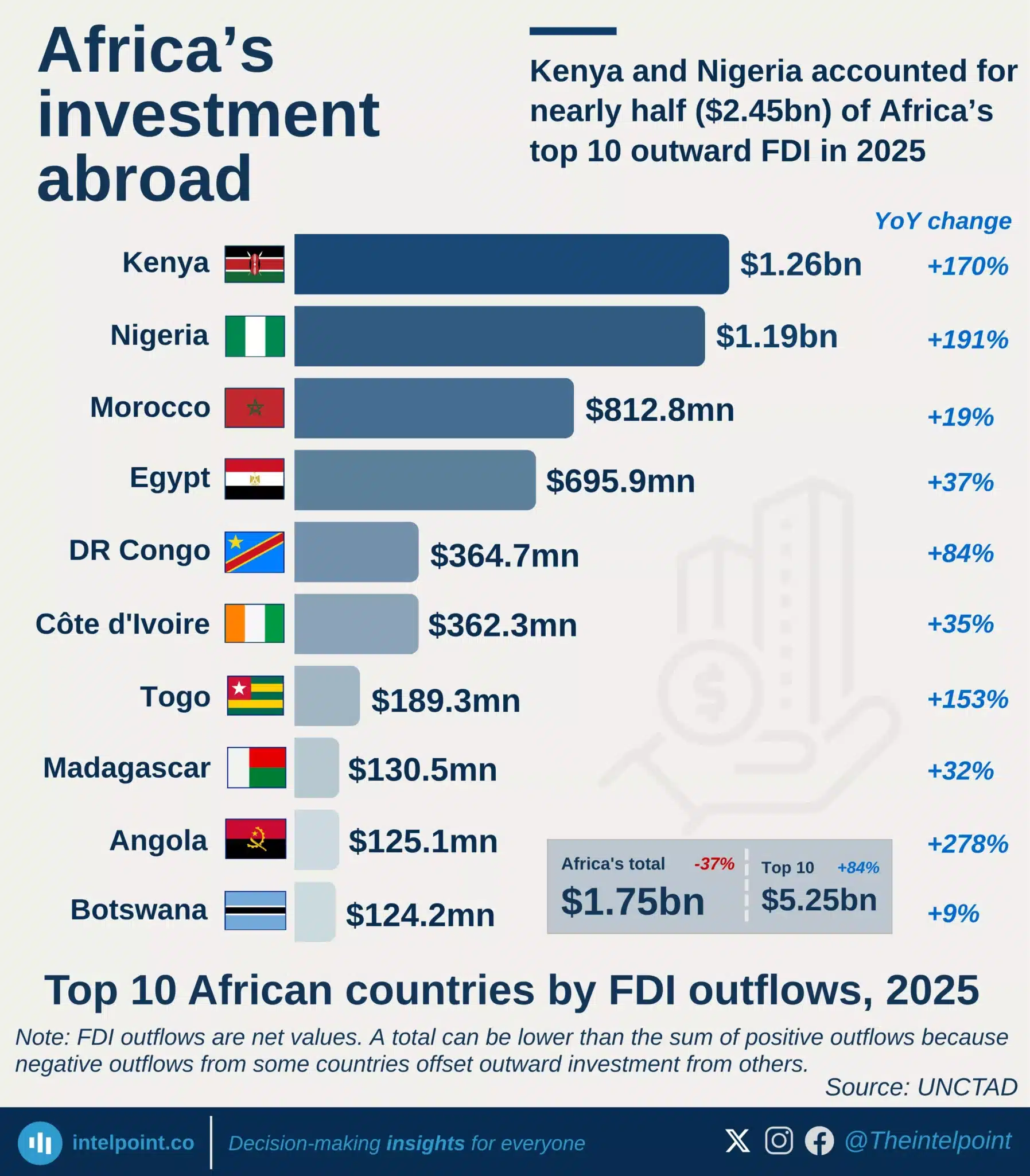

Kenya and Nigeria accounted for nearly half ($2.45bn) of Africa’s top 10 outward FDI in 2025

Kenya led Africa’s outward FDI in 2025, recording $1.26bn.

Nigeria followed closely with $1.19bn, after a 191% increase.

Together, Kenya and Nigeria accounted for $2.45bn of the top 10 total.

Morocco and Egypt completed the top four, with $812.8m and $695.9m.

Angola recorded the fastest growth among the top 10, rising 278%.

Africa’s total outflow was lower because negative outflows offset gains elsewhere.

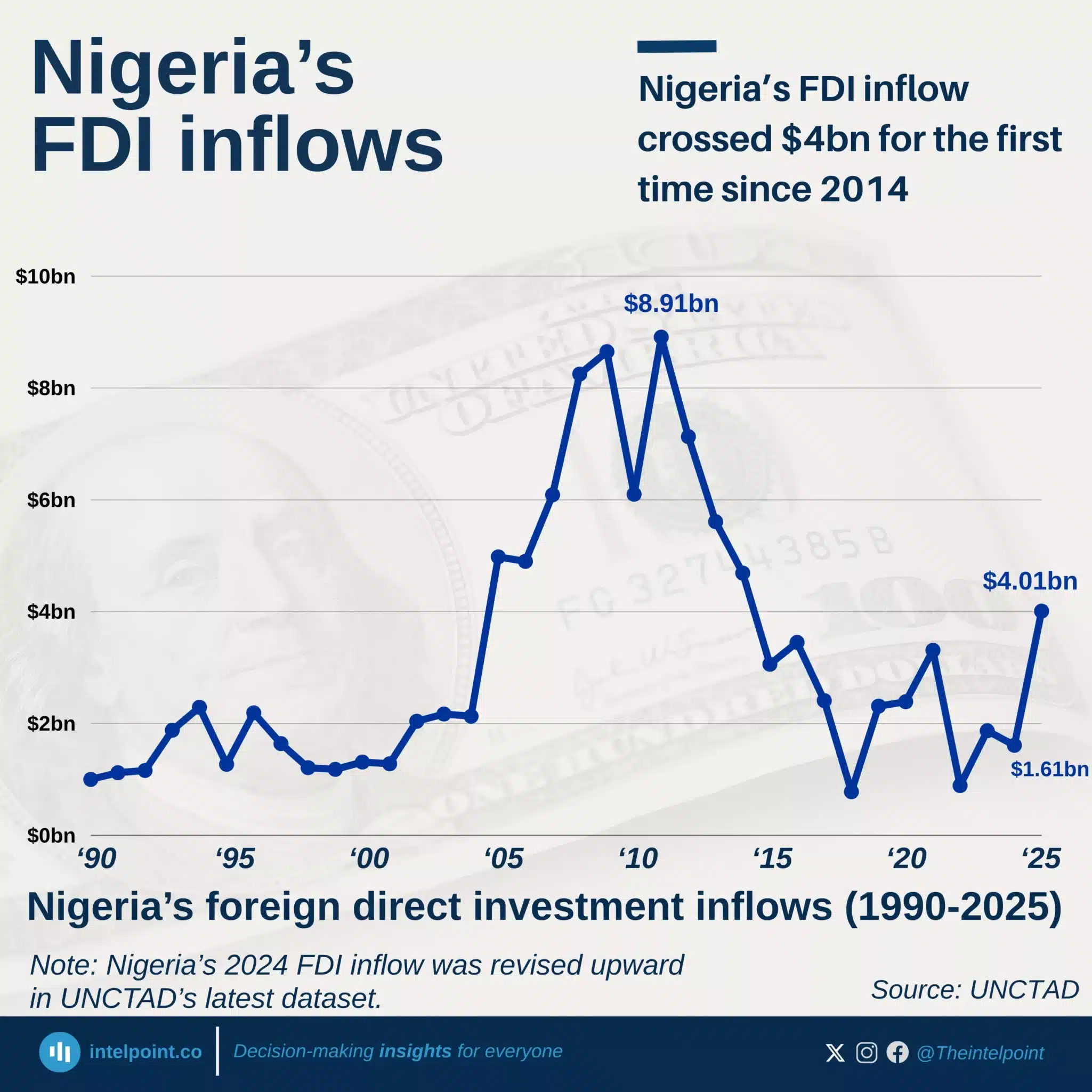

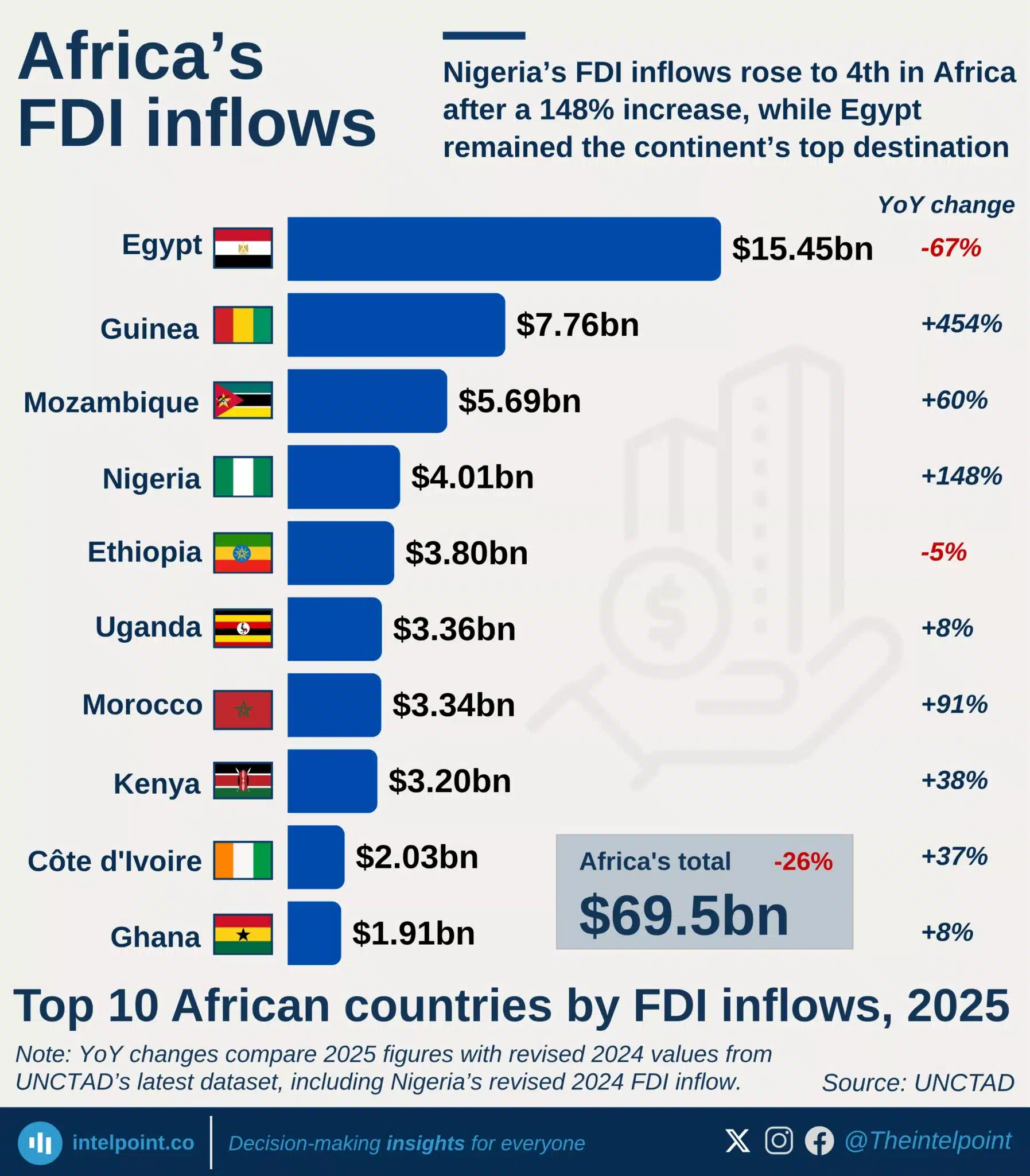

Nigeria’s FDI inflow crossed $4bn for the first time since 2014

Nigeria’s FDI inflows rose to $4.01 billion in 2025, the highest level since 2014.

The 2025 figure represents a 148% increase from the revised $1.61 billion recorded in 2024.

Despite the rebound, Nigeria remains far below its 2011 peak of $8.91 billion.

Nigeria’s strongest FDI period was 2005 to 2014, when inflows stayed above $4 billion every year.

Nigeria’s FDI inflows rose to 4th in Africa after a 148% increase, while Egypt remained the continent’s top destination

Egypt remained Africa’s top FDI destination with $15.45bn. Nigeria ranked 4th after FDI inflows rose 148% to $4.01bn. Guinea had the biggest top-10 jump, rising 454% to $7.76bn. Africa’s top 10 accounted for 73% of total FDI inflows.

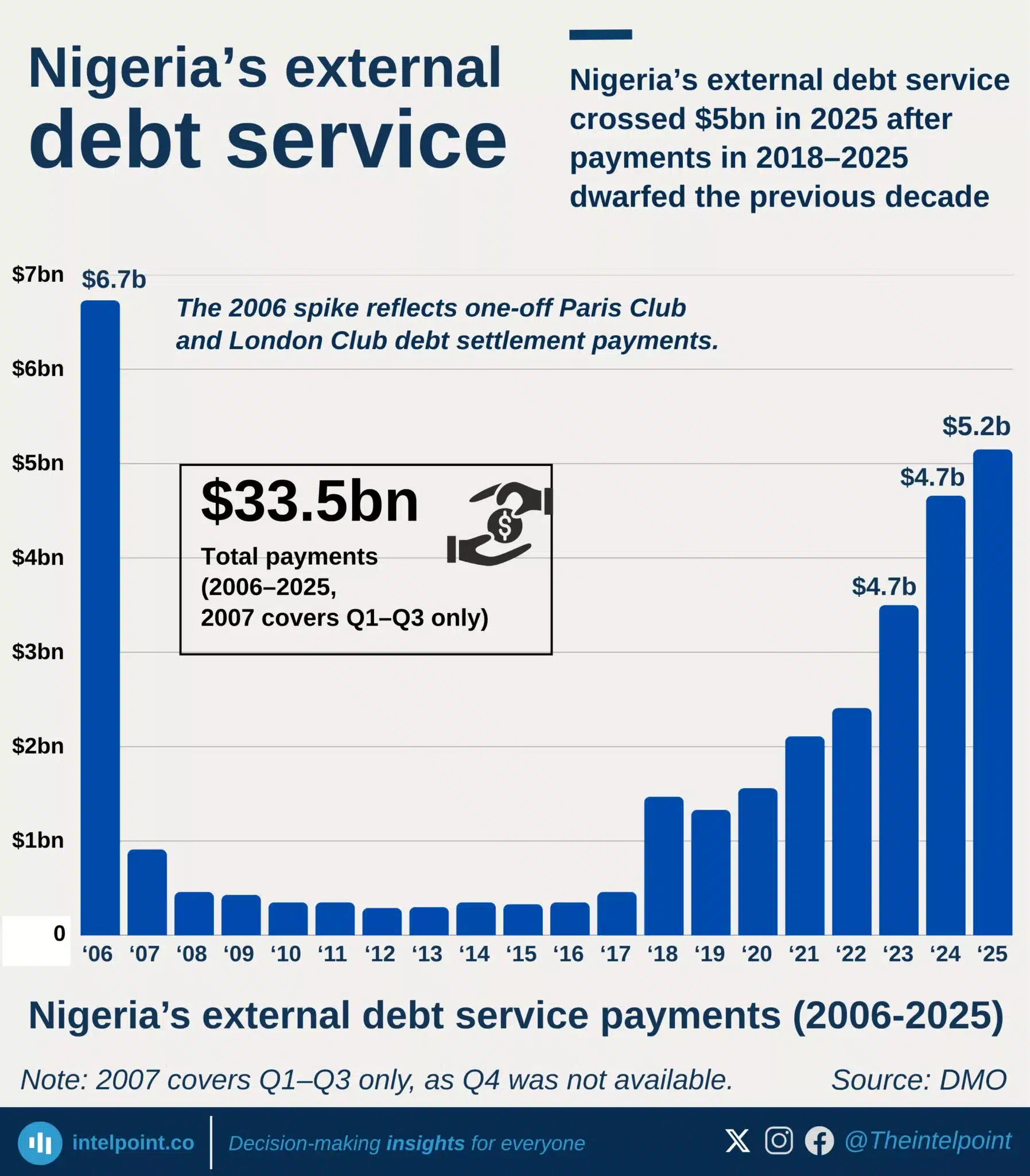

Nigeria’s external debt service crossed $5bn in 2025 after payments in 2018–2025 dwarfed the previous decade

Nigeria’s external debt service entered a heavier phase in 2018.

External debt service crossed $5bn in 2025.

Nigeria paid about $22.2bn from 2018 to 2025.

That was about 6x the $3.7bn paid from 2008 to 2017.

The 2006 spike reflects one-off debt settlement payments.

1

2

3

…

47

Next

Can’t find what you’re looking for? Please fill the form below

Contact Form Demo

Updates

First Name

Last Name

Email

Organisation

Role

Your Message

Submit Form

GET IN TOUCH

+234 813 204 738

hello@intelpoint.co

FIND US ON

SIGN UP TO OUR NEWSLETTER

Get periodic updates about the African startup space, access to our reports, among others.

Subscribe Here

Subscription Form

Updates

Sign Up

A product of Techpoint Africa. All rights reserved

Subscribe to our newsletter

Subscription Form

Subscribe

Sign Up

twitter-square

facebook-square

instagram