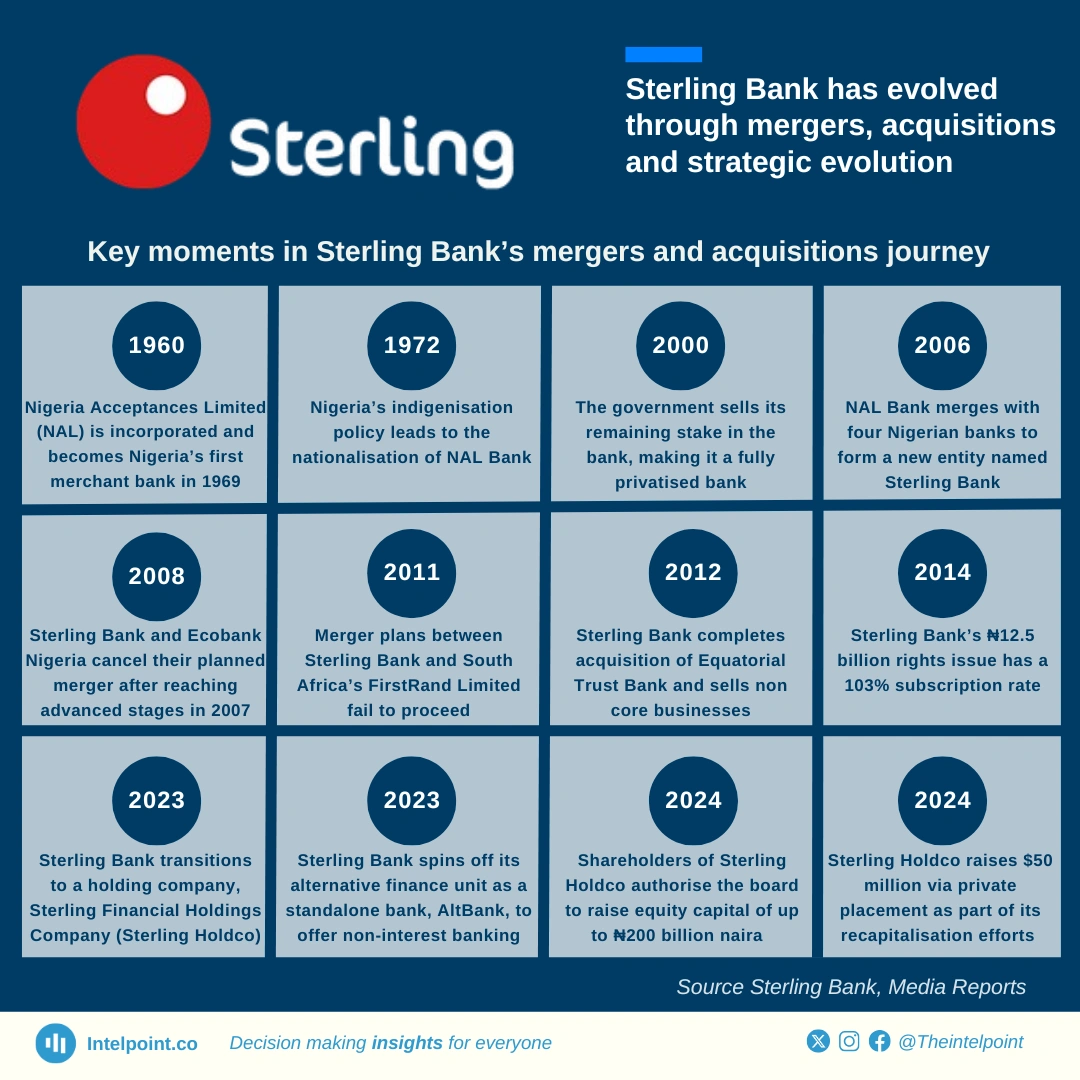

Sterling Bank's origins trace back to 1960 as Nigeria Acceptances Limited, later becoming the first merchant bank in 1969

In 2006, NAL Bank merged with four other banks, forming Sterling Bank as it is known today

Sterling explored several merger opportunities, including with Ecobank in 2008 and FirstRand in 2011, but these plans did not materialise

In 2023, Sterling transitioned into a holding company structure, spinning off its alternative finance arm as a standalone entity, AltBank

The bank began raising fresh capital in 2024, with shareholders approving a ₦200 billion equity capital raise and securing a $50 million private placement as part of its recapitalisation

FirstBank has undergone multiple transformations since its establishment in 1894, adapting to industry shifts and regulatory changes.

The bank transitioned from foreign ownership to local incorporation in 1969, aligning with Nigeria’s indigenisation policy.

Structural and branding changes continued, including its rebranding to First Bank of Nigeria in 1979 and restructuring into a holding company in 2012.

Recent developments include FBN Holdings’ name change to FirstHoldCo and the bank’s planned relocation of its headquarters to Eko Atlantic City in 2025.

Polaris Bank traces its roots back to the establishment of Prudent Bank Plc in 1989.

Prudent Merchant Bank Limited merged with Bond Bank Limited, EIB International Bank Plc, Reliance Bank Limited, and Co-operative Bank Plc to create Skye Bank Plc.

In 2014, Skye Bank Plc acquired Mainstreet Bank Limited.

The Central Bank of Nigeria revoked Skye Bank's operating license in 2018, and Polaris Bank Limited subsequently took over its assets and liabilities.