Africa's rise to the top of the World Bank borrowing table was not a single event; it was the result of one crisis stacking on top of another.

Before the pandemic, African governments were already borrowing heavily to close an infrastructure gap estimated at up to $108 billion per year in roads, power, and connectivity. Then the commodity price crash of 2014 hit, throwing 10 of the 14 countries that had taken out natural resource-backed loans into serious debt trouble and forcing many to return to multilateral lenders just to cover existing obligations.

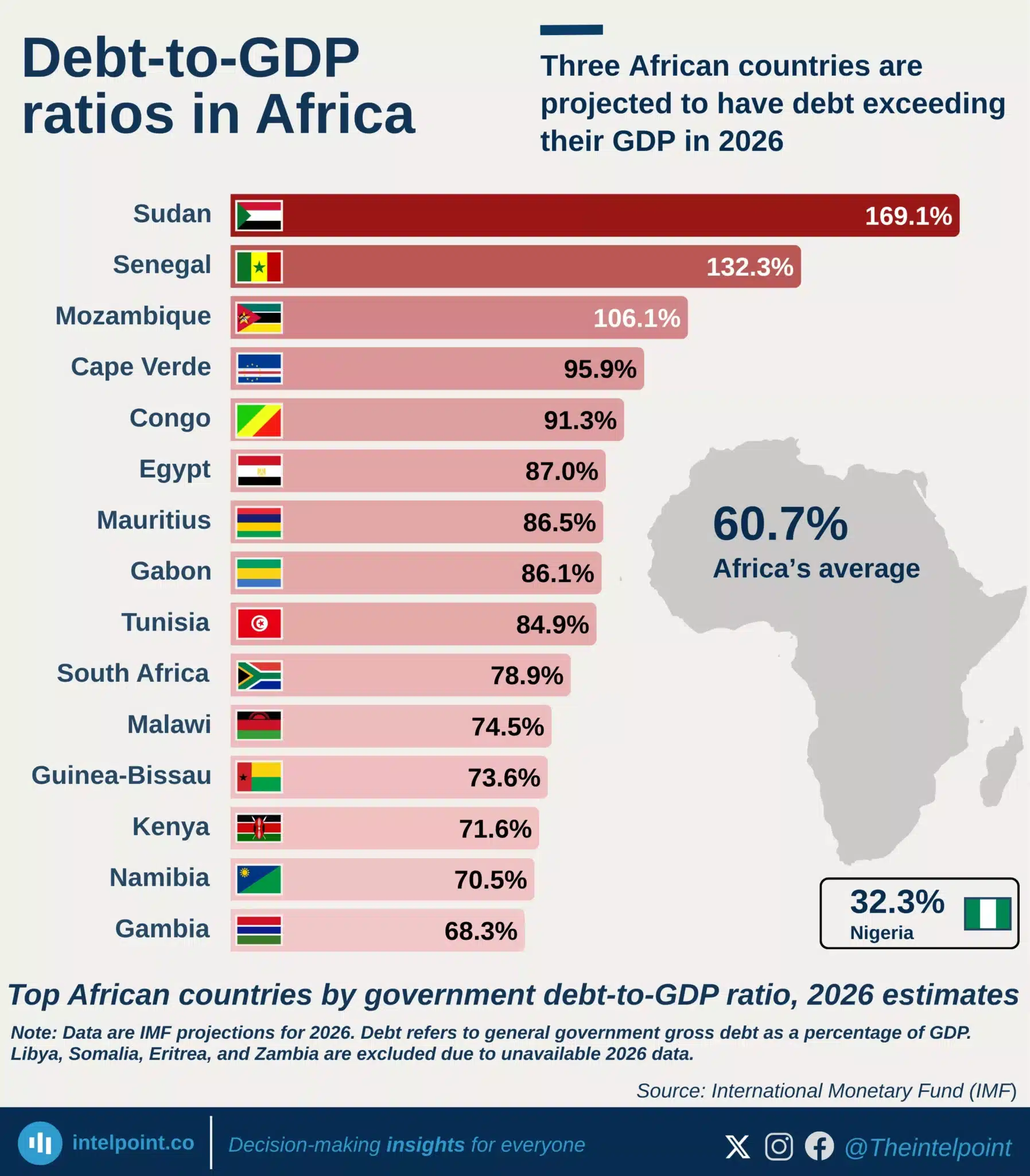

COVID-19 made everything worse. With tax revenues collapsing, health budgets stretched, and currencies sliding against the dollar, 21 low-income African countries are now either in debt distress or dangerously close to it.

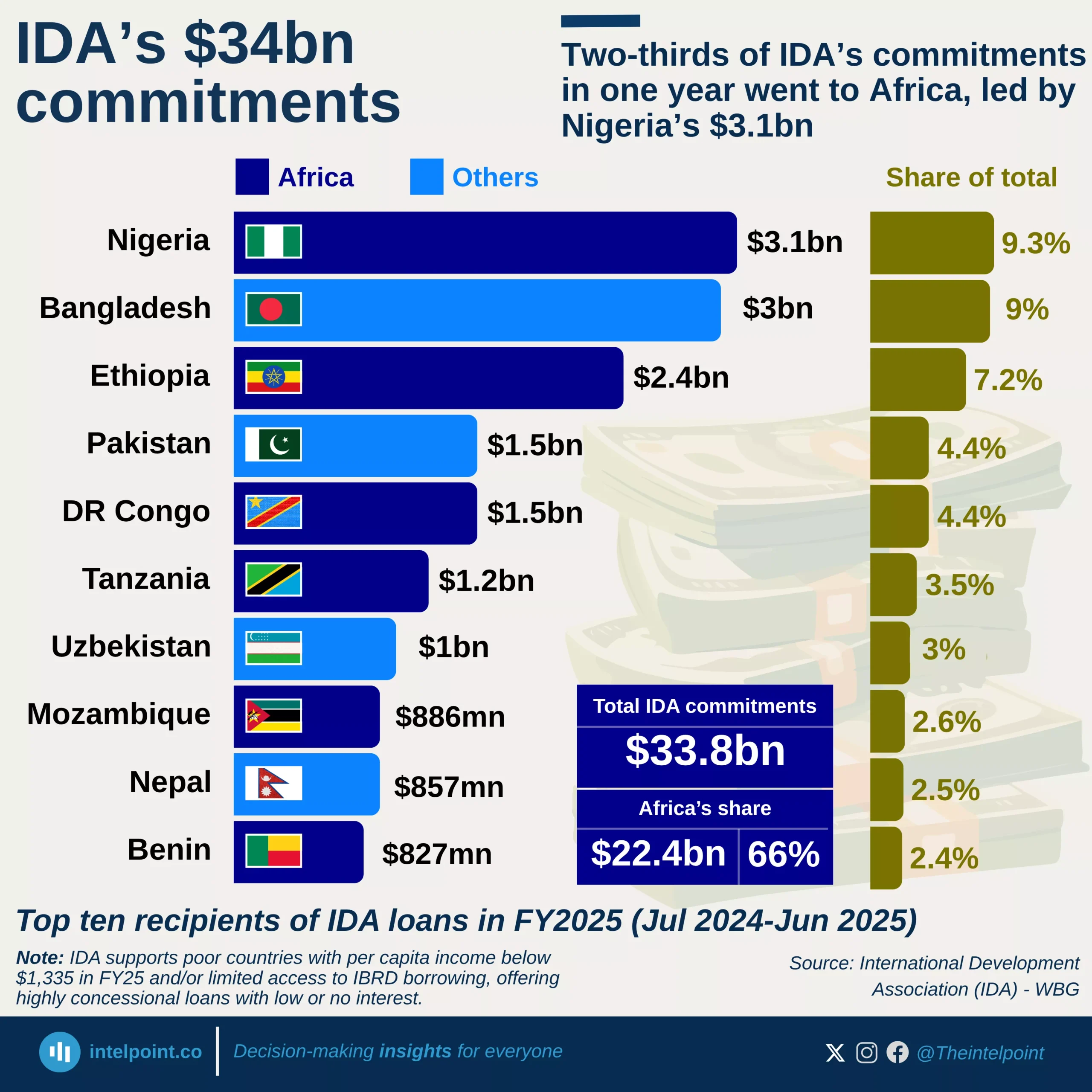

The World Bank stepped in to fill that vacuum in a big way; since its founding, IDA has disbursed just over $210 billion to Africa, accounting for 73% of its total lifetime disbursements.

By 2024, Africa's outstanding World Bank debt stood at $151.7 billion, more than double East Asia and Pacific's $71.3 billion and clear of every other region by a distance that has only grown since 2017.

But the regional number hides more than it reveals.

Just six countries — Nigeria ($17.8 billion), Kenya ($13.8 billion), Ethiopia ($12.8 billion), Egypt ($12.3 billion), Tanzania ($12.1 billion), and Morocco ($10.2 billion) — account for roughly 52% of Africa's entire World Bank debt stock; this concentration has only deepened over time.

Nigeria alone has gone from $2.27 billion in 2000 to $17.8 billion in 2024, a near-eightfold increase in two decades. In the 2025 fiscal year alone, Africa absorbed 66% of all IDA commitments globally — $22.4 billion in a single year — a concentration that reflects both how acute the financing need has become and how deliberately the World Bank has repositioned itself toward the continent.

Europe and Central Asia sit at $60.64 billion, East Asia and Pacific at $71.3 billion, Latin America and the Caribbean at $80.16 billion, South Asia at $89.60 billion, and the Middle East at just $10.82 billion.

This chart tells you who is borrowing. What it does not tell you is whether that borrowing is building something or simply accumulating.