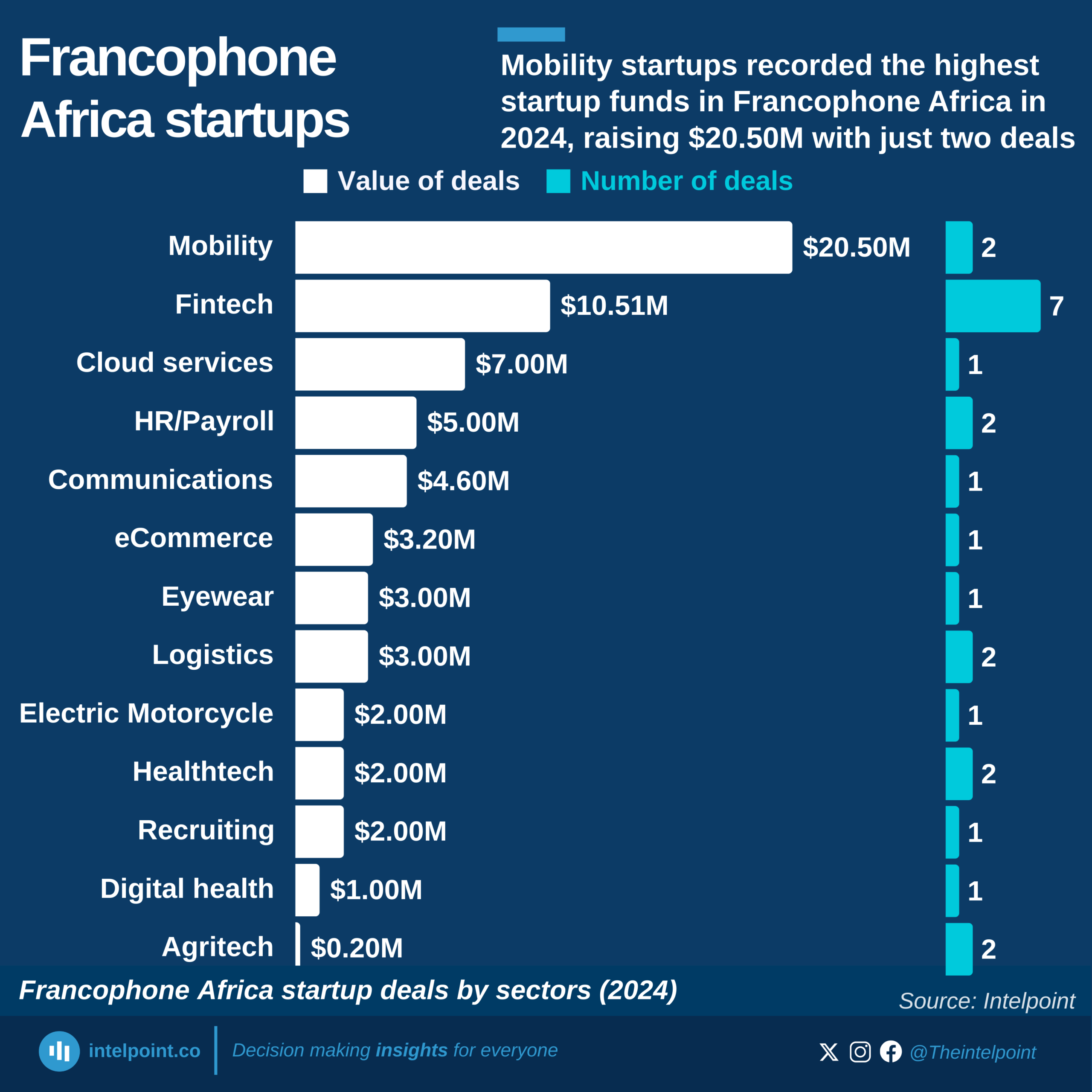

Francophone Africa’s startup ecosystem saw a bold shift in 2024, with Mobility startups taking a surprising lead in total deal value. A single deal in the Mobility sector (secured by Ampersand in Rwanda) accounted for $19.5 million — nearly double the total raised by Fintech (7 deals), which came in second at $10.51 million. The other deal in the mobility sector was at a value of $1M (secured by Solarbox in Senegal). This standout figure perhaps signals the mobility sector’s potential to reshape urban mobility across the region. While Fintech still drew the highest number of deals (7), Mobility claimed the crown for value with just two transactions.

What’s even more interesting is how this reveals the uneven landscape of startup funding in Francophone Africa. Sectors like Cloud Services, HR/Payroll, and Communications each recorded only a single or a couple of deals but raised millions, indicating that investors are willing to place big bets on what they consider high-impact solutions. On the flip side, essential sectors such as Agritech and Digital Health pulled in the lowest funding, highlighting potential blind spots or areas still waiting to catch investor attention.