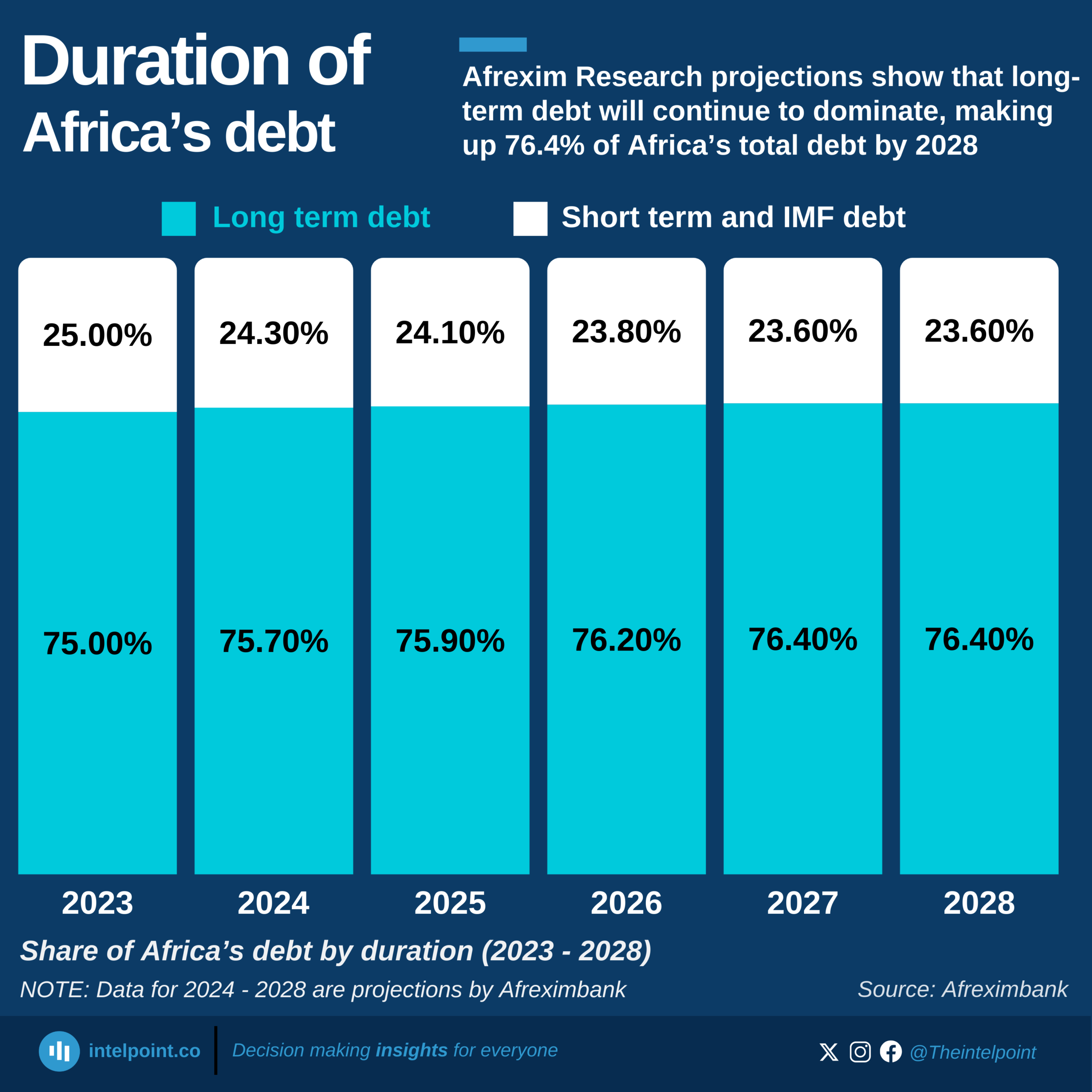

Africa's debt is shifting further toward long-term obligations, with projections indicating that by 2028, 76.4% of the continent’s total debt will be long-term. This slow but steady increase underscores a preference for extended repayment periods, reducing the burden of short-term debt repayments but potentially increasing overall costs due to prolonged interest payments.

In everyday terms, this is similar to how businesses or individuals prefer long-term loans over short-term ones to ease immediate financial pressure. While long-term financing offers breathing space, it requires strong fiscal discipline to ensure that repayments remain sustainable in the future.