Key Takeaways:

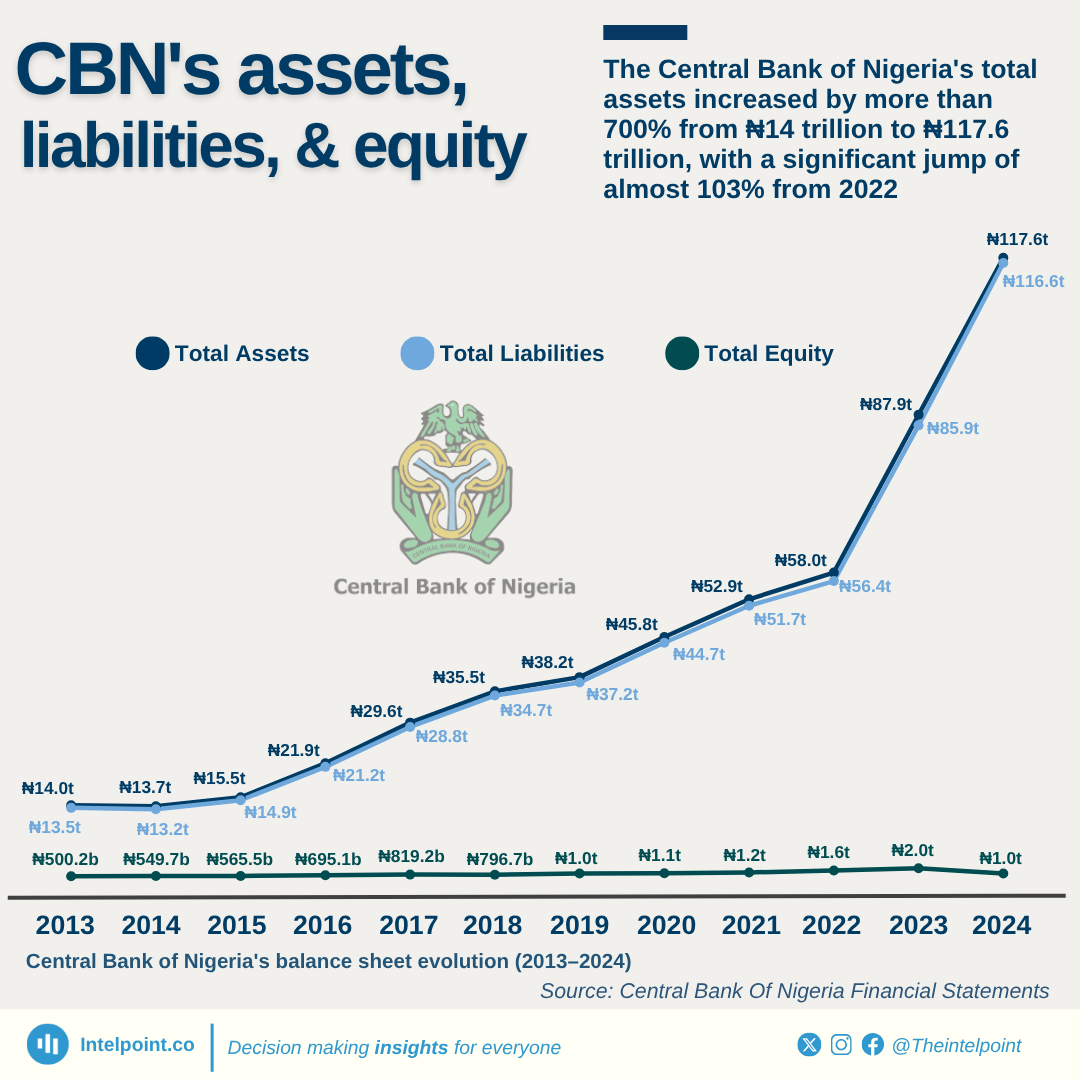

The Central Bank of Nigeria's (CBN) balance sheet grew significantly during the previous decade. Total assets continuously expanded from ₦14 trillion in 2013 to an amazing ₦117.6 trillion by 2024. Similarly, liabilities increased from ₦13.5 trillion to ₦116.6 trillion during the same period.

The total equity of CBN during this period experienced significant fluctuation, ranging from ₦500 billion to ₦2 trillion. Aside from this, the data showed robust financial growth and balance sheet expansion, particularly in the past two years, highlighting the CBN's changing role in Nigeria's economic stability.