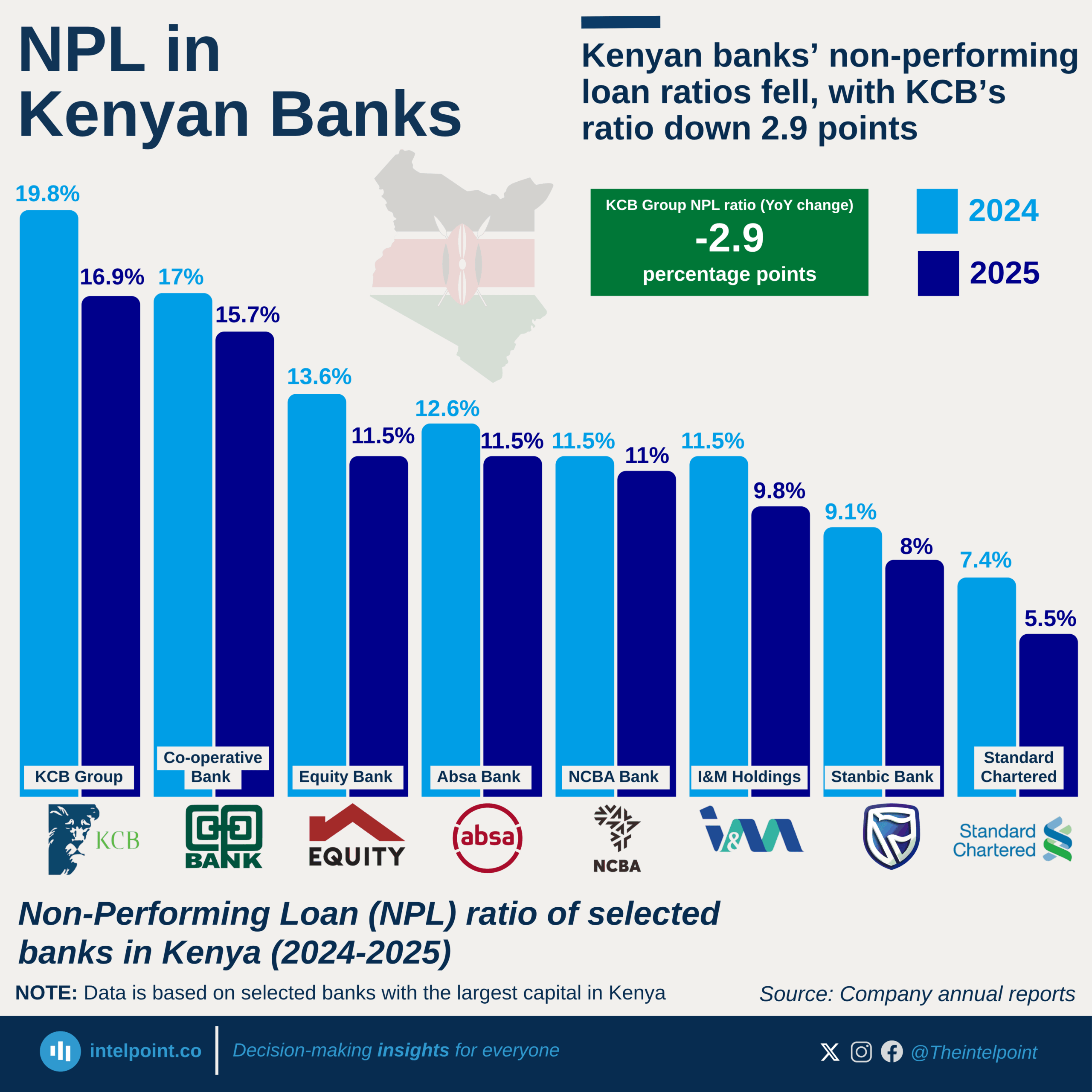

In 2025, asset-quality pressure in Kenyan banking improved for most of the large banks. All eight selected banks show a decline in the non-performing loan ratio, with the largest decline in KCB Group. At the top end, KCB Group still had the highest NPL ratio among the banks at 16.9%, followed closely by Co-operative Bank at 15.7%.

The sector backdrop supports that reading, with the Central Bank of Kenya saying the industry gross NPL ratio rose to 17.6% in April 2025, from 17.2% in February, before easing to 16.5% in November 2025, with reductions seen in sectors such as mining and quarrying, energy and water, personal and household, and transport and communication.

At the bank level, the pattern is mixed but directionally better than the 2024 high mark for several lenders. KCB Group’s FY2025 investor presentation shows its NPL ratio improved to 16.9% from 19.8% in FY2024. Equity Group also improved, with its FY2025 NPL ratio at 11.5%, down from 13.6% in FY2024, after having risen from 12.1% in FY2023. These are not trivial improvements; they point to more aggressive recoveries, restructurings, write-offs, and tighter underwriting.