There are nearly 600 million women aged 15-24 worldwide, with 90% living in low- and middle-income countries (LMICs), making them a significant share of the global population.

37 countries grant women less than half of the legal rights of men, affecting 500 million women, while globally, women enjoy less than two-thirds of the legal rights available to men.

Closing the gender gap in employment and entrepreneurship could boost global GDP by over 20%, and eliminating the gap within a decade could double the global growth rate.

Women hold just 1 in 5 corporate board positions, partly because less than 20% of countries require gender-sensitive public procurement, excluding them from a $10 trillion-a-year opportunity.

Women earn only 77 cents for every $1 paid to men, while 92 countries lack equal pay laws. Additionally, 20 countries prohibit women from night work and 45 ban women from “dangerous” jobs.

By 2030, an estimated 8% of the world’s female population (342.4 million women and girls) will still live on less than $2.15 a day, with 220.9 million in sub-Saharan Africa.

Climate change could push 158.3 million more women and girls into poverty by 2050, which is 16 million more than men and boys under a worst-case scenario.

By 2020, food insecurity was projected to impact 236 million more women and girls, compared to 131 million more men and boys.

By 2050, women will still spend 2.5 times more hours per day on unpaid care work than men. If valued monetarily, women’s unpaid labor could exceed 40% of GDP in some countries.

The International Women's Day (IWD) 2025 theme, "Accelerate Action," calls on everyone—individuals, businesses, and governments—to break barriers and speed up progress toward gender equality.

The United Nations Secretary-General, in his IWD address, emphasizes the importance of heeding the voices of women and girls globally, advocating for action over apathy to advance gender equality.

Source:

World Bank Group, United Nations, Consultative Group to Assist the Poor (CGAP)

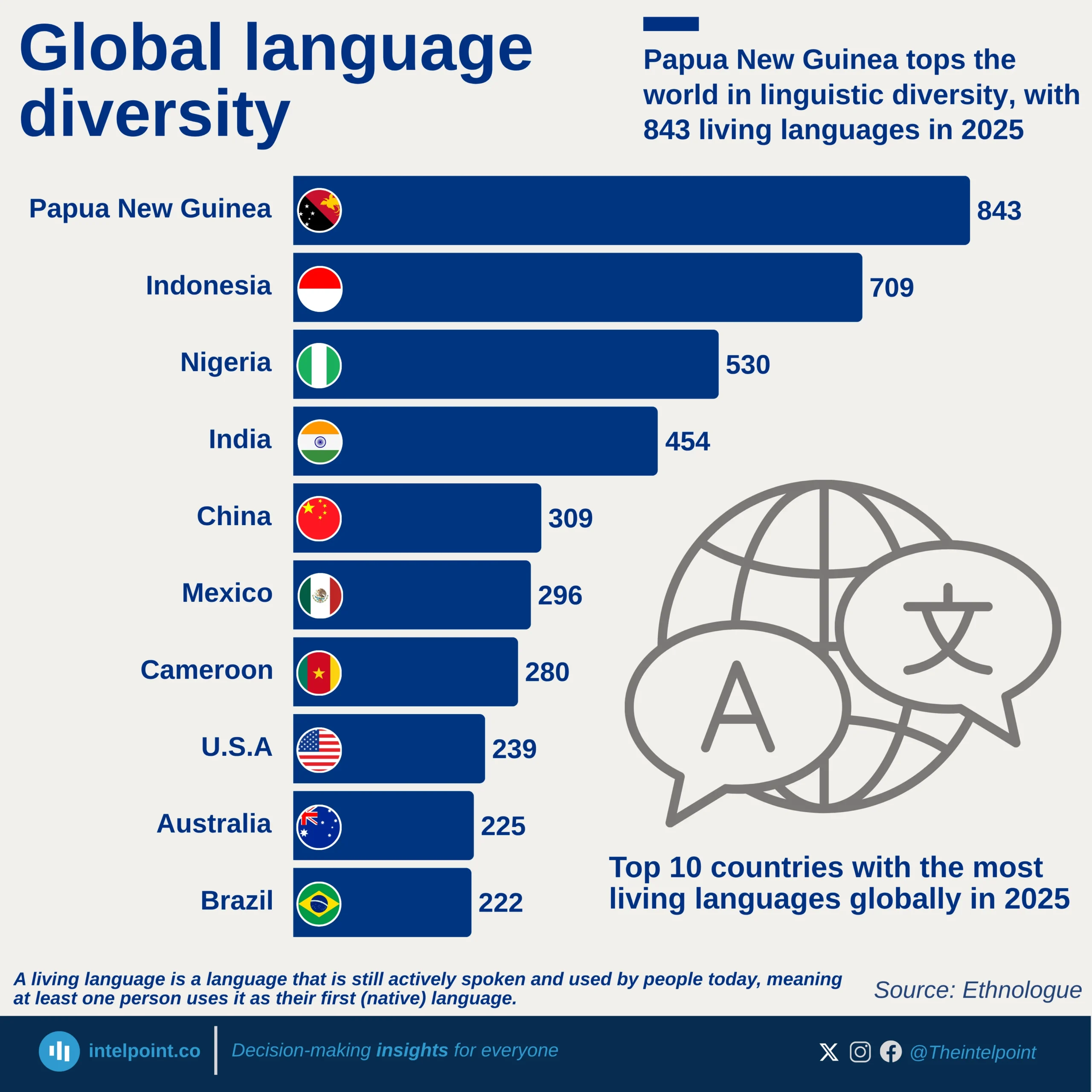

Papua New Guinea remains unmatched: With 843 living languages, the Pacific nation continues to hold the title of the world’s most linguistically diverse country.

Nigeria tops Africa: Hosting 530 living languages, Nigeria ranks third globally and stands as Africa’s richest linguistic hub.

Indonesia (709) and India (454) are also in the top five, showcasing the dense cultural mosaic across Asia.

Even large, developed countries like the U.S. (239), Australia (225), and Brazil (222) make the list, proving that language diversity transcends geography and development.

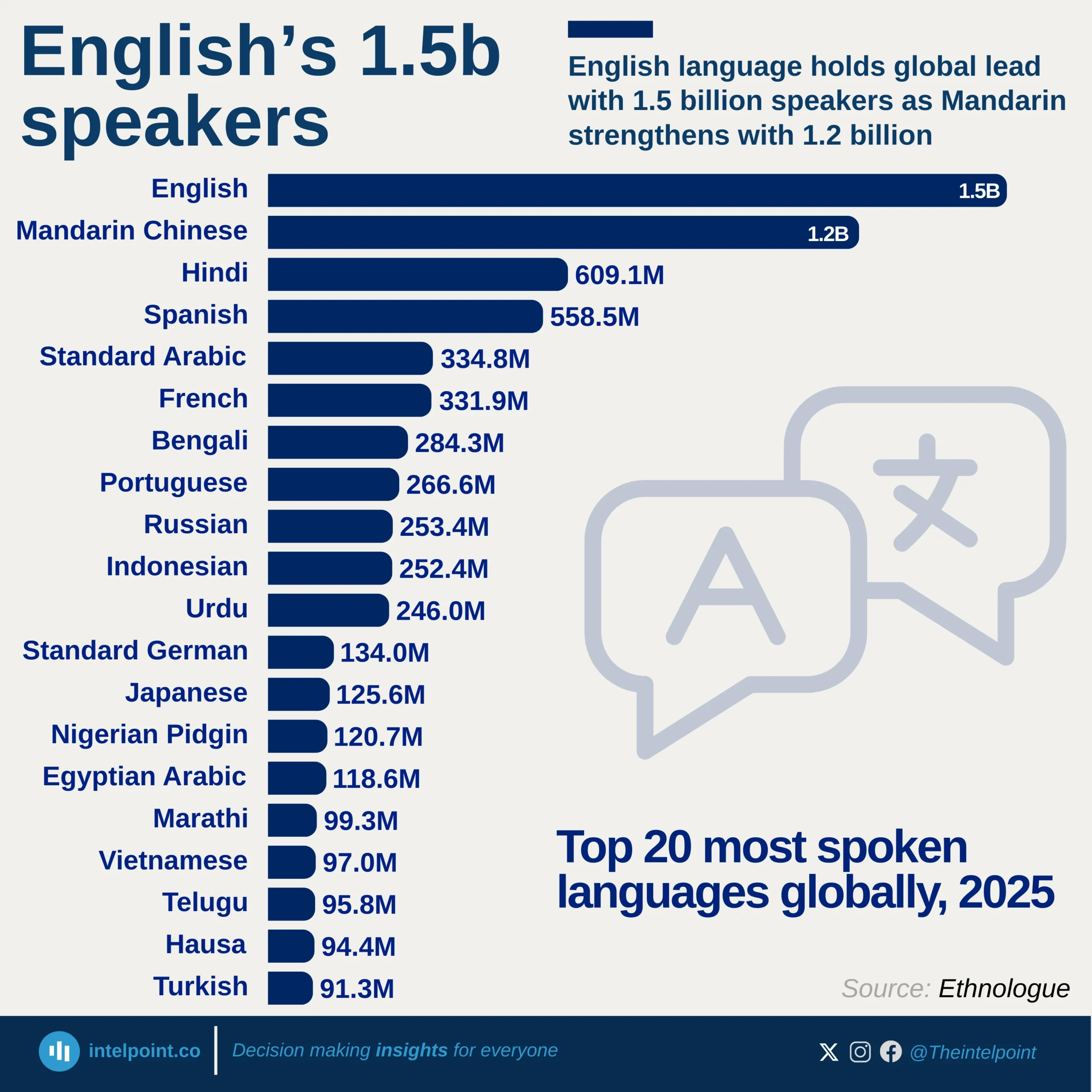

English dominates globally with 1.5 billion speakers, nearly 300 million more than Mandarin Chinese.

Asian languages are highly represented, with Mandarin, Hindi, Arabic, Bengali, Indonesian, Urdu, Japanese, Marathi, Vietnamese, Telugu, and Turkish making up over half of the top 20.

Spanish and French stand out as major global languages, reflecting both native speakers and strong international adoption. African languages are emerging on the global stage, with Nigerian Pidgin (120.7M) and Hausa (94.4M) among the top 20.

The gap between top and bottom languages in the ranking is wide. English has over 15 times more speakers than Turkish, which closes the top 20 list.

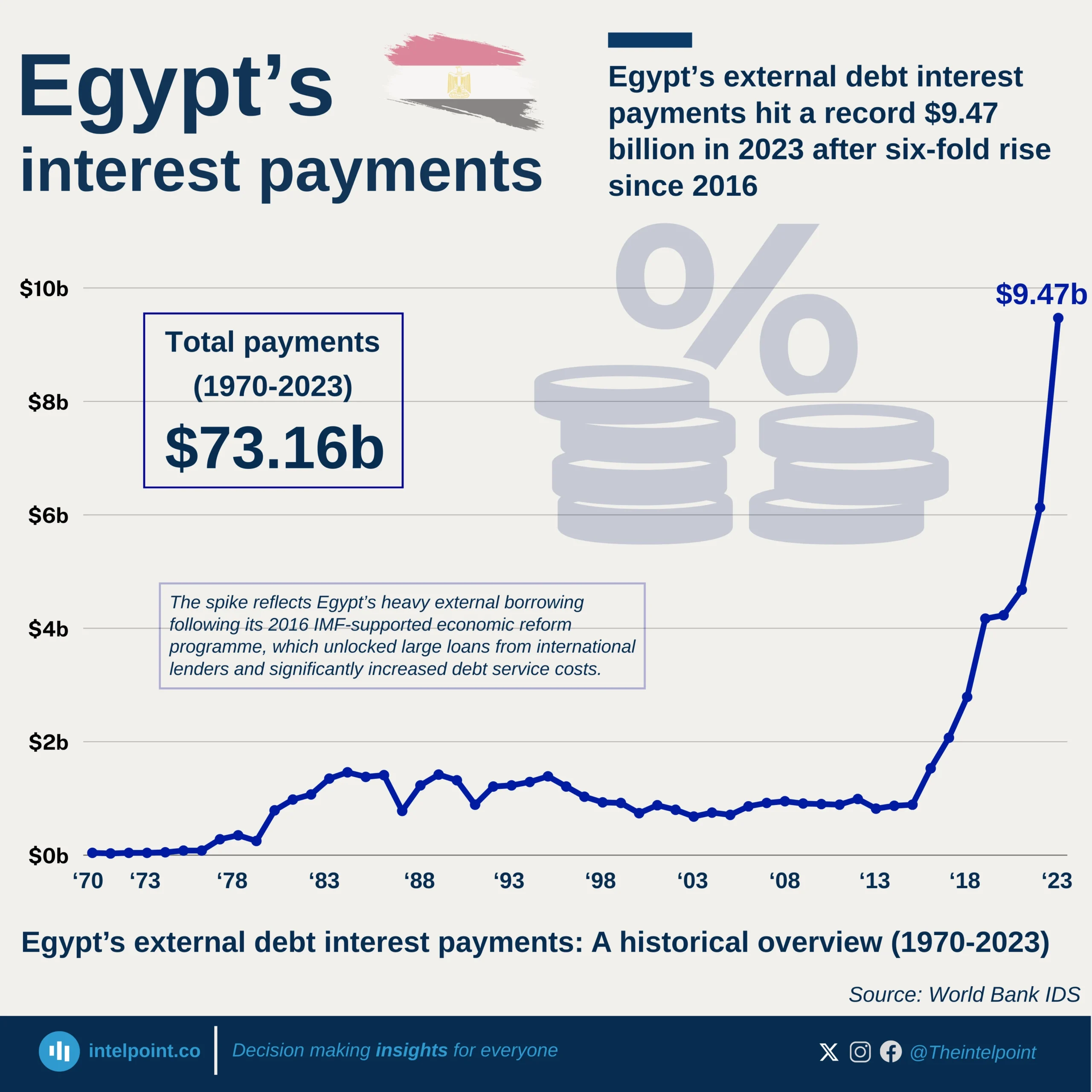

From 1970 through the early 2000s, Egypt’s debt interest payments hovered mostly under $1.5 billion, with fluctuations tied to global oil shocks and debt rescheduling.

Payments remained relatively moderate, ranging between $0.7–$1.0 billion annually.

Following Egypt’s 2016 IMF programme and rising external borrowing, payments jumped dramatically, climbing from $1.53 billion in 2016 to $6.13 billion in 2022.

Interest payments hit an all-time high of $9.47 billion in 2023, underscoring the heavy burden of Egypt’s rapid debt accumulation and exposure to global financing costs.