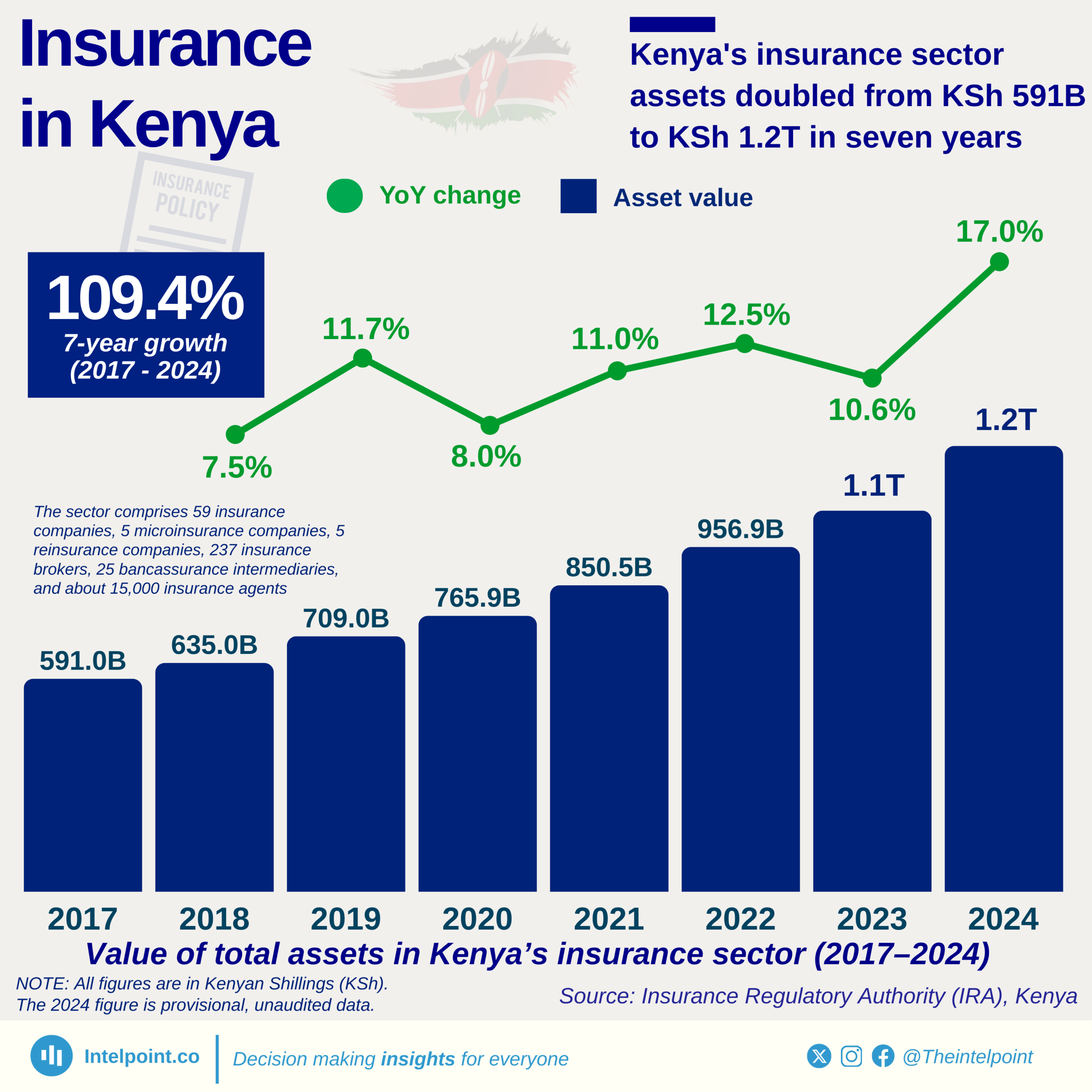

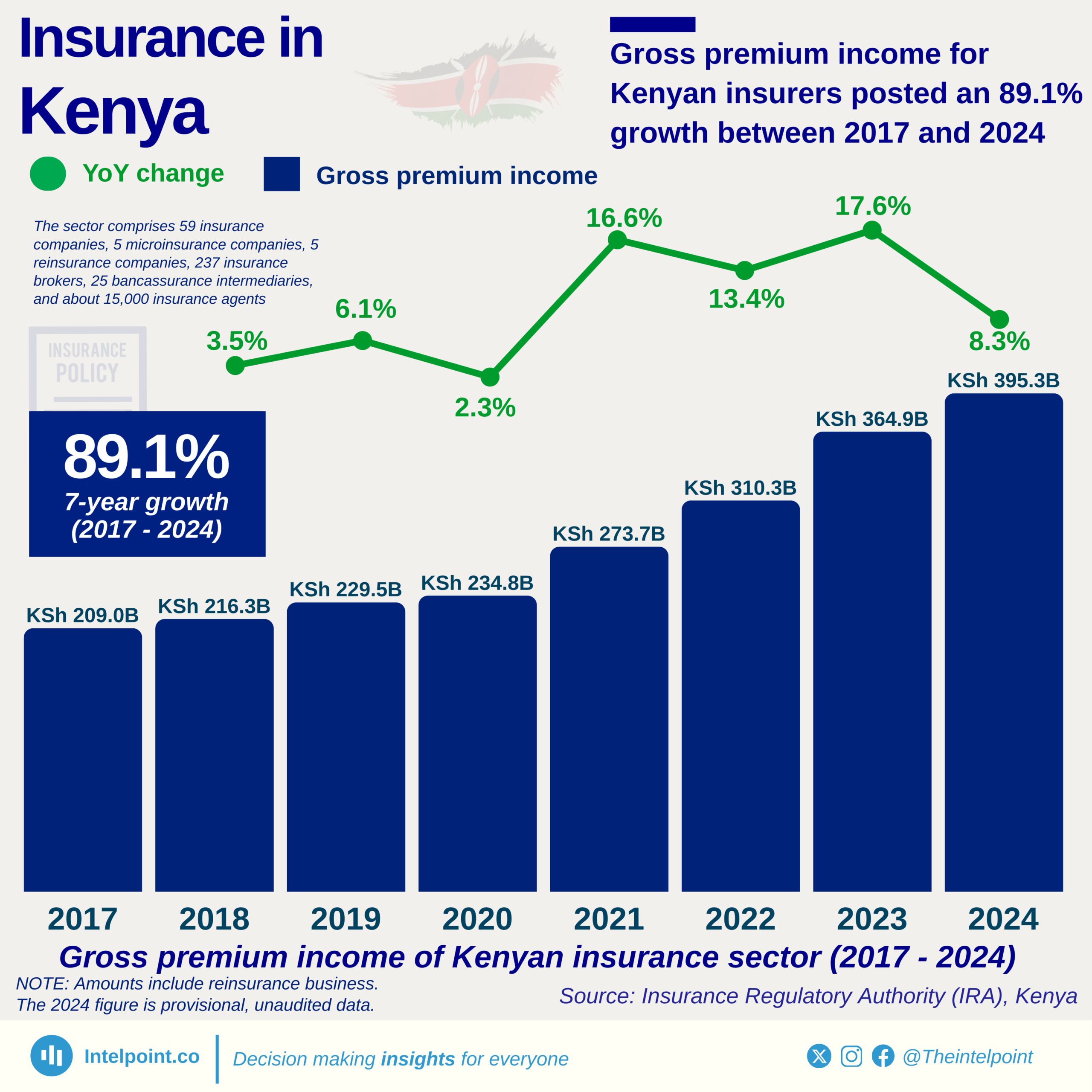

The gross premium income of Kenya’s insurance sector rose from KSh 209.0 billion in 2017 to KSh 395.3 billion in 2024. This represents an impressive 89.1% increase, underscoring the sector’s expanding role in financial services and risk management. While year-on-year growth has varied, the overall trend reveals a steadily deepening insurance market in the country. This shift points to growing awareness, rising incomes, and increased trust in insurance services—factors that are gradually transforming the sector into a key pillar of Kenya’s economy.