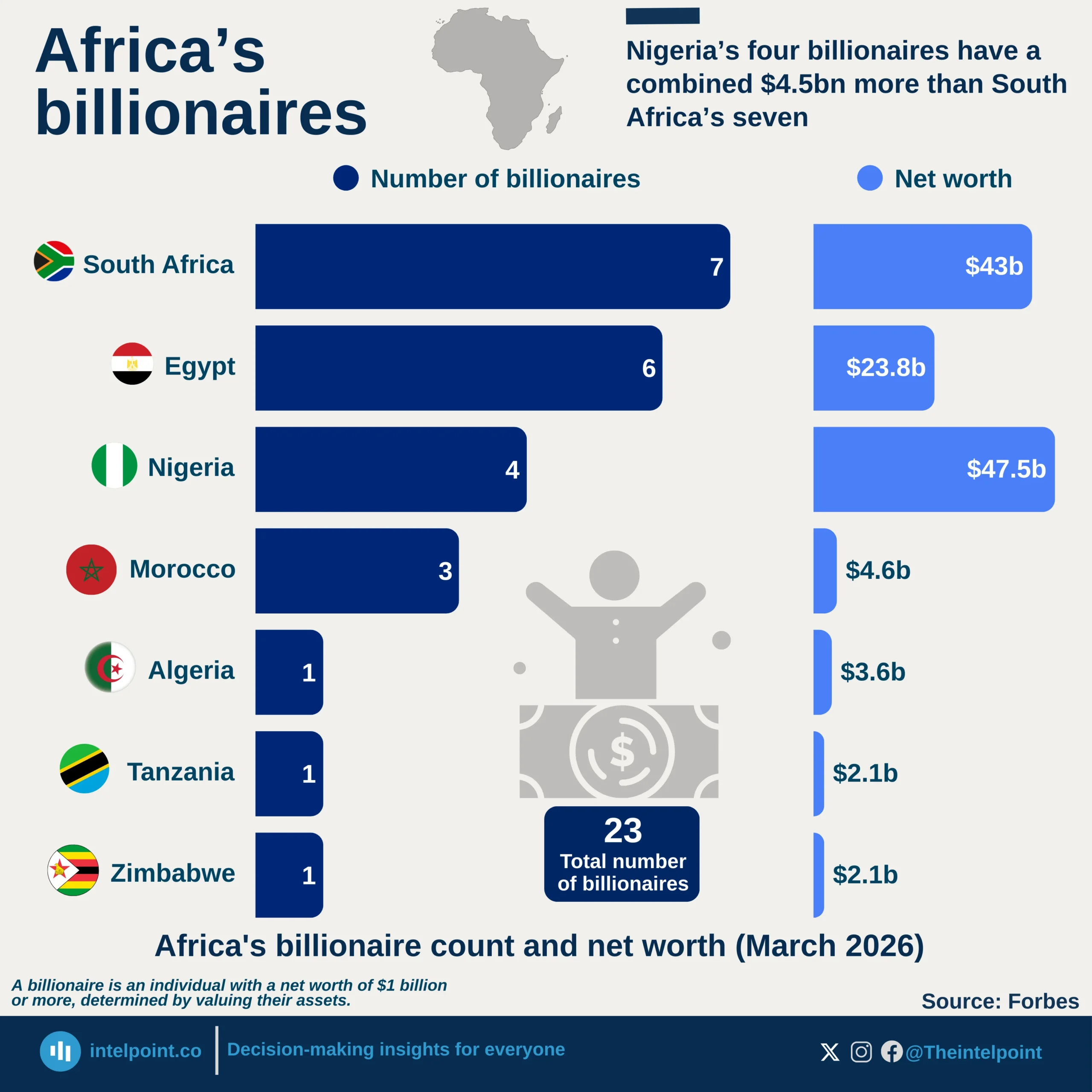

South Africa leads in headcount, with seven billionaires, more than other African countries.

Nigeria leads in wealth, with four billionaires worth $47.5 billion, $4.5 billion more than the combined $43 billion of South Africa's seven billionaires.

Nigeria's billionaires are richer individually, with an average net worth of $11.9 billion, compared with South Africa's $6.1 billion.

North Africa punches below its weight: Egypt, Morocco, and Algeria have ten billionaires combined but just $31.4 billion in total wealth.

East Africa barely registers: Tanzania and Zimbabwe each have just one billionaire, both worth $2.1 billion.

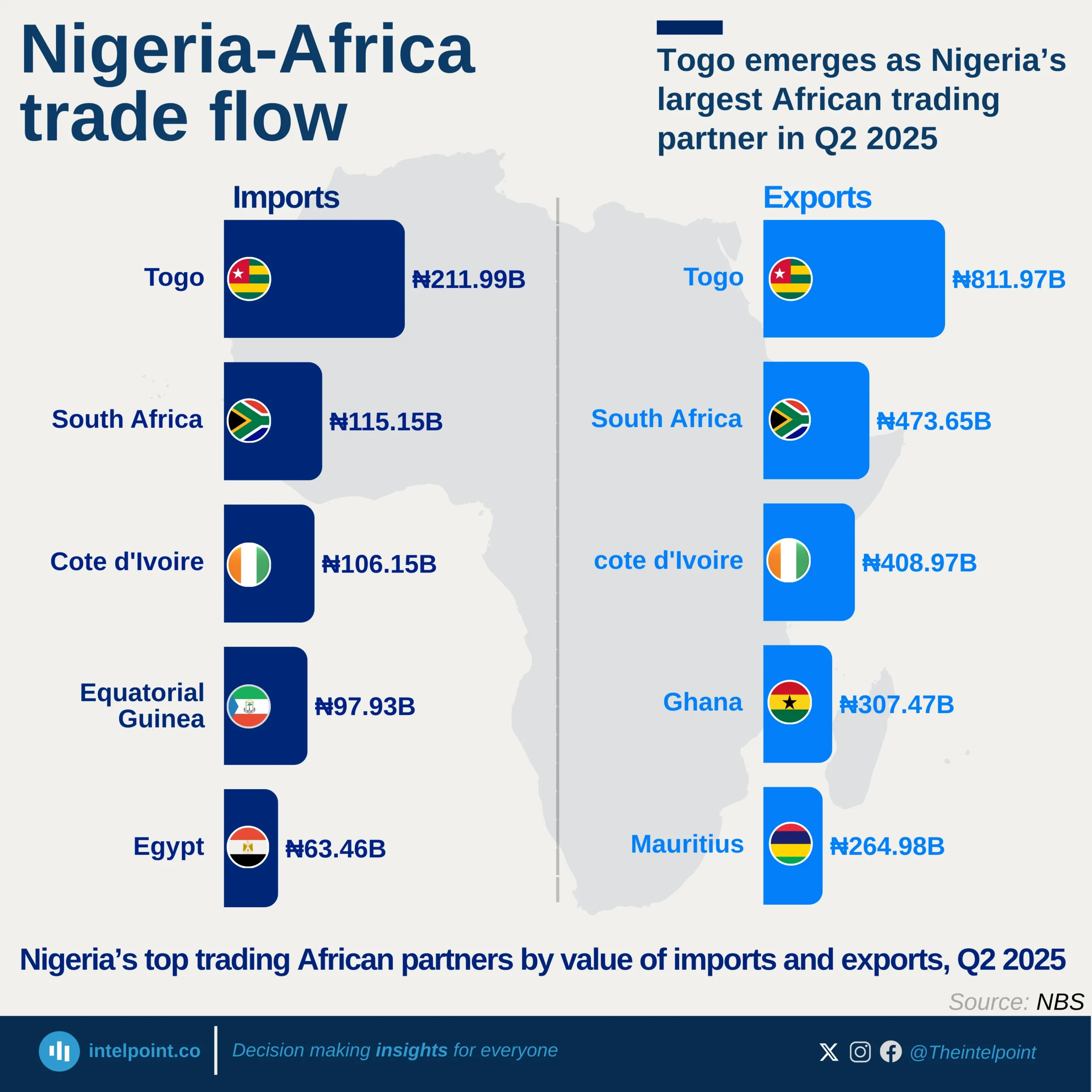

Togo leads on both sides of trade, supplying ₦211.99B in imports and receiving ₦811.97B in exports, making it Nigeria’s strongest African partner by value.

South Africa ranks second, with imports of ₦115.15B and exports of ₦473.65B, reflecting deep bilateral trade ties.

Côte d’Ivoire also features prominently, sending ₦106.15B worth of goods to Nigeria while importing ₦408.97B, showing balanced engagement.

West Africa dominates Nigeria’s intra-African trade, with Togo, Côte d’Ivoire, and Ghana collectively accounting for a significant share of regional exports.

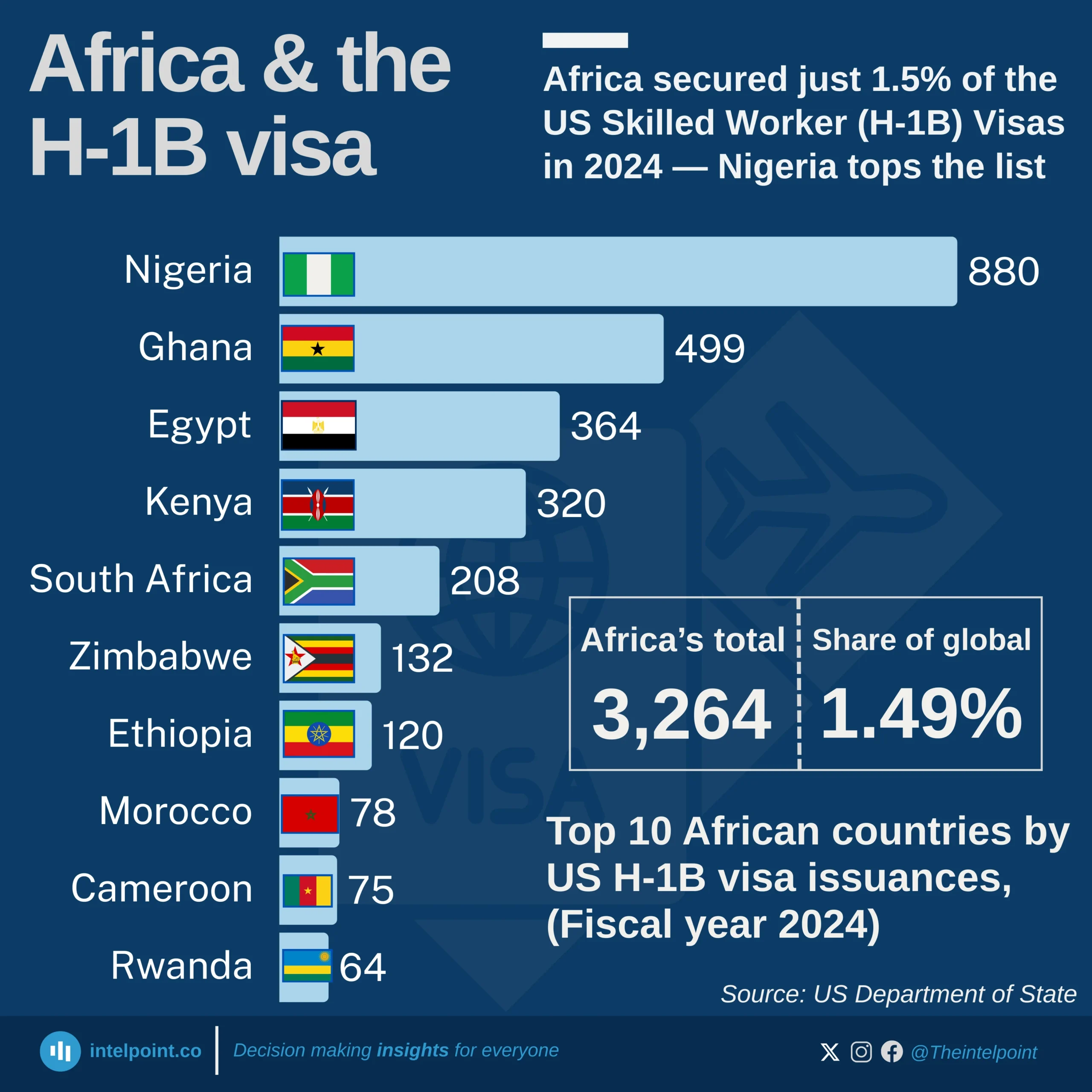

Nigeria ranked first in Africa, with 880 H-1B visas issued in FY 2024, far ahead of Ghana (499) and Egypt (364).

East and Southern Africa featured prominently, with Kenya (320), South Africa (208), and Zimbabwe (132) among the top 10.

North African representation was modest, with Morocco (78) and Egypt (364) being the only countries in the region on the list.

Despite these numbers, Africa’s collective total is marginal globally, especially compared to India’s ~150,000 issuances and China’s large volumes.

President Donald Trump’s $100,000 fee for new U.S. H-1B skilled worker visas will have limited impact on Africa, which has historically received only a small fraction of these visas.

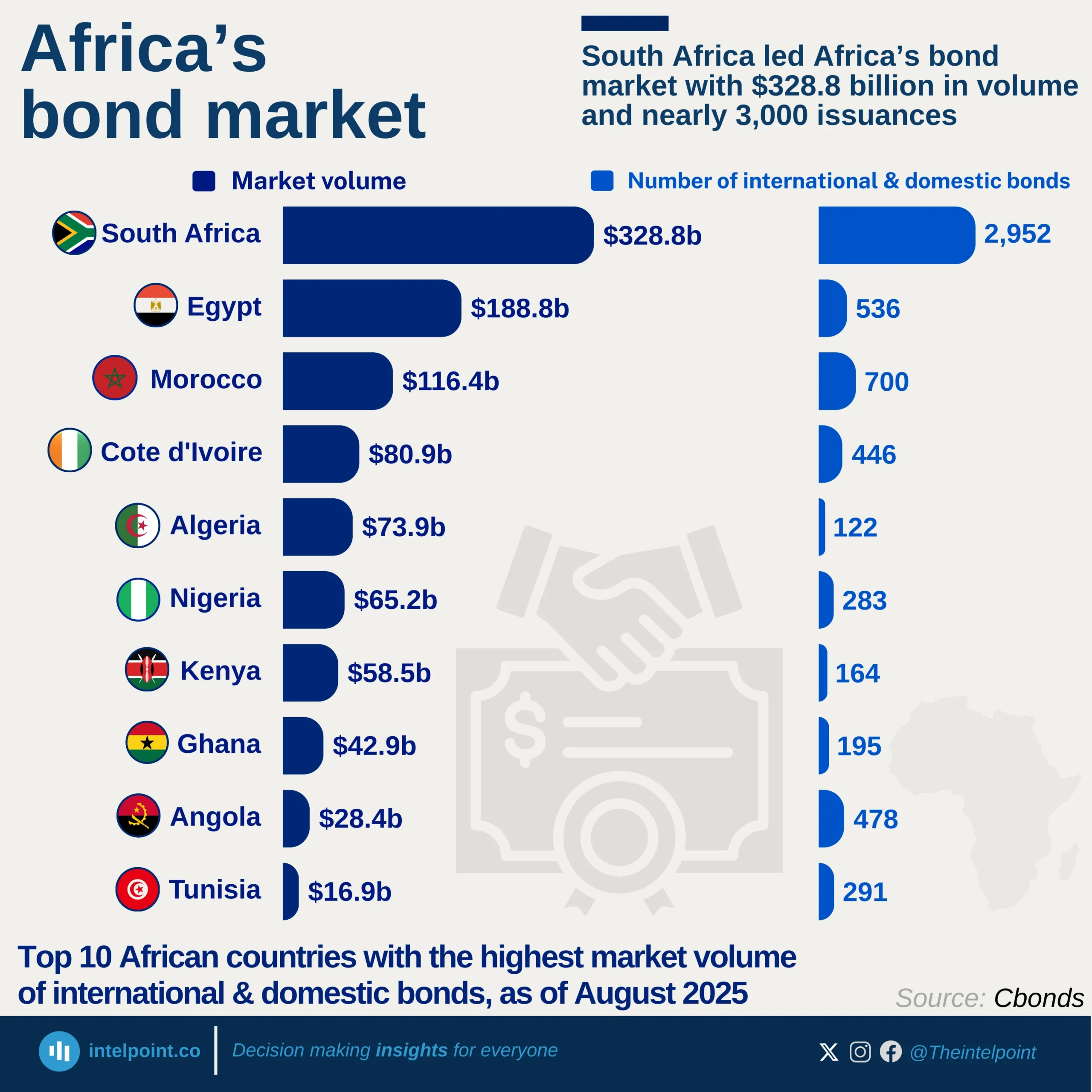

South Africa is the clear leader, recording a bond market volume of $328.8 billion and 2,952 issuances, far ahead of all other African economies.

Egypt and Morocco follow as strong contenders with bond volumes of $188.8 billion and $116.4 billion, respectively, though both trail South Africa by wide margins.

Côte d’Ivoire, Algeria, and Nigeria represent the mid-tier, each exceeding $65 billion, showing notable regional financial activity.

Smaller markets like Tunisia and Angola feature relatively lower volumes ($16.9 billion and $28.4 billion) but maintain significant issuance activity.