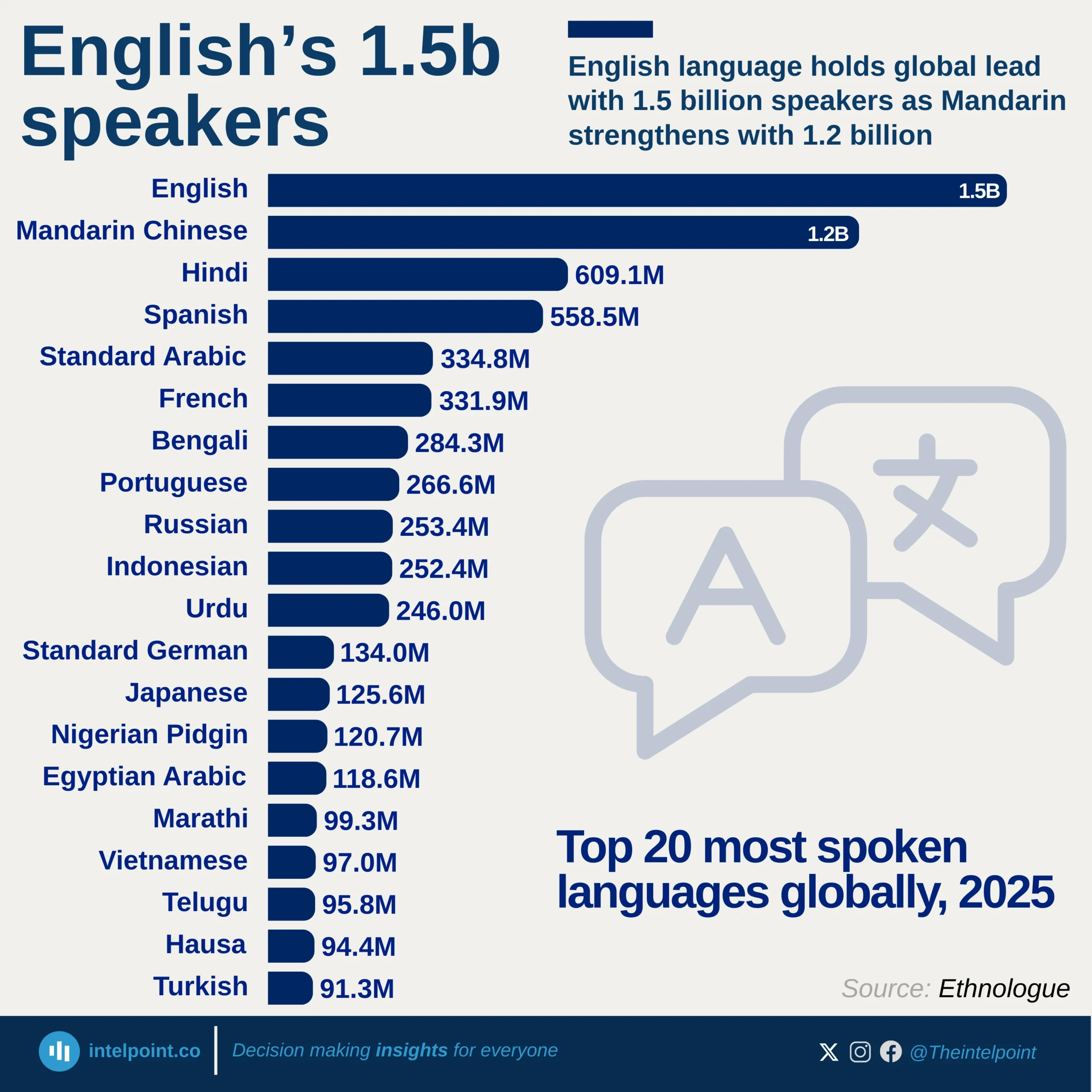

English dominates globally with 1.5 billion speakers, nearly 300 million more than Mandarin Chinese.

Asian languages are highly represented, with Mandarin, Hindi, Arabic, Bengali, Indonesian, Urdu, Japanese, Marathi, Vietnamese, Telugu, and Turkish making up over half of the top 20.

Spanish and French stand out as major global languages, reflecting both native speakers and strong international adoption. African languages are emerging on the global stage, with Nigerian Pidgin (120.7M) and Hausa (94.4M) among the top 20.

The gap between top and bottom languages in the ranking is wide. English has over 15 times more speakers than Turkish, which closes the top 20 list.

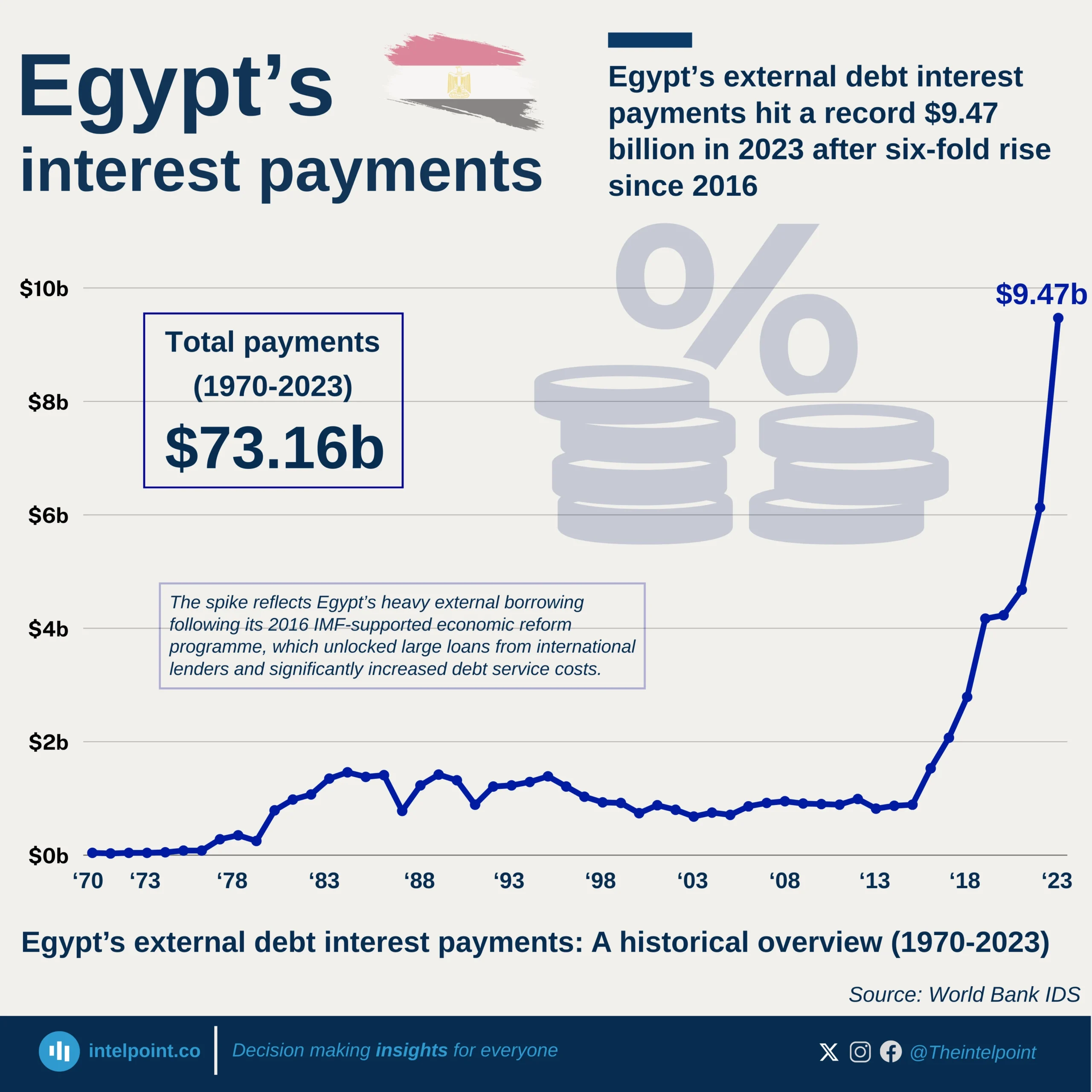

From 1970 through the early 2000s, Egypt’s debt interest payments hovered mostly under $1.5 billion, with fluctuations tied to global oil shocks and debt rescheduling.

Payments remained relatively moderate, ranging between $0.7–$1.0 billion annually.

Following Egypt’s 2016 IMF programme and rising external borrowing, payments jumped dramatically, climbing from $1.53 billion in 2016 to $6.13 billion in 2022.

Interest payments hit an all-time high of $9.47 billion in 2023, underscoring the heavy burden of Egypt’s rapid debt accumulation and exposure to global financing costs.

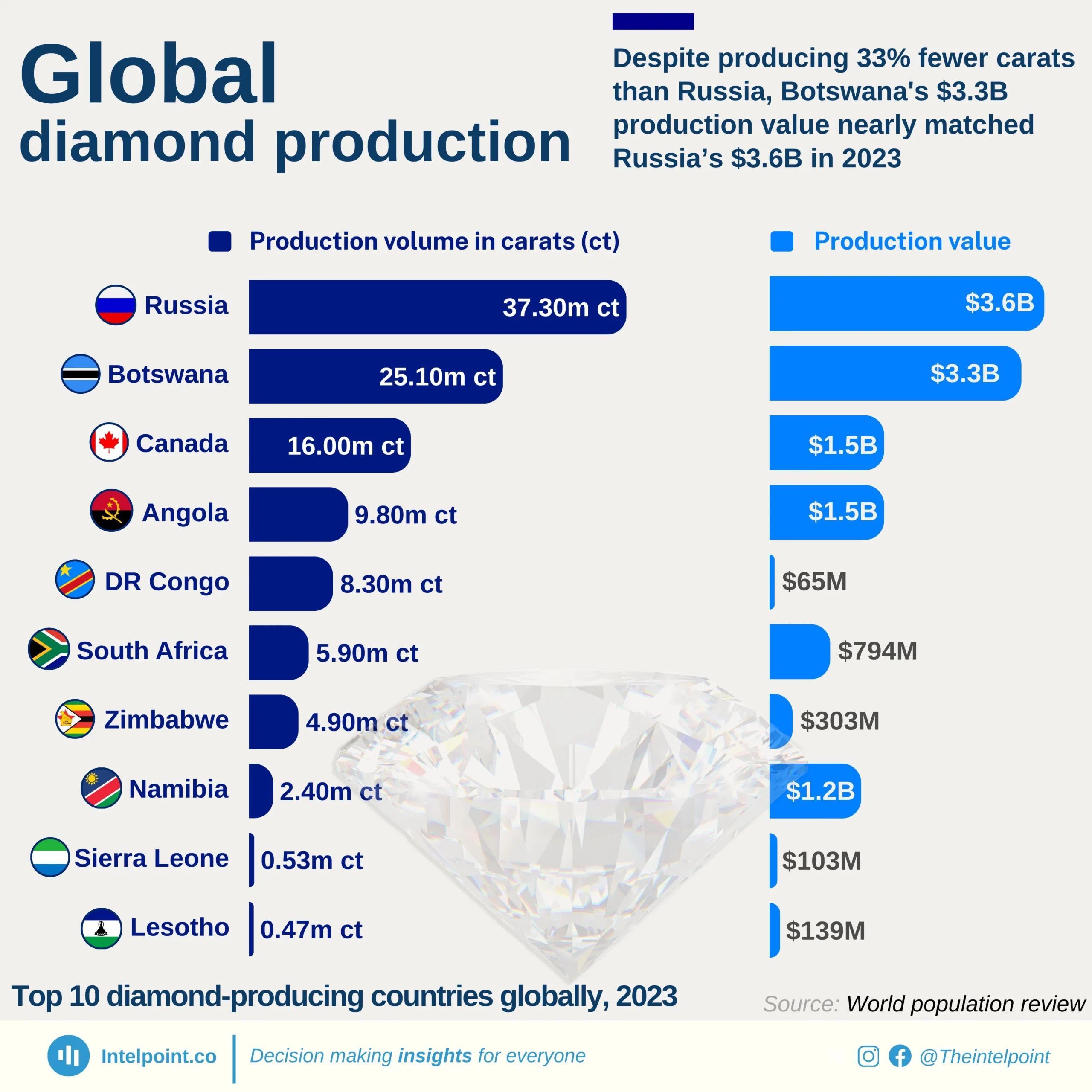

Russia is the volume leader with 37.3M carats, nearly 1.5× Botswana’s 25.1M carats.

Botswana punches above its weight: though producing 33% fewer carats than Russia, its output value almost matches Russia's due to higher value per carat price.

Eight of the top 10 producers are African (Botswana, Angola, DR Congo, South Africa, Zimbabwe, Namibia, Sierra Leone, Lesotho).

Low-volume producers like Namibia (2.4M ct → $1.2B) highlight how smaller deposits can yield high-value diamonds.

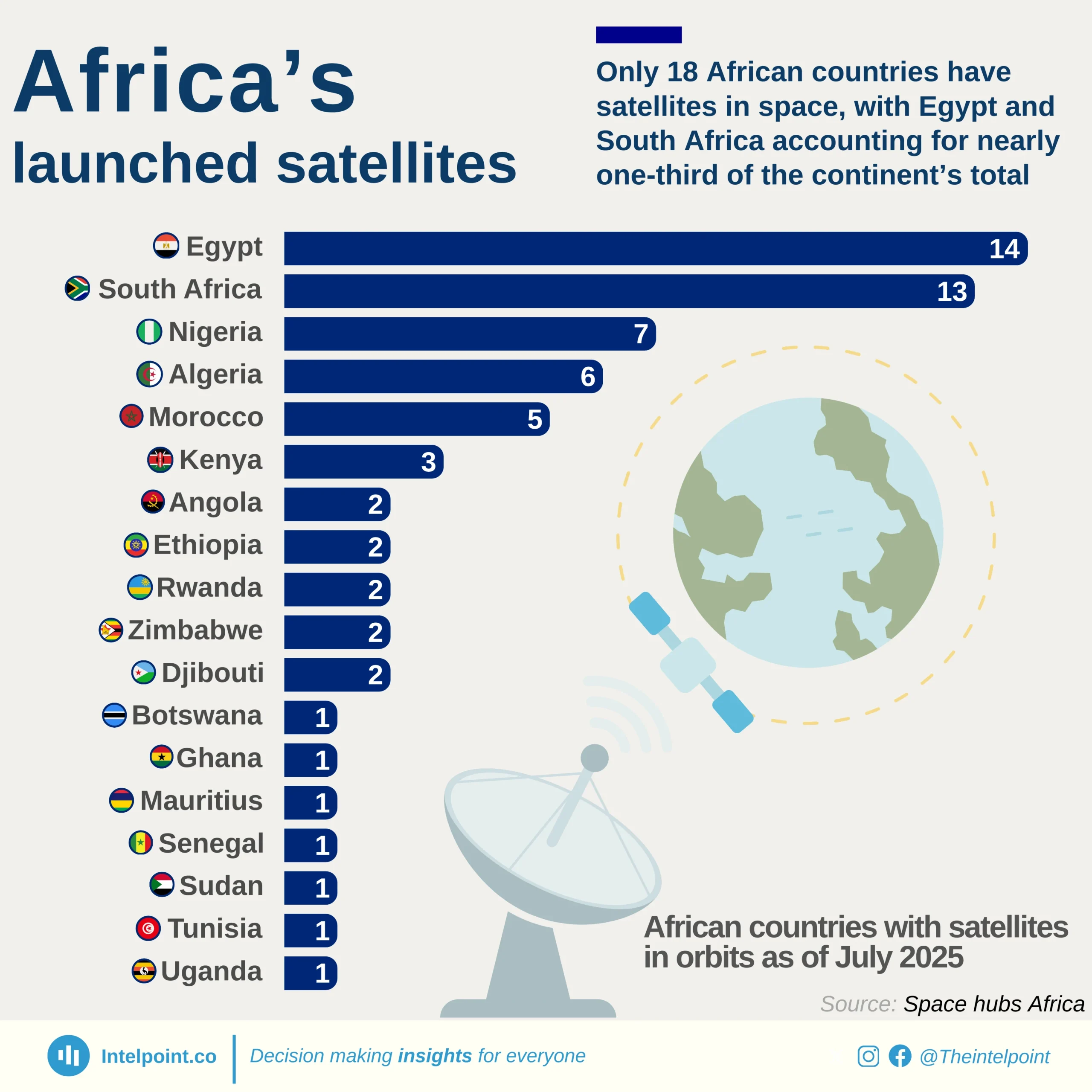

Egypt and South Africa dominate Africa’s space presence, with 14 and 13 satellites respectively, accounting for nearly one-third of the continent’s total.

Nigeria (7), Algeria (6), and Morocco (5) form the next tier, highlighting North and West Africa as emerging hubs in satellite development.

The majority of other African countries with satellites, including Rwanda, Ethiopia, Zimbabwe, Djibouti and Angola, have two satellites each.

Out of 54 African nations, only 18 have any satellites in orbit, underscoring the vast disparity in space investment and technological capacity across the continent.