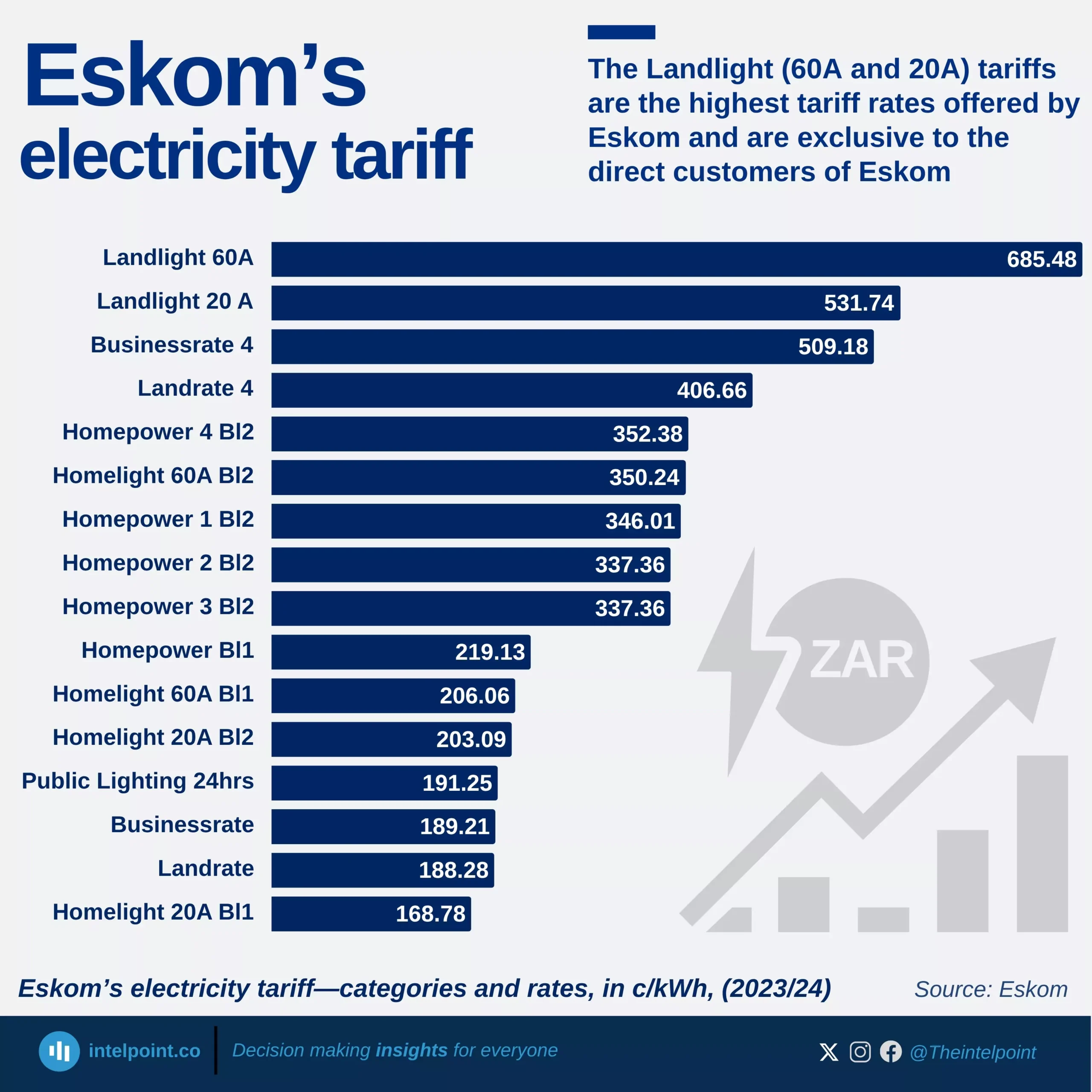

Over the years, Eskom has developed a range of tariff structures to cater to the diverse needs of its customers across South Africa. In the 2023/24 tariff year, Landlight tariffs, specifically the 60A and 20A variants, remain the highest charged rates, standing at 685.48 c/kWh and 531.74 c/kWh respectively. These tariffs are exclusive to direct (non-local authority) customers and are predominantly applied in rural areas where Eskom supplies electricity directly to end-users, without municipal intermediaries.

At the other end of the spectrum, the Homelight 20A Block 1 tariff, applicable to households consuming between 0–350 kWh, is the lowest, at 168.78 c/kWh. This affordability makes it ideal for lower-income or low-usage households, reinforcing Eskom's attempt to maintain accessibility in basic electricity consumption.

The high cost of the Landlight tariffs is compensated by the absence of several fixed charges typically included in other Eskom tariffs.