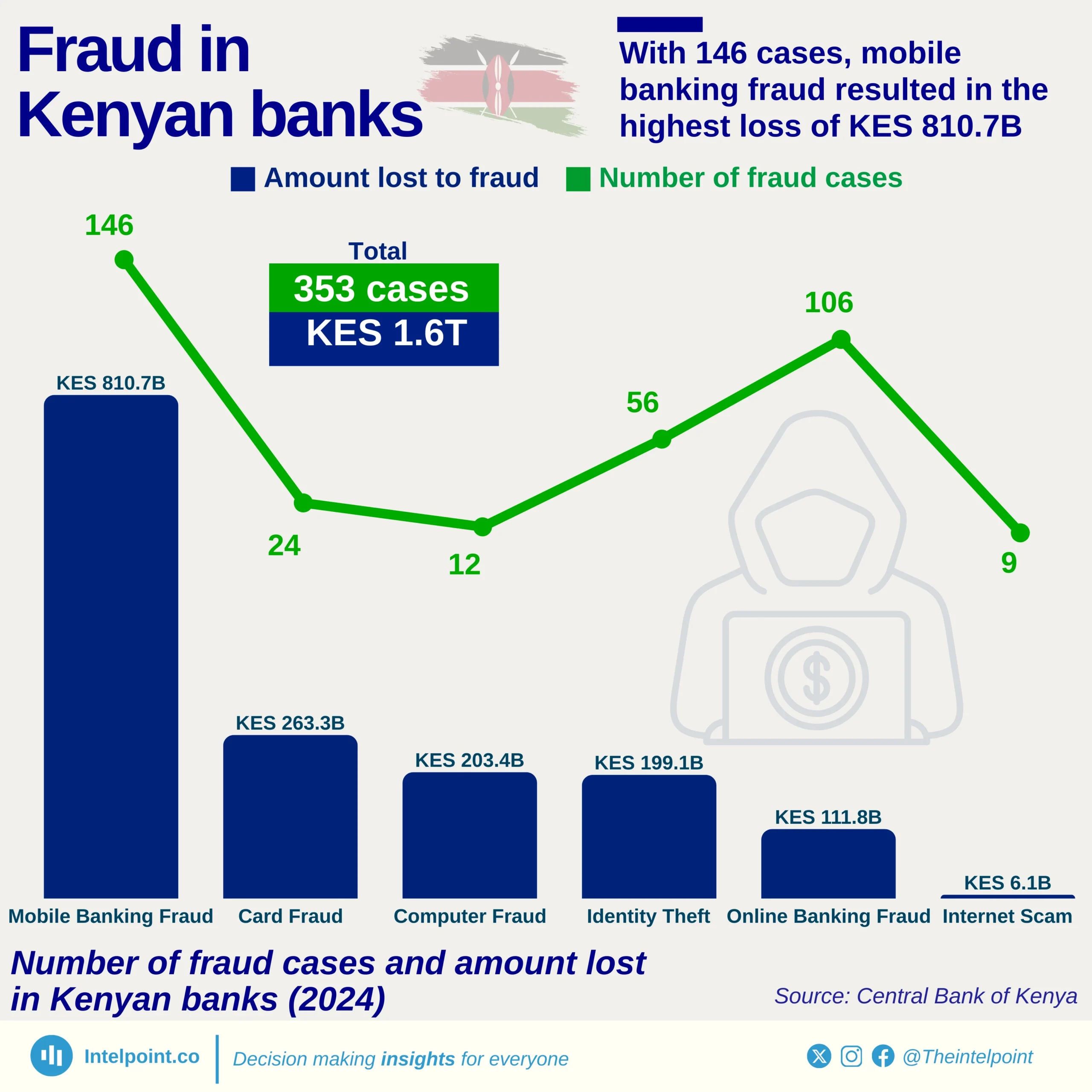

Kenya’s banking sector continues to grapple with rising fraud, with losses reaching KES 1.6 trillion in 2024 from 353 reported cases. Mobile banking fraud accounted for the highest loss at KES 810.7 billion—over half of the total losses.

This highlights the paradox of digital convenience. Just as mobile money has transformed daily life—whether it's paying for groceries, sending money to family, or covering school fees—it has also created new vulnerabilities. A single breach in mobile banking can cause losses in billions.

Fraud cases were also frequent in areas like online banking, which recorded 106 incidents, yet the losses (KES 111.8B) were far lower compared to mobile banking. Similarly, identity theft had 56 cases but resulted in KES 199.1B in losses. Card fraud, though with only 24 cases, caused KES 263.3B in damages, showing that some fraud types are highly efficient at draining funds with minimal attempts. At the other end, internet scams had just 9 cases, but still managed to cause KES 6.1B in losses.