Key takeaways:

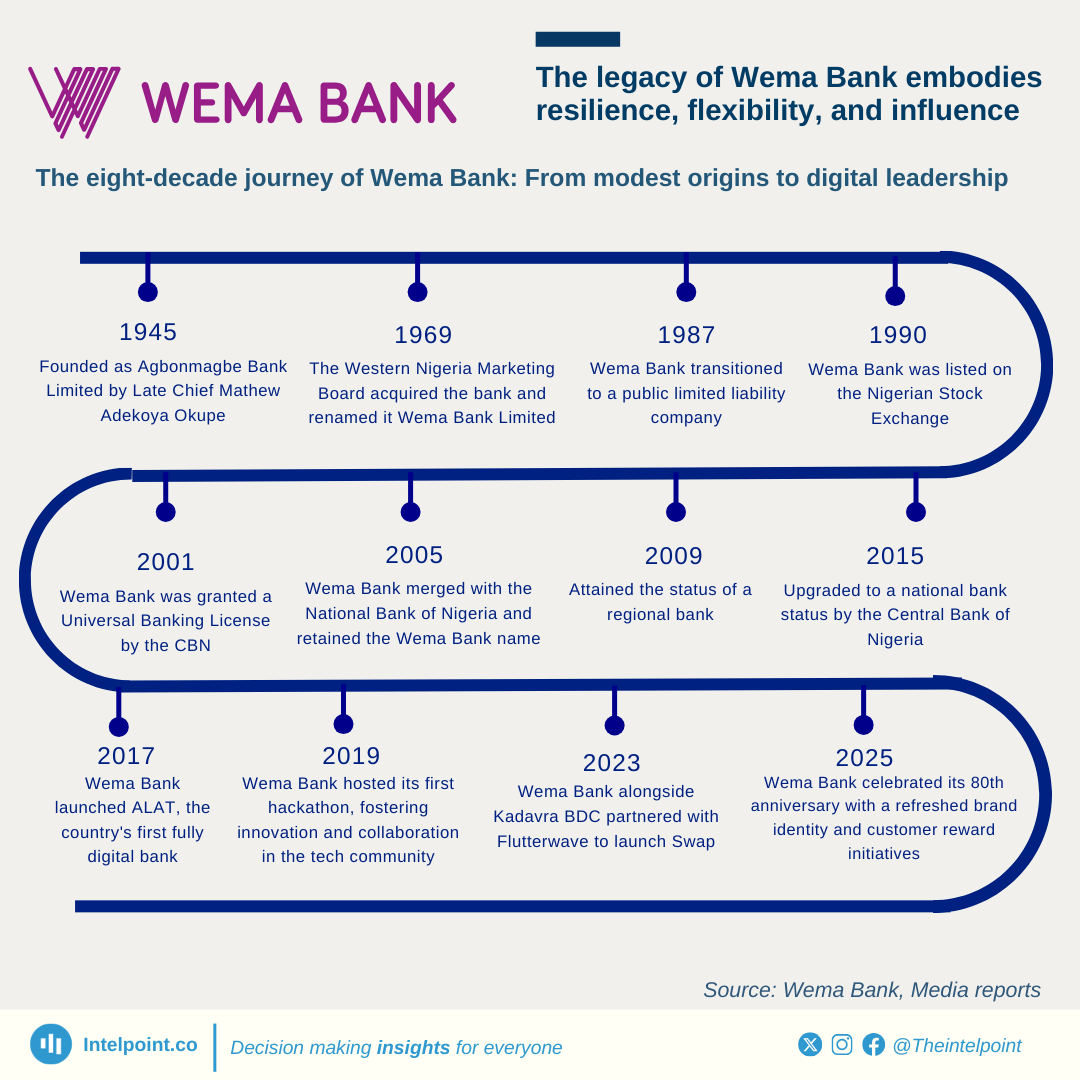

Wema Bank's journey commenced in 1945 when Chief Mathew Adekoya Okupe established Agbonmagbe Bank Limited. In 1969, it adopted the name Wema Bank Limited after its acquisition by the Western Nigeria Marketing Board.

The bank became a public limited liability company in 1987 and was listed on the Nigerian Stock Exchange in 1990. Wema Bank acquired a Universal Banking License in 2001, broadening its range of services. In 2005, Wema Bank merged with the National Bank of Nigeria and retained the Wema Bank name.

Following a strategic restructuring from 2009 to 2015, the bank secured a national banking license in 2015 and unveiled a new logo that represents synergy and innovation.

Showing its dedication to technological progress, Wema Bank launched ALAT in 2017, Nigeria's first fully digital bank. In celebration of its 80th anniversary in 2025, Wema Bank revealed a refreshed brand identity and introduced customer reward programmes, highlighting its legacy of resilience and innovation.