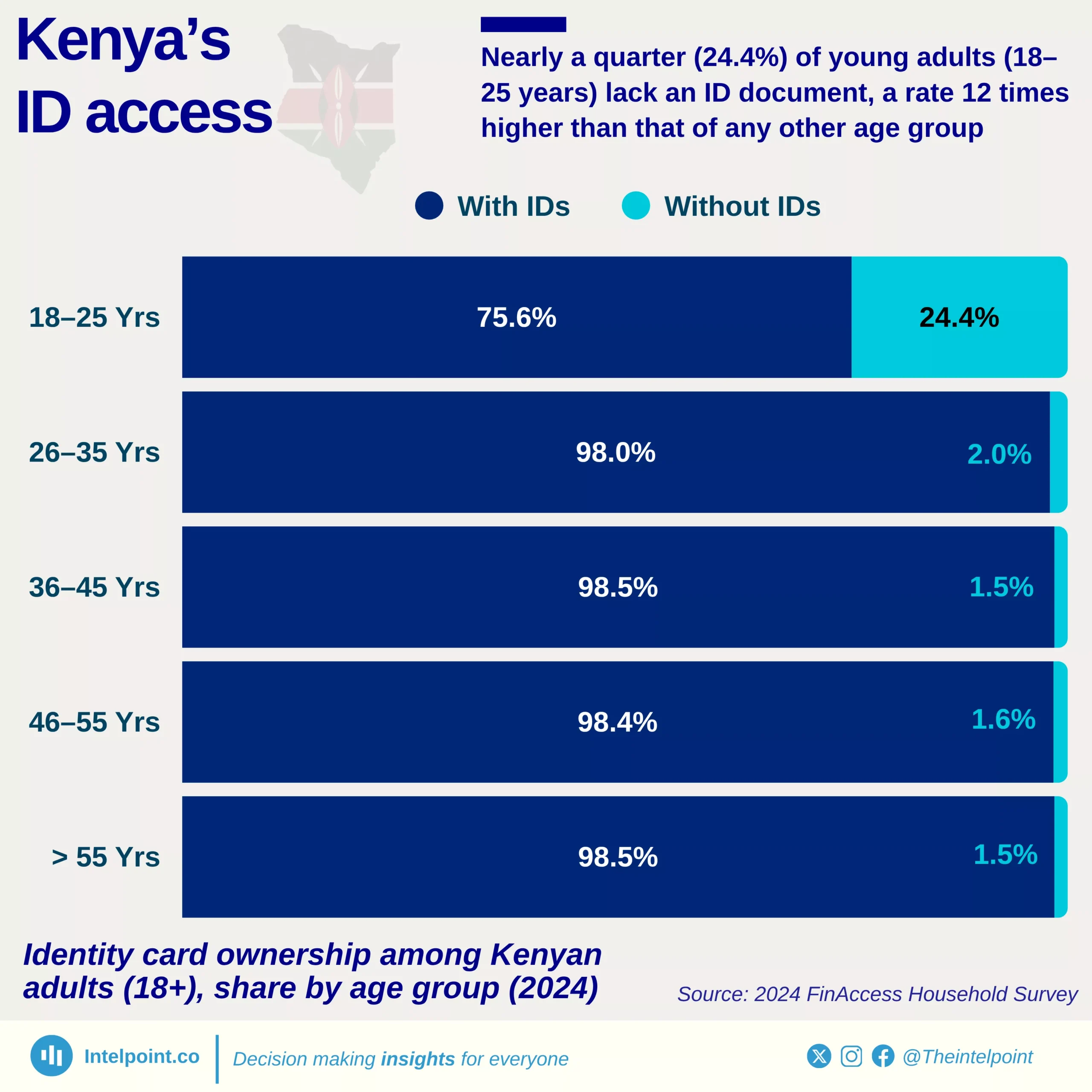

The 2024 FinAccess Household Survey revealed a significant gap in Kenya’s identity card (ID) ownership among young adults aged 18–25 years. While nearly all older Kenyans possess an ID, 24.4% of those aged 18–25 still lack one, making this group 12 times more likely to be without identification compared to other age groups. This is a key challenge in Kenya’s efforts to expand financial inclusion and access to government services, both of which often depend on formal identification.

The difference in ID access between younger and older adults highlights a critical transition challenge faced by Kenya’s youth. Many young adults struggle with delays or bureaucratic bottlenecks in obtaining IDs after reaching 18, especially those in rural areas or informal settlements.