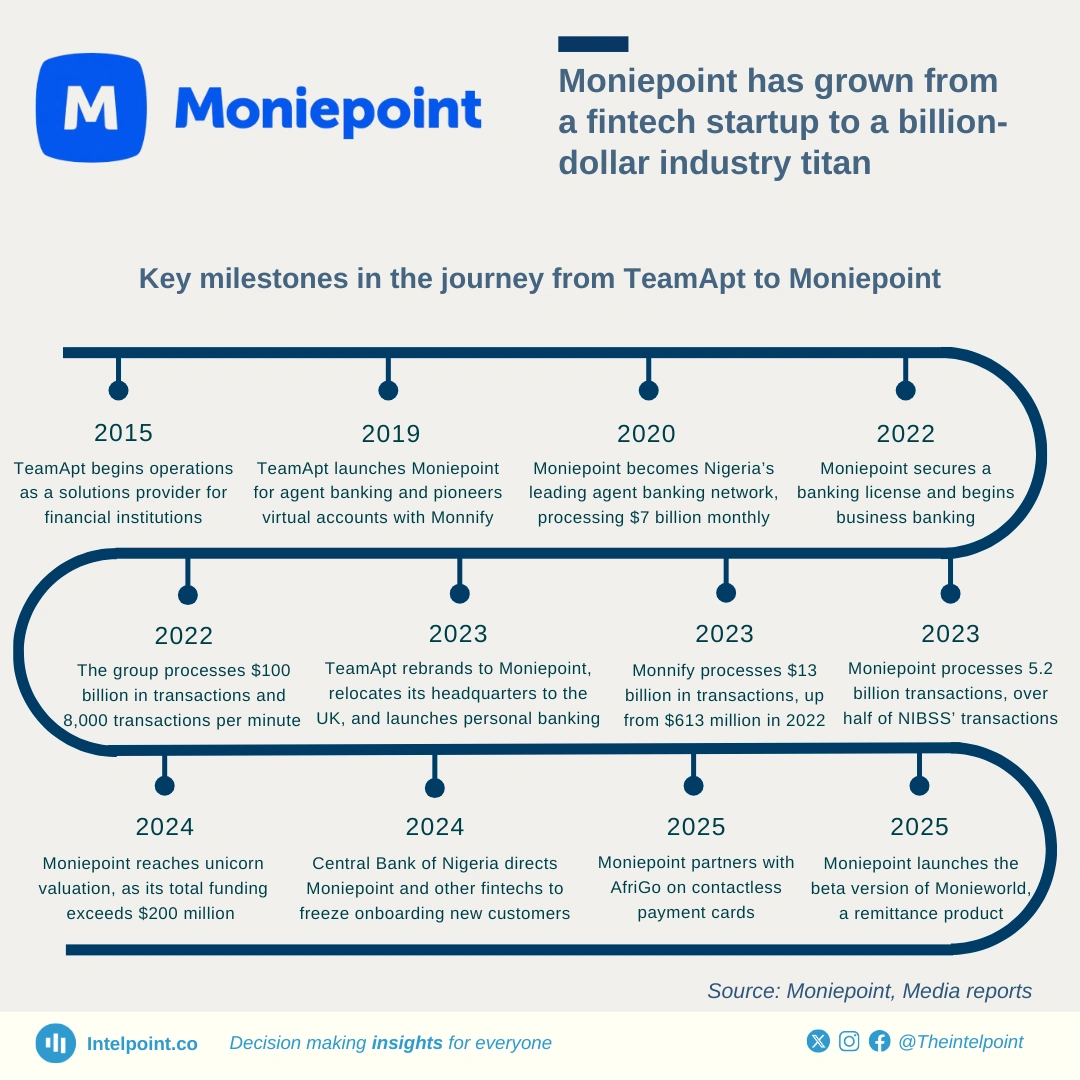

Moniepoint’s transformation from TeamApt to a fintech unicorn has been marked by significant milestones. Starting in 2015, the company shifted its focus to agent banking in 2019 and quickly became a dominant player, processing $7 billion monthly by 2020. The acquisition of a banking license in 2022 led to a surge in transactions, reaching 5.2 billion that year.

In 2023, the company expanded into personal banking, relocated its headquarters to the UK, and saw Monnify’s transaction volume jump to $13 billion. By 2024, Moniepoint had surpassed $200 million in funding and attained unicorn status. Looking ahead to 2025, its focus will include contactless payments and remittance services through Monieworld.