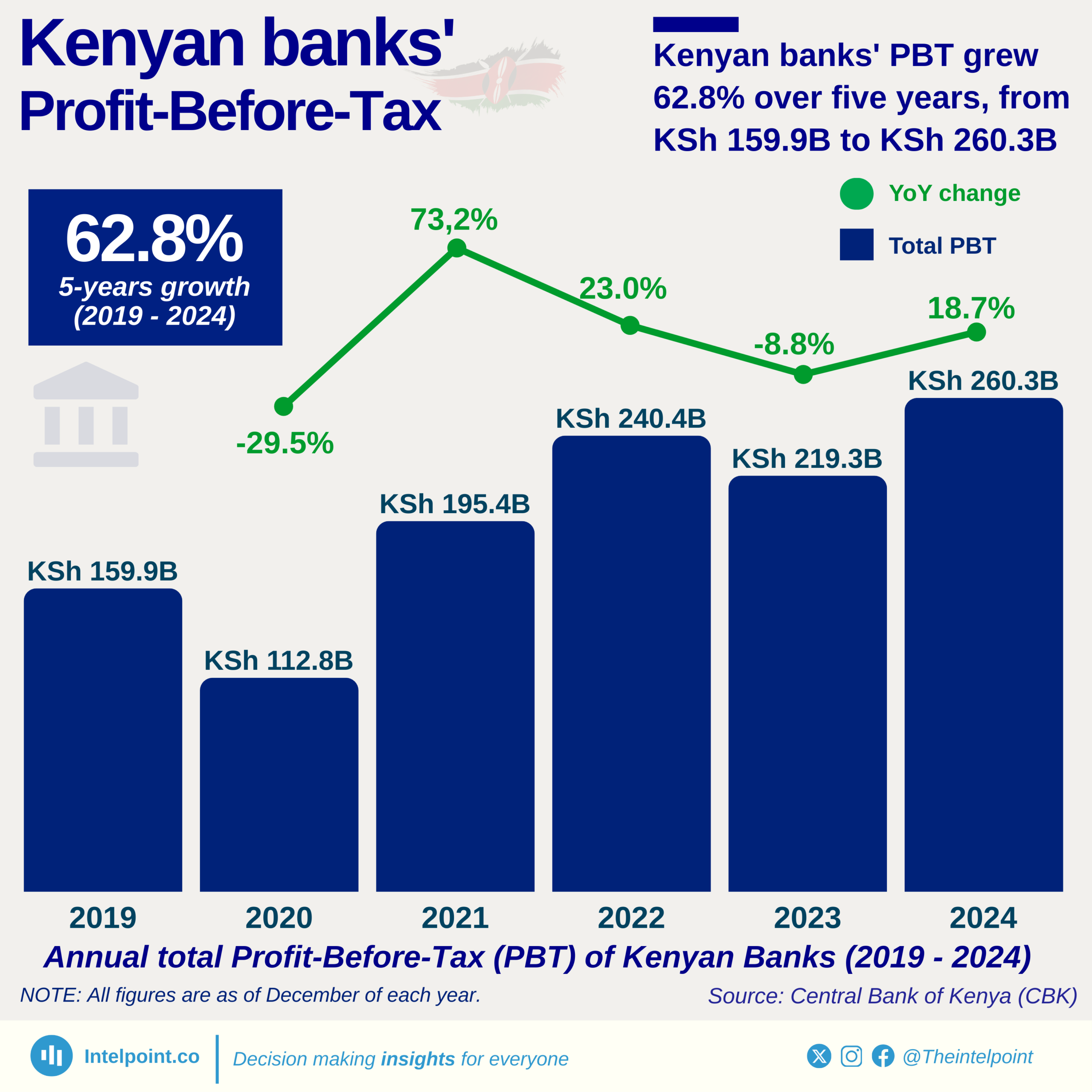

Kenyan banks have shown remarkable resilience over the past five years, with their total Profit-Before-Tax (PBT) growing by 62.8%, rising from KSh 159.9 billion in 2019 to KSh 260.3 billion in 2024. This growth reflects the sector’s ability to recover from shocks, adapt to changing market conditions, and maintain profitability despite periods of volatility. While the trend has not been consistently upward year-on-year, the overall trajectory underscores the strength of the banking industry.

The sharpest drop came in 2020, when PBT fell by 29.5% to KSh 112.8 billion. This period coincided with the economic disruptions of the COVID-19 pandemic. Yet, by 2021, banks bounced back strongly, recording a 73.2% increase in profits, signalling recovery and renewed market confidence. This rebound illustrates how external shocks may slow growth temporarily, but do not necessarily derail long-term sector performance.