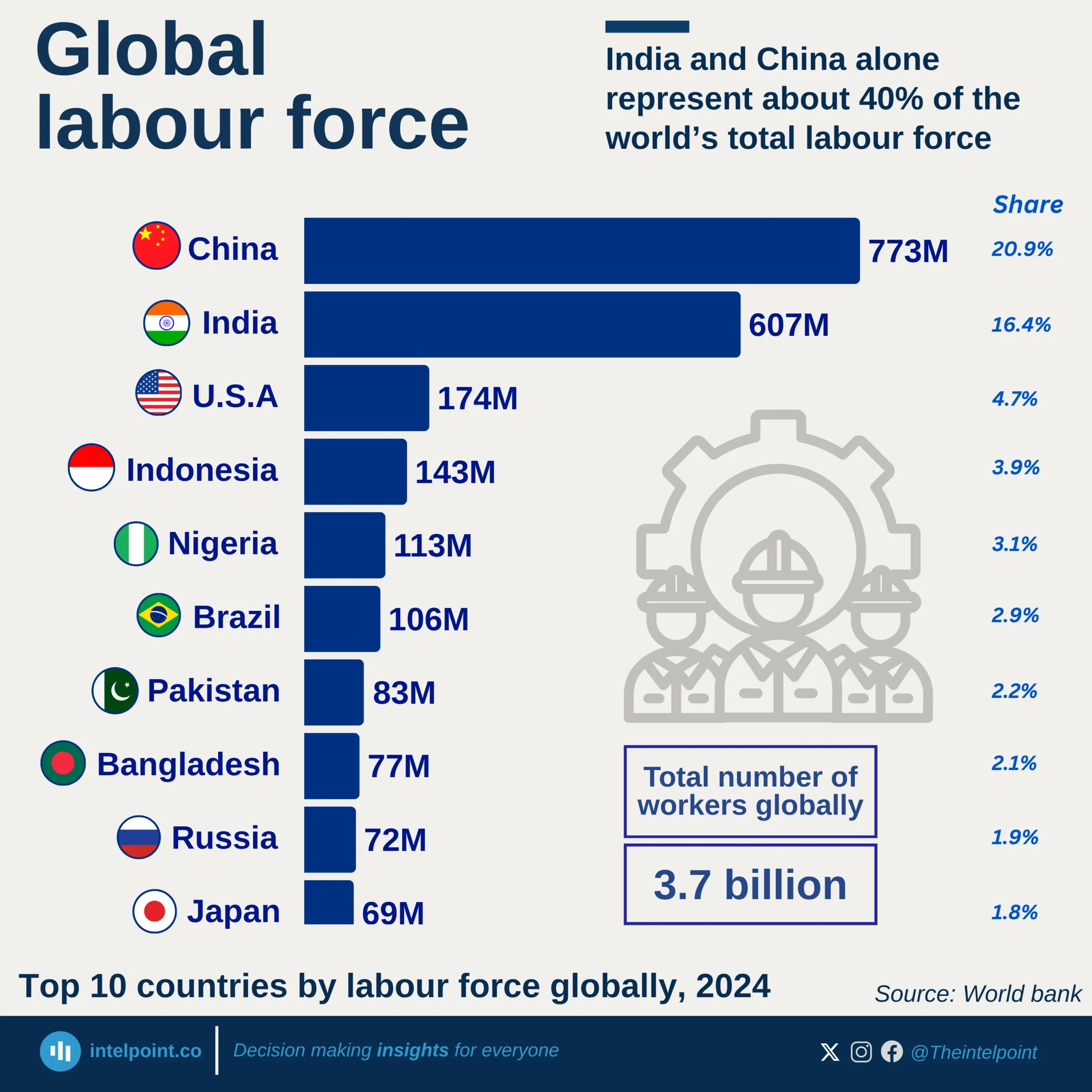

China (773M) and India (607M) together make up for about 40% of the world’s total labour force.

Nigeria ranks 5th globally with 113 million workers, the largest in Africa and only African country in the top 10.

Asia dominates, accounting for over 47% of global workers, highlighting the region’s population and production strength.

The U.S.A. (174M) ranks third, representing just about 5% of global labour but producing almost a quarter of global GDP, proving productivity, not size, drives wealth.

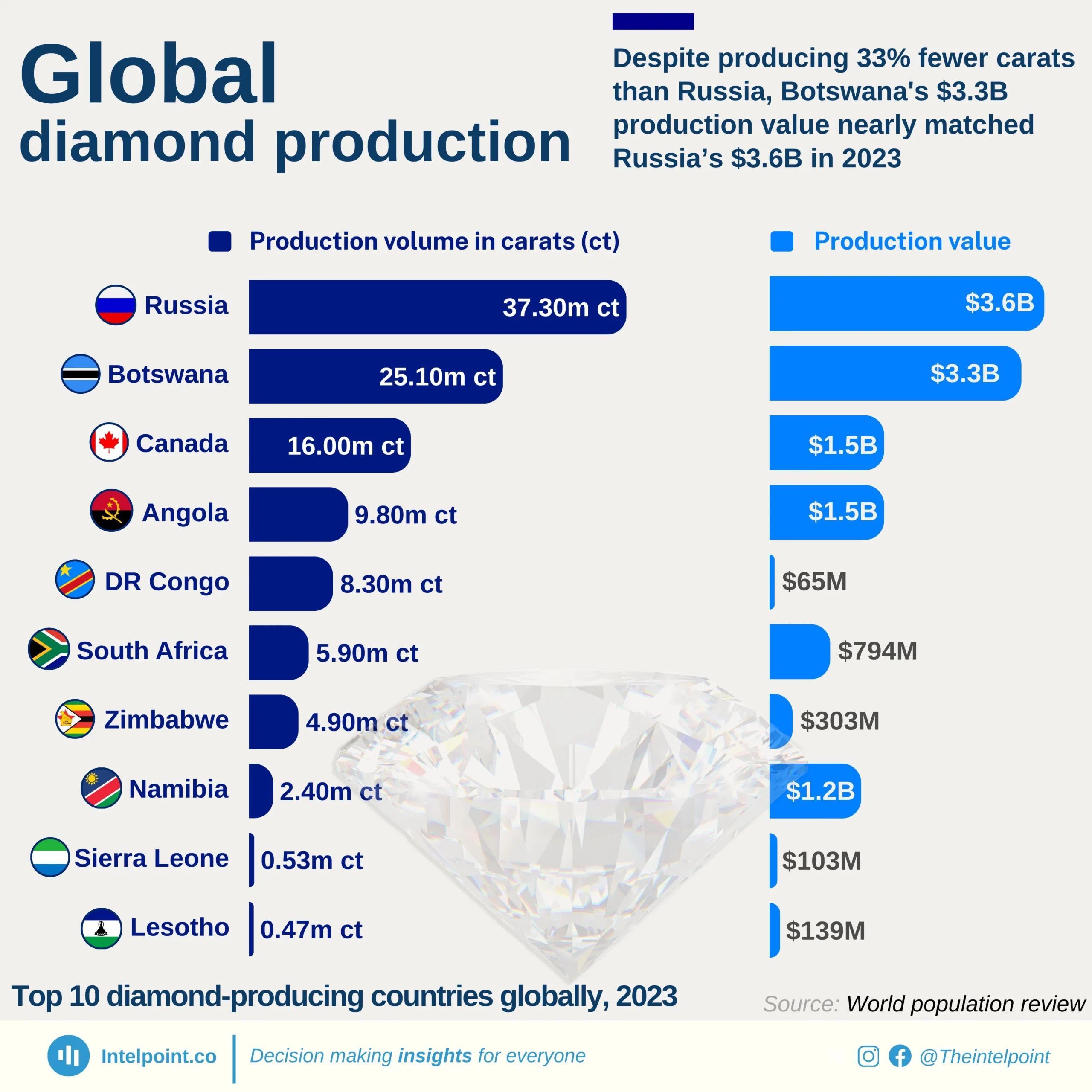

Russia is the volume leader with 37.3M carats, nearly 1.5× Botswana’s 25.1M carats.

Botswana punches above its weight: though producing 33% fewer carats than Russia, its output value almost matches Russia's due to higher value per carat price.

Eight of the top 10 producers are African (Botswana, Angola, DR Congo, South Africa, Zimbabwe, Namibia, Sierra Leone, Lesotho).

Low-volume producers like Namibia (2.4M ct → $1.2B) highlight how smaller deposits can yield high-value diamonds.

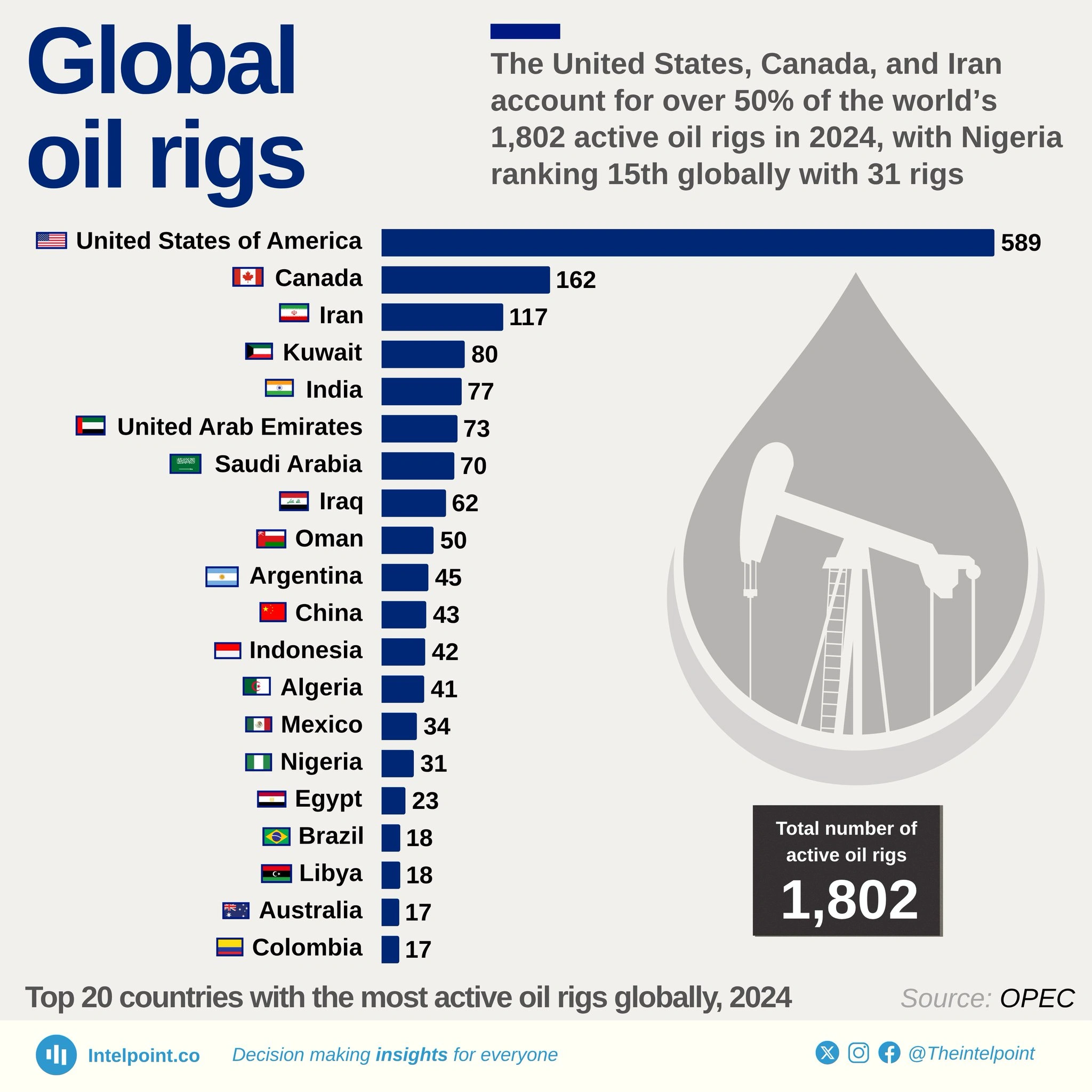

The United States remains the undisputed leader with 589 active rigs, accounting for nearly a third of all rigs worldwide in 2024.

Canada (162 rigs) and Iran (117 rigs) follow as the second and third highest contributors to global drilling activity.

Middle Eastern producers dominate the top 10, with Kuwait (80), UAE (73), Saudi Arabia (70), Iraq (62), and Oman (50) collectively operating 335 rigs.

Nigeria ranks 15th globally with 31 active rigs, making it one of only two African nations in the global top 20.

The top 10 countries account for over 75% of the world’s active rigs, reflecting the continued concentration of drilling infrastructure in a handful of key oil-producing regions.

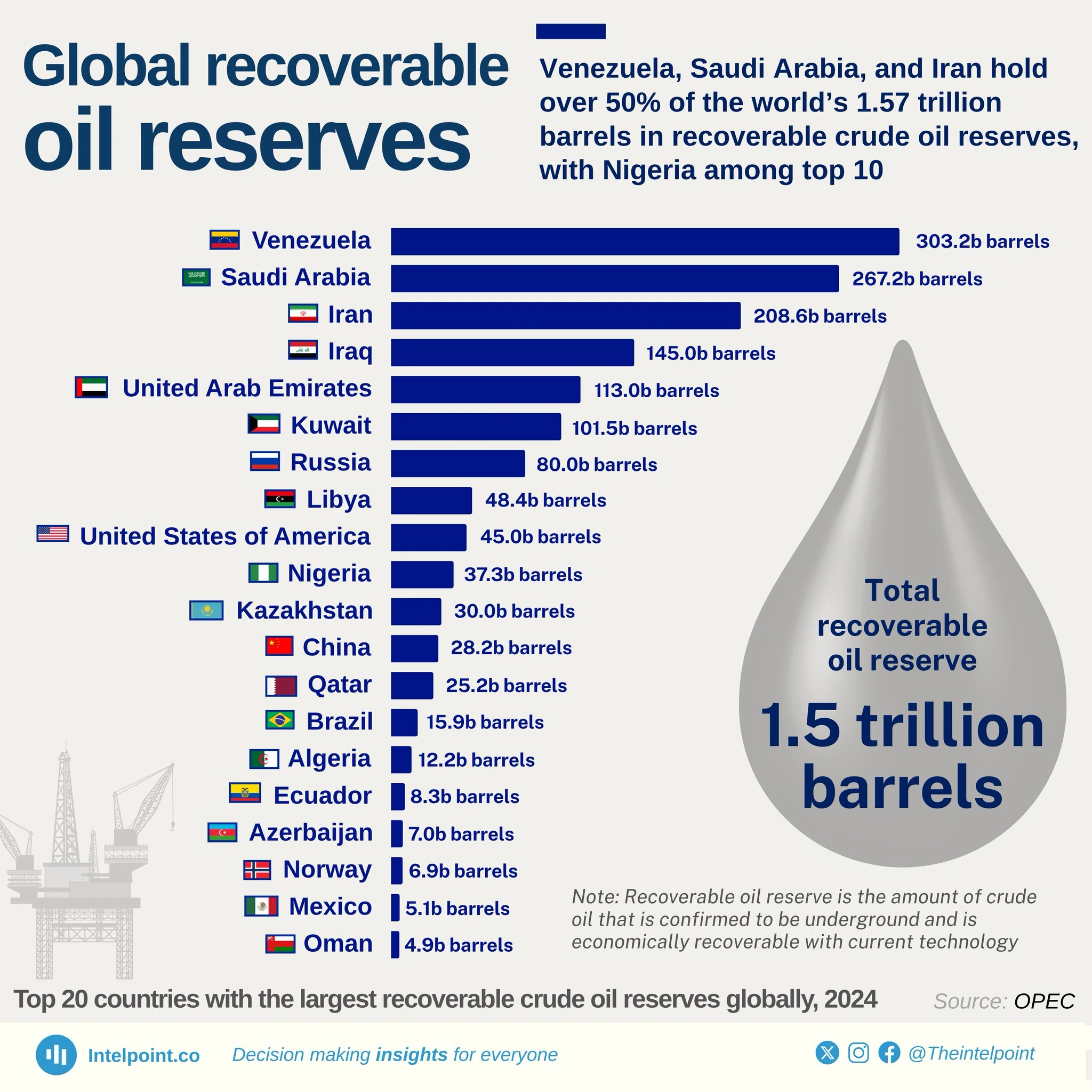

The world’s total proven recoverable crude oil reserves stand at 1.57 trillion barrels in 2024.

Venezuela, Saudi Arabia, and Iran collectively hold over 50% of these reserves, with 303.2B, 267.2B, and 208.6B barrels respectively.

Nigeria ranks 10th globally with 37.3 billion barrels, placing it ahead of other major producers like Kazakhstan, China, and Brazil.

The majority of the largest reserves are concentrated in Middle Eastern and South American countries, with only a few top holders located in North America, Africa, and Asia.

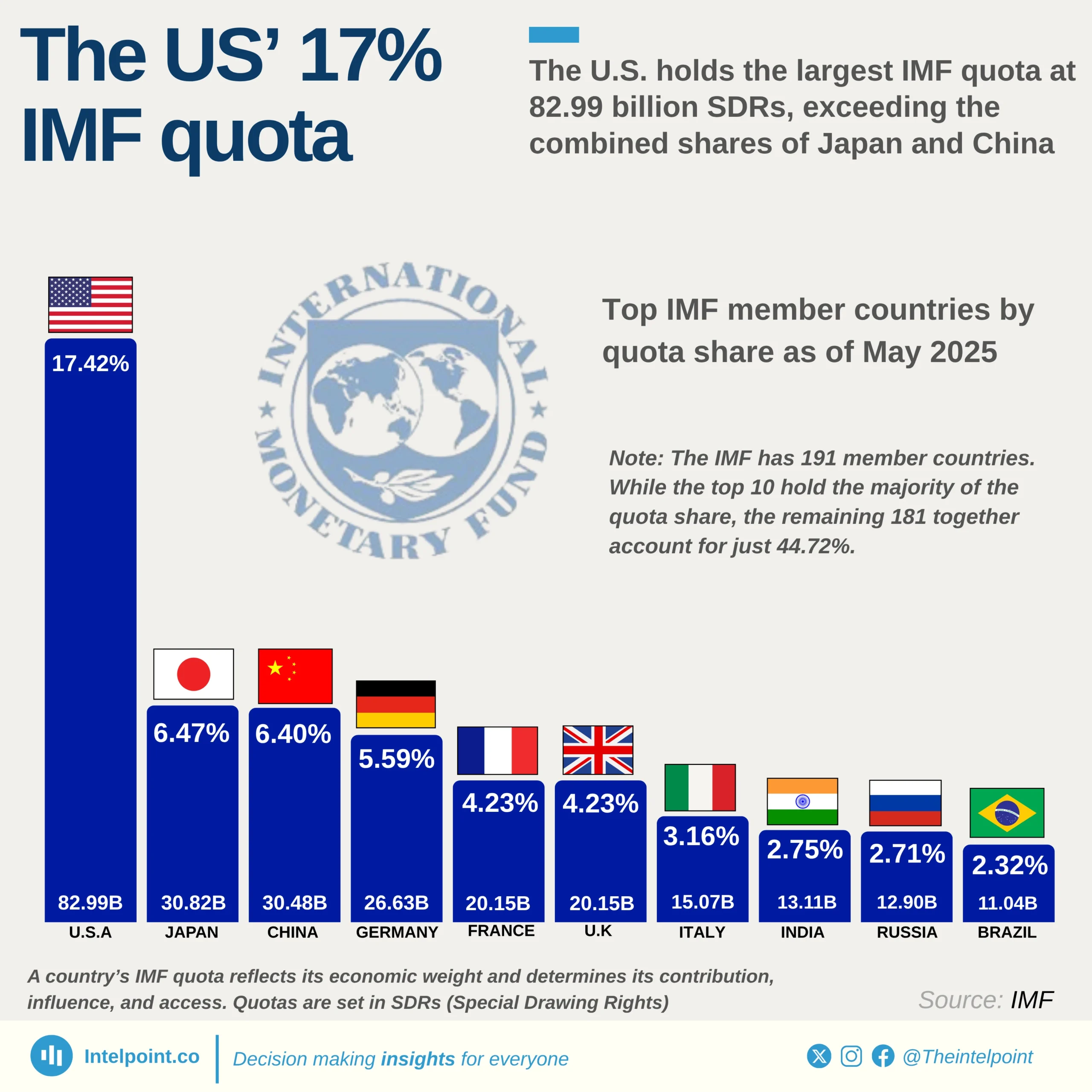

The United States holds the largest IMF quota by far, with 82,994.2 billion SDRs, accounting for 17.42%, more than double the quota of any other country.

Japan, China, and Germany follow as the next largest contributors, each holding between 5.5% and 6.5% of total quota shares.

European countries (Germany, France, the U.K., Italy) collectively maintain a strong presence, together accounting for nearly 17.21%, almost equal to the U.S. alone.

Emerging economies like India and Russia have relatively modest shares (2.75% and 2.71%, respectively) despite their growing roles in global economic affairs, indicating an imbalance between global influence and IMF voting power.