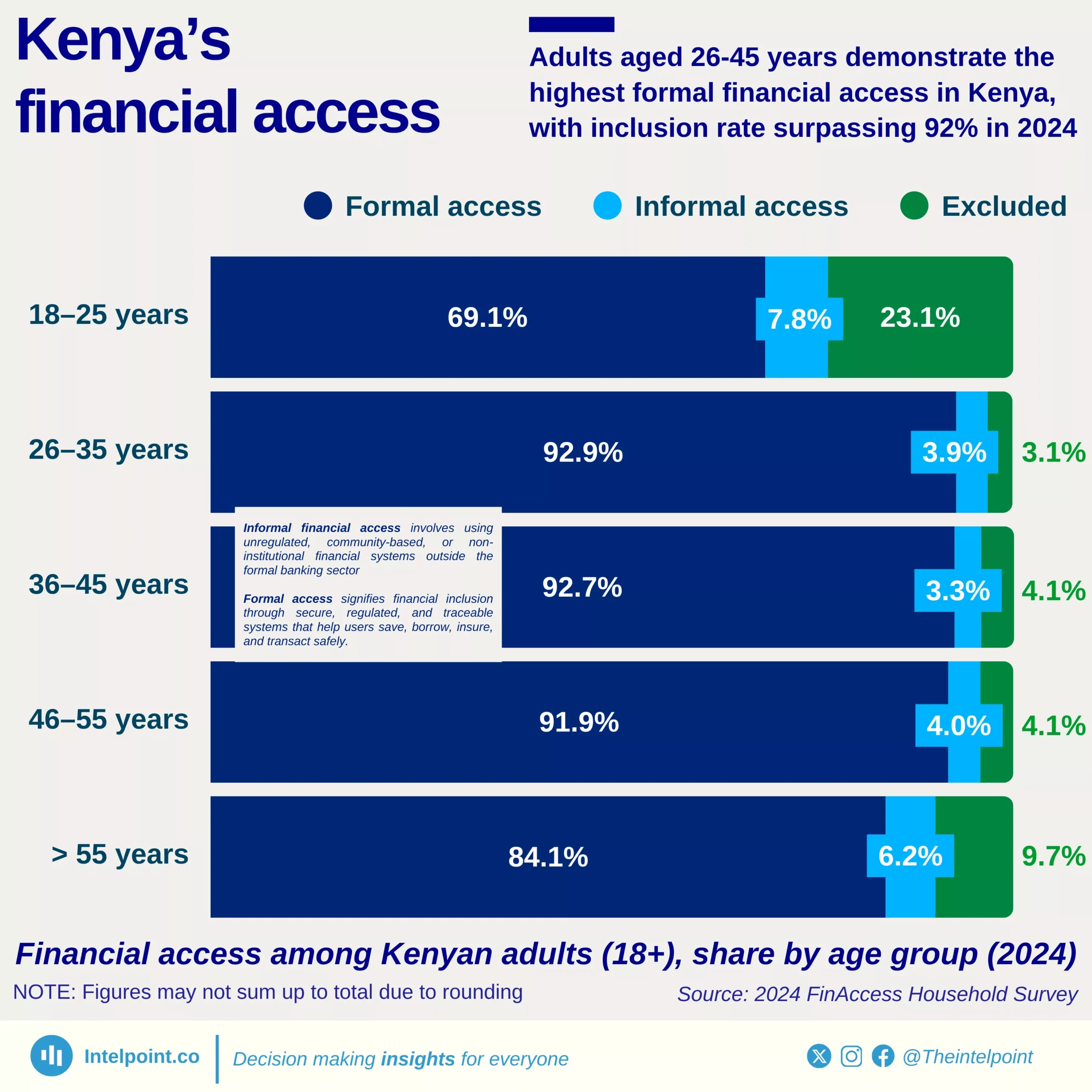

Adults aged 26–35 years have the highest formal financial access in Kenya at 92.9%. The 36–45 age group follows closely with 92.7% formal inclusion, highlighting strong access among the middle-aged population.

Young adults (18–25 years) remain the most financially excluded group, with 23.1% still outside the financial system. Older adults (above 55 years) also show weaker inclusion, with 84.1% formal access and 9.7% exclusion. Informal access remains relatively low across all age groups, signalling the dominance of formal channels. Kenya’s financial inclusion story continues to evolve positively, and data from 2024 shows that adults aged 26–45 years have the highest formal financial access, with inclusion rates surpassing 92%.

This indicates that the country’s economically active population is deeply integrated into formal financial systems such as banks, mobile money, and insurance platforms. In contrast, younger adults (18–25 years) and older adults (above 55 years) show relatively lower levels of formal inclusion, underscoring the uneven spread of financial access across age groups. This suggest that Kenya’s digital financial revolution—driven by platforms like M-Pesa and increased mobile penetration—has largely benefitted those within their prime working years.

These individuals often have regular incomes, business activities, or families to support, making them more likely to use savings accounts, mobile money, and credit facilities.