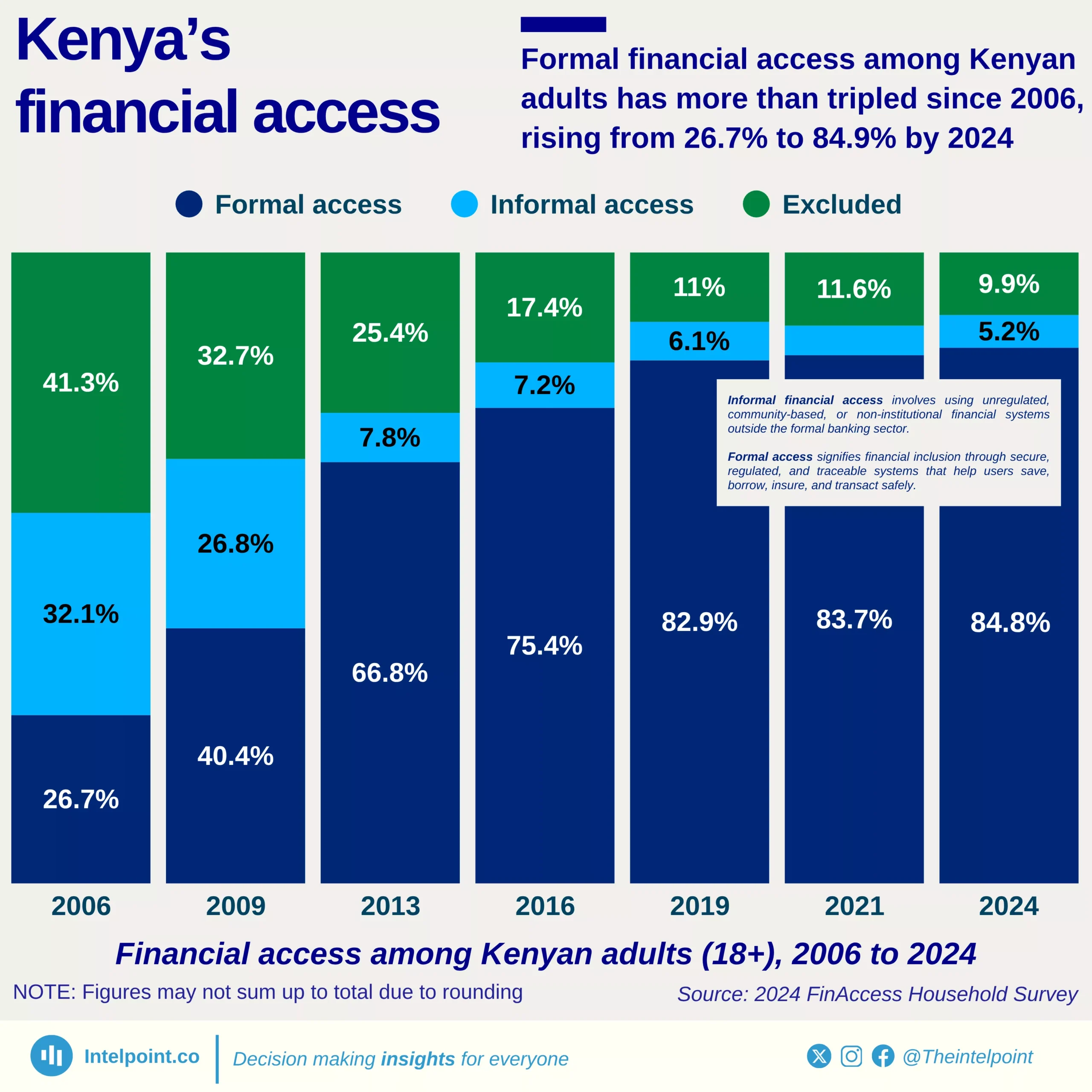

Kenya’s financial landscape has undergone a remarkable transformation in less than two decades. Formal financial access among adults has more than tripled, rising from 26.7% in 2006 to 84.9% in 2024. This shift underscores Kenya’s position as one of Africa’s leaders in financial inclusion, primarily driven by innovations in mobile banking and digital financial services.

Over time, the country has witnessed a steady decline in the number of financially excluded adults, from 41.3% in 2006 to just 9.9% in 2024. This progress reflects deliberate policy efforts, technological adoption, and the success of platforms like M-Pesa, which have helped bridge the gap between traditional banking and informal systems. By making financial services more accessible and secure, Kenya has demonstrated how innovation can drive inclusion even in developing economies.