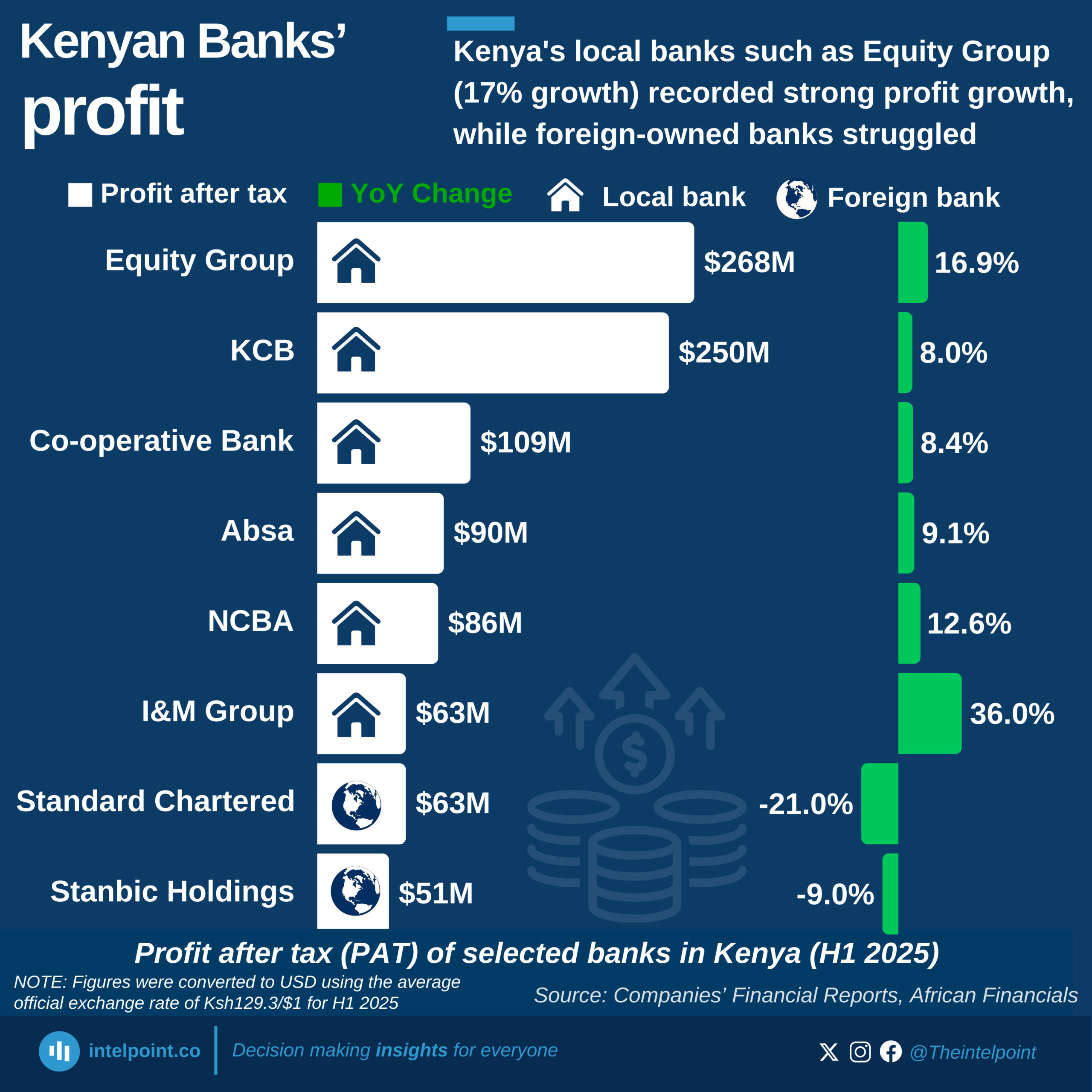

Kenya’s banking sector showed a sharp contrast in performance between local and foreign-owned banks in the first half of 2025. Local banks such as Equity Group, KCB, and Co-operative Bank continued to post strong profits, with Equity Group leading at $268 million, boosted by a 17% year-on-year growth. In contrast, foreign banks like Standard Chartered and Stanbic Holdings struggled, recording profit declines of 21% and 9% respectively. This divergence highlights the resilience of local banks in navigating Kenya’s economic and regulatory environment.

The data also shows that mid-tier banks like NCBA and Absa are steadily strengthening their positions, recording double-digit and high single-digit profit growth, respectively. Interestingly, I&M Group posted the fastest growth at 36%, although from a smaller profit base compared to the larger banks.