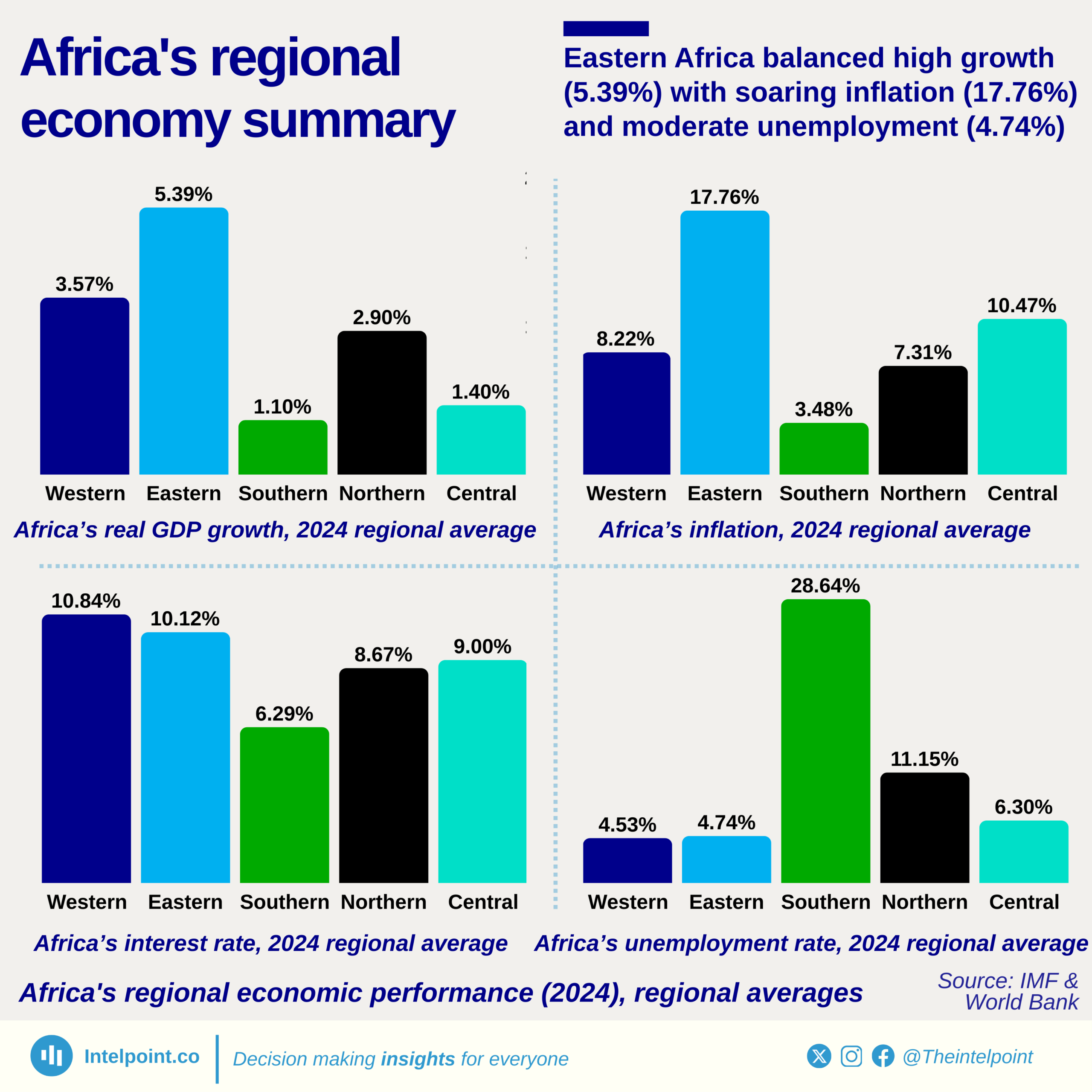

Eastern Africa showed a dynamic economic profile in 2024, showcasing the highest real GDP growth rate at 5.39%, but also grappling with the continent’s highest inflation at 17.76%. This reflected a region growing quickly but also facing the challenges of overheating economies, price instability, and rising cost of living. While unemployment in Eastern Africa remained relatively moderate at 4.74%, the inflationary pressure could pose a long-term risk if not managed.

In contrast, Southern Africa experienced the continent’s slowest growth at 1.10%, yet it also enjoyed the lowest inflation at 3.48%. However, the region struggled with a crippling unemployment rate of 28.64%, which dwarfed all other regions and highlighted a deep structural challenge. Western Africa offered a more balanced picture, with decent growth at 3.57%, moderate inflation (8.22%), and one of the lowest unemployment rates at 4.53%.