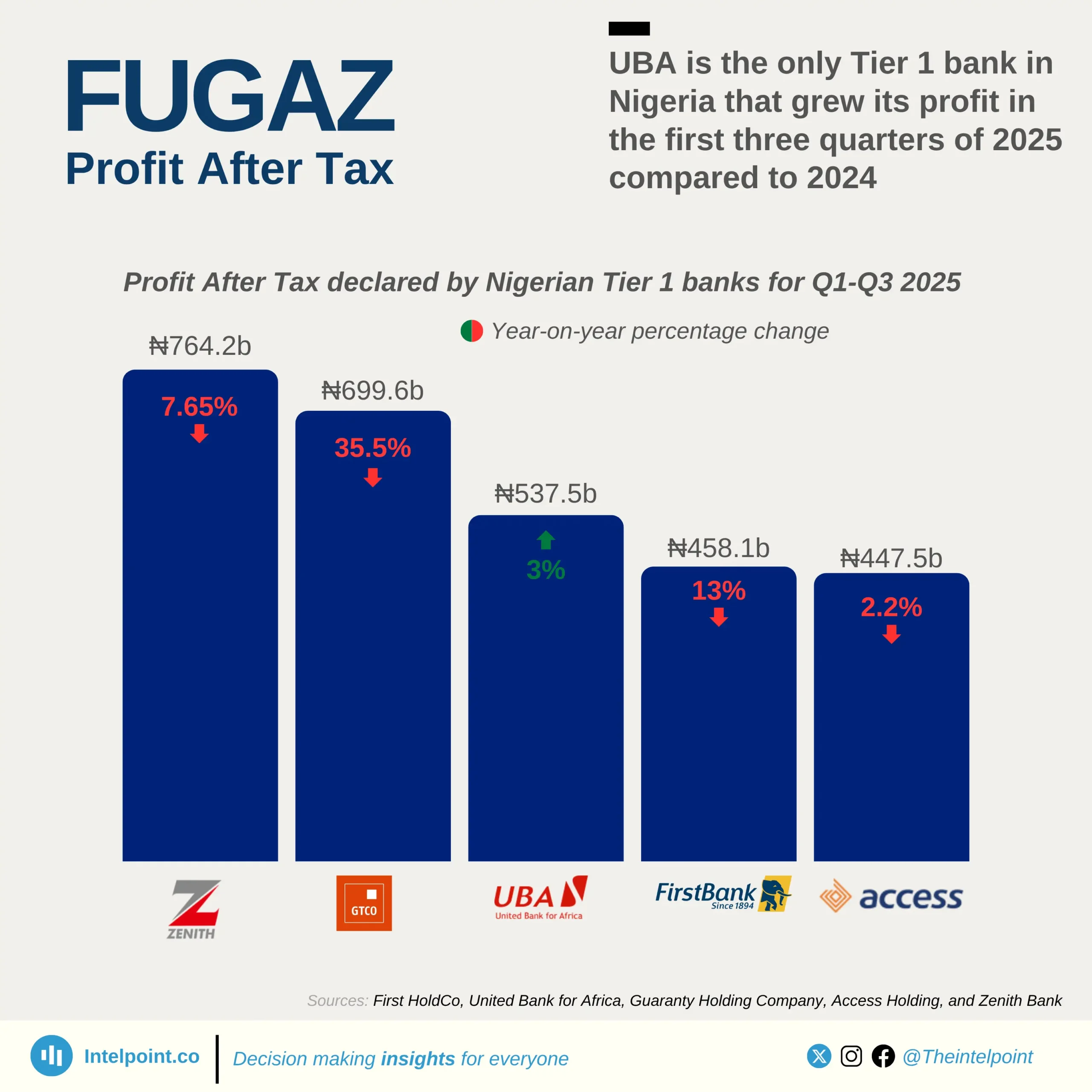

FirstBank, Nigeria’s oldest banking institution, has evolved significantly since its establishment in 1894. Initially operating as the Bank of British West Africa, it underwent multiple name changes and ownership shifts, reflecting broader economic and regulatory developments. The 1969 indigenisation policy led to its local incorporation, and in 1979, it was renamed First Bank of Nigeria.

The bank continued to modernise, restructuring into a holding company in 2012. In recent years, governance reforms and strategic moves have shaped its trajectory, with FBN Holdings rebranding to FirstHoldCo and the bank announcing the construction of a new headquarters at Eko Atlantic City. These changes highlight FirstBank’s enduring presence and adaptability in Nigeria’s financial landscape.