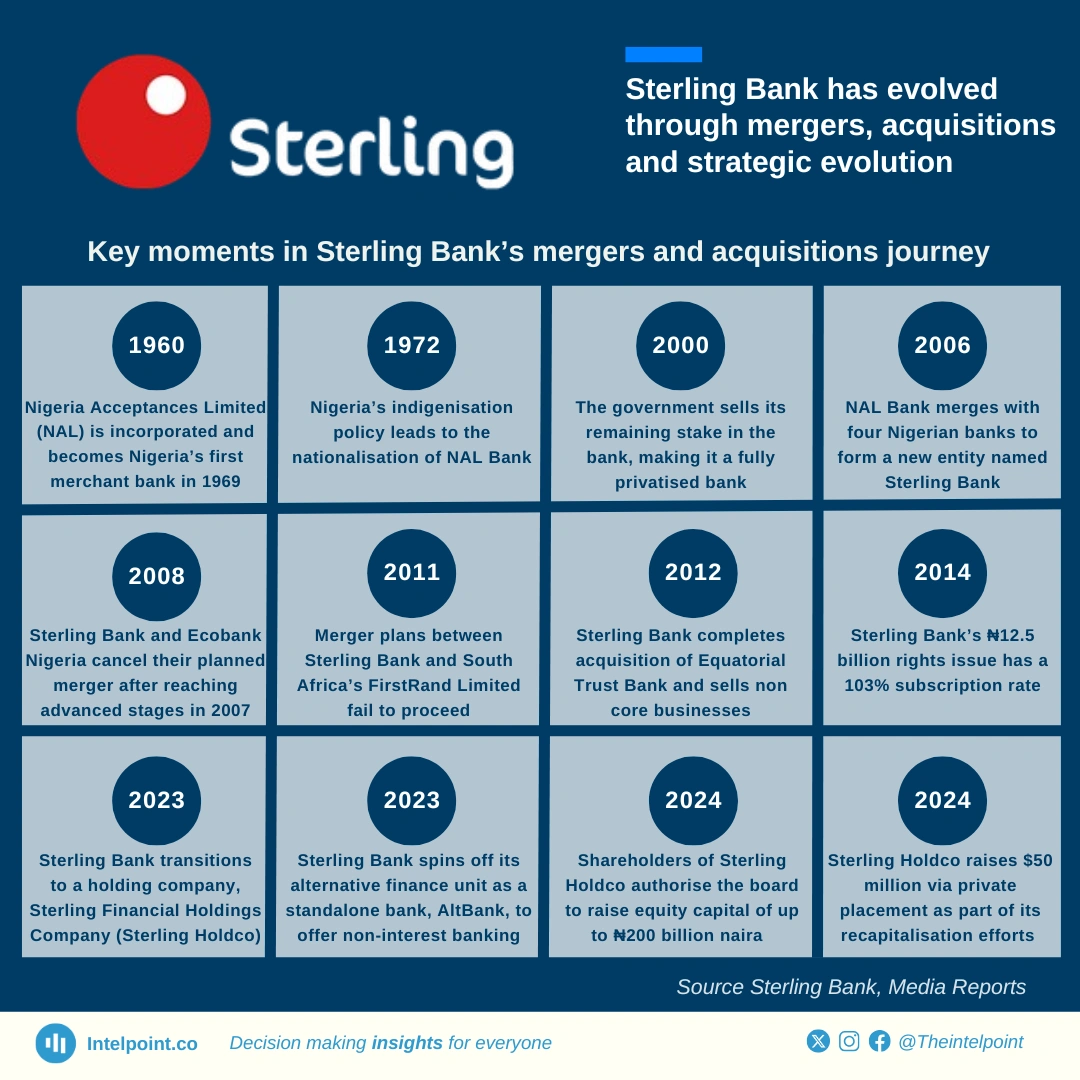

Sterling Bank’s history reflects a series of strategic shifts, including mergers, acquisitions, and restructuring. It began as Nigeria Acceptances Limited in 1960, then became a merchant bank in 1969. The nationalisation policy of 1972 placed the bank under government control until it was fully privatised in 2000. A landmark merger in 2006 saw NAL Bank combine with four other Nigerian banks to form Sterling Bank.

Over the years, Sterling pursued various mergers and acquisitions, including its successful takeover of Equatorial Trust Bank in 2012. In 2023, it transitioned into a holding company, Sterling Holdco, while spinning off AltBank as a standalone entity. Looking ahead, Sterling is strengthening its financial position with a ₦200 billion equity raise, aligning with Nigeria’s evolving banking landscape.