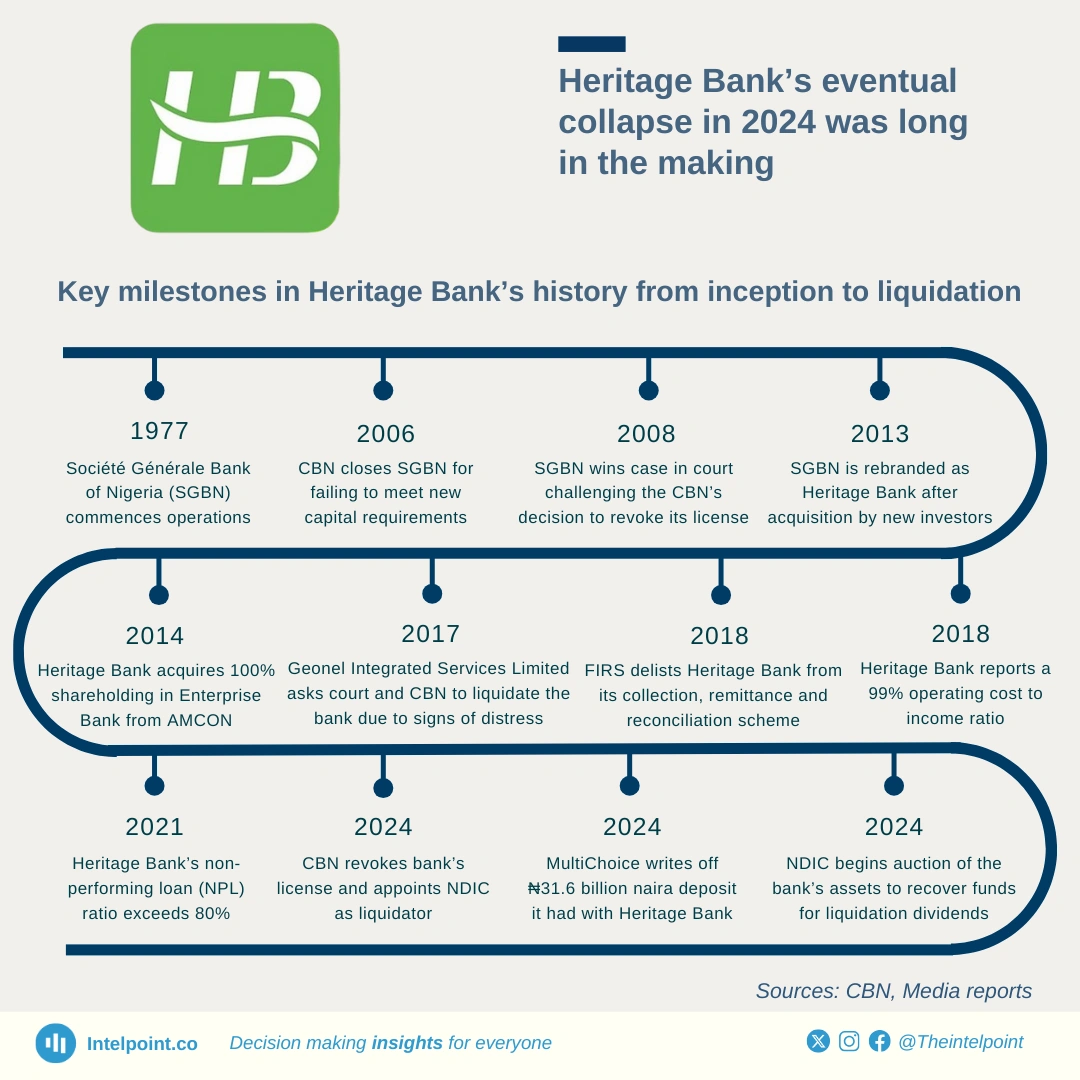

By 2021, cracks in Heritage Bank’s foundation became evident. It posted an ₦82.9 billion loss, largely due to a non-performing loan ratio of over 81%, one of the highest ever recorded in Nigeria. The Central Bank of Nigeria (CBN) closely monitored the situation, and by 2024, it was clear the bank was no longer viable. With its license revoked, Heritage Bank became another cautionary tale of how mismanagement and financial instability could bring down even a once-promising institution.