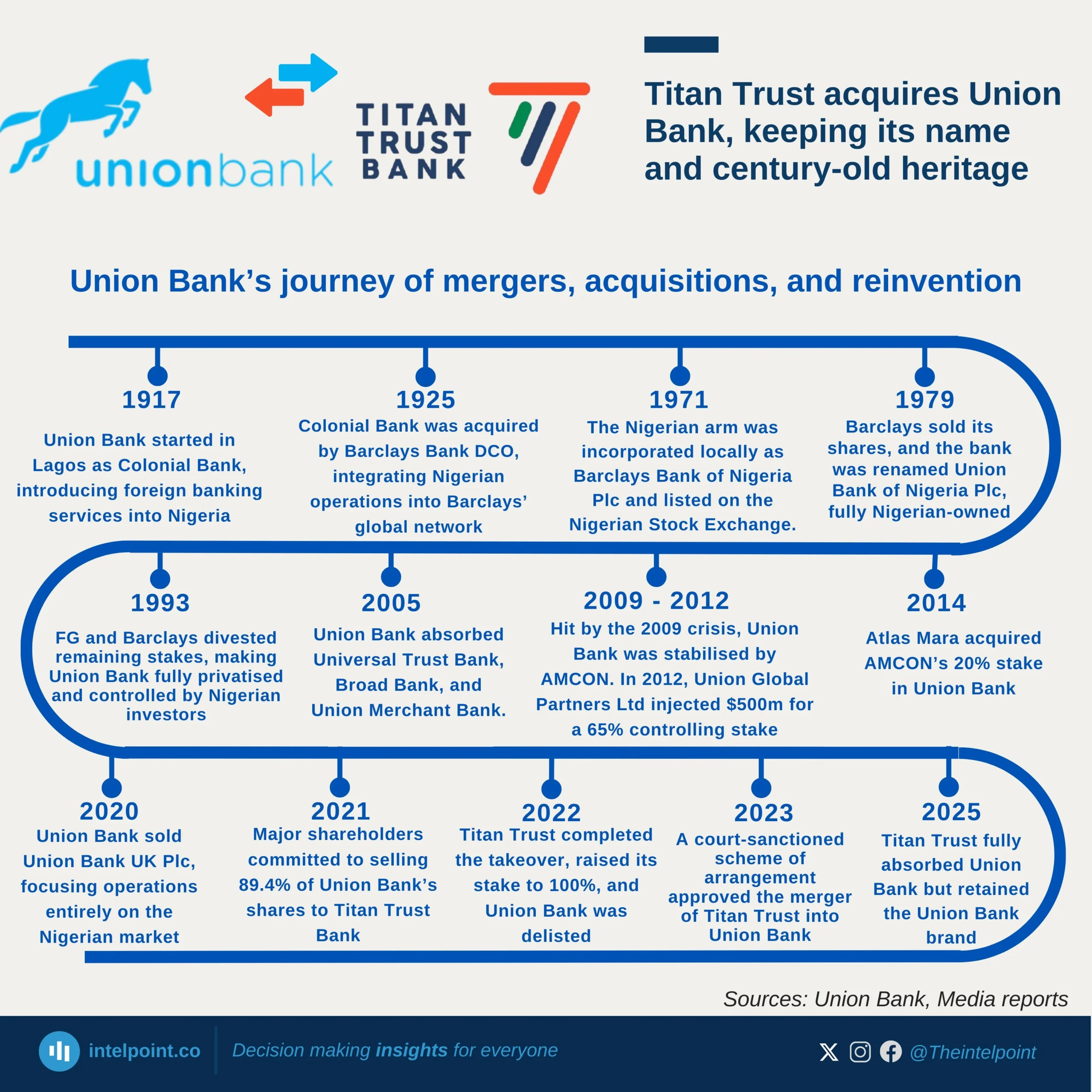

Founded in 1917 as Colonial Bank, Union Bank’s evolution mirrors Nigeria’s banking history. From Barclays’ takeover in 1925 to its indigenisation in 1979, Union Bank became one of Nigeria’s most recognised financial institutions. The 2009 banking crisis exposed deep vulnerabilities, but a $500m investment from Union Global Partners Ltd and AMCON’s intervention restored stability, ensuring the bank’s survival during a period that saw many Nigerian lenders collapse.

The biggest transformation came between 2021 and 2025. Titan Trust Bank, a much younger player, acquired full ownership of Union Bank, first by securing 89.4% in 2021 and then completing a full takeover by 2023. A court-sanctioned merger in December 2023 formally integrated Titan Trust into Union Bank. By September 2025, Titan Trust ceased as a standalone entity, choosing to retain Union Bank’s century-old name and legacy—a move that preserved public trust while marking a new chapter of reinvention under fresh control.