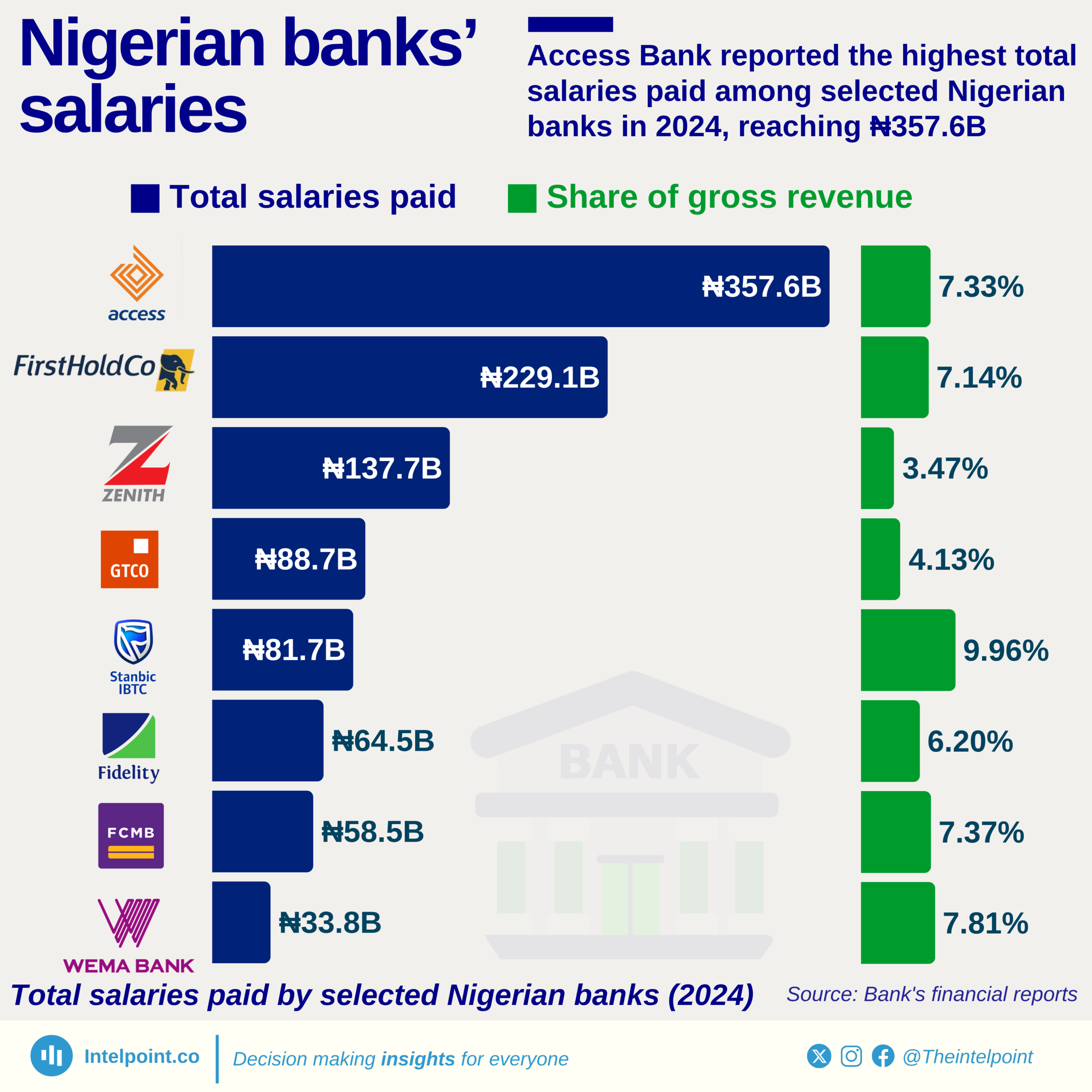

Access Bank, led in 2024, paid the highest total staff salaries among selected Nigerian banks, reaching ₦357.6 billion. This salary outlay accounted for 7.33% of its gross revenue, indicating both the scale of its operations and the size of its workforce. It was followed by First Bank’s holding company (FirstHoldCo), which paid ₦229.1 billion in staff salaries—just over 7% of its gross revenue.

While Access Bank paid the most in naira terms, Stanbic IBTC stood out with the highest salary-to-revenue ratio at 9.96%, meaning nearly one-tenth of its total earnings went to staff salaries. This suggests a more compensation-heavy structure, potentially due to a smaller workforce or stronger emphasis on human capital per unit of revenue. On the other hand, Zenith Bank’s salary spend stood at ₦137.7 billion, accounting for only 3.47% of its gross revenue—the lowest among the listed banks, indicating a leaner cost structure or higher gross income.