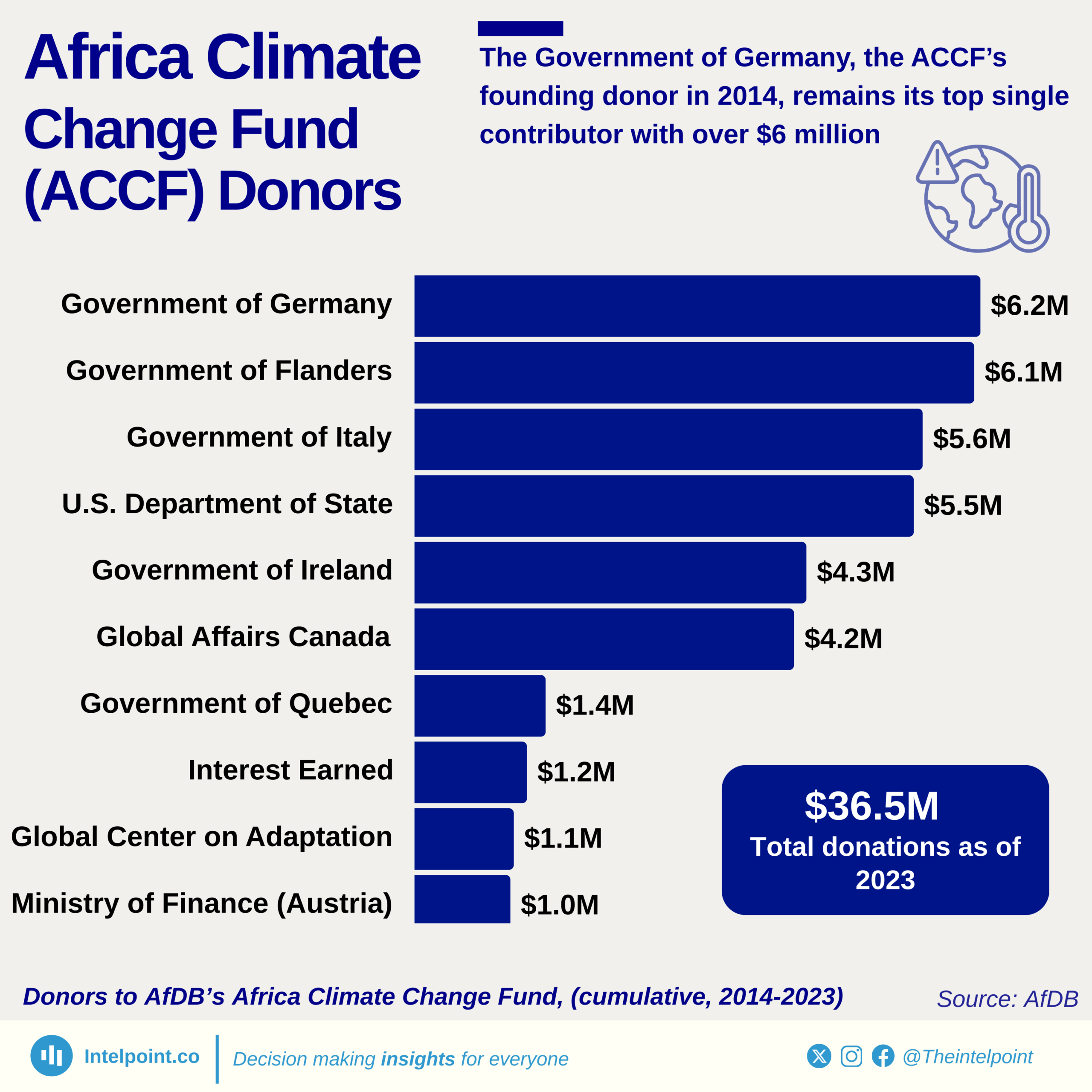

Launched in 2014, the Africa Climate Change Fund has grown into a $36.5 million pool of hope, fuelled by donors who believe in Africa’s climate future. Managed by the African Development Bank, the fund started as a bilateral partnership with Germany and later expanded into a multi-donor platform, drawing backing from the U.S. Department of State and the Government of Flanders, among others. Germany, leading since inception, gave the fund its biggest single boost: $6.19 million.

Although the U.S. became a contributor, its climate funding has faced setbacks, particularly during the Trump administration, when major foreign aid cuts and a withdrawal from key climate finance pledges strained the flow of support to African initiatives like this.

So far, over $2.6 million worth of projects have been completed, with others worth $13.2 million in progress. Among them are two multinational efforts: Empowering Women and Youth for Entrepreneurship and Job Creation in Climate Adaptation, and Support to the African Financial Alliance on Climate Change. Each effort is backed with $1 million.